Over the past several months, some crypto companies have suspended withdrawals or halted operations. In some cases, these companies have represented to their customers that their products are eligible for FDIC deposit insurance coverage, which may lead customers of these companies to believe, mistakenly, that their money or investments are safe.

The Federal Deposit Insurance Corporation (FDIC) is concerned that some customers of crypto companies, such as crypto custodians, exchanges, brokers, wallet providers, and neobanks may be confused about whether, and if so, how, they may be covered by FDIC deposit insurance.

This Fact Sheet is intended to address some common misconceptions about the scope of deposit insurance coverage and whether deposit insurance applies to funds that customers provide to these crypto companies.

The FDIC issued letters demanding five crypto companies (“Cryptonews”, “Cryptosec”, “SmartAsset”, “FTX US” фтв “Crypto.com”) and their officers, directors, and employees cease and desist from making false and misleading statements about FDIC deposit insurance and take immediate corrective action to address these false or misleading statements.

Based upon evidence collected by the FDIC, each of these companies made false representations—including on their websites and social media accounts—stating or suggesting that certain crypto–related products are FDIC–insured or that stocks held in brokerage accounts are FDIC–insured.

What is the Federal Deposit Insurance Corporation do?

The FDIC insures deposits; examines and supervises financial institutions for safety, soundness, and consumer protection; makes large and complex financial institutions resolvable; and manages receiverships.

The FDIC is providing the information below to assist the public in understanding FDIC deposit insurance coverage in light of recent market activity and media reports.

What is the FDIC?

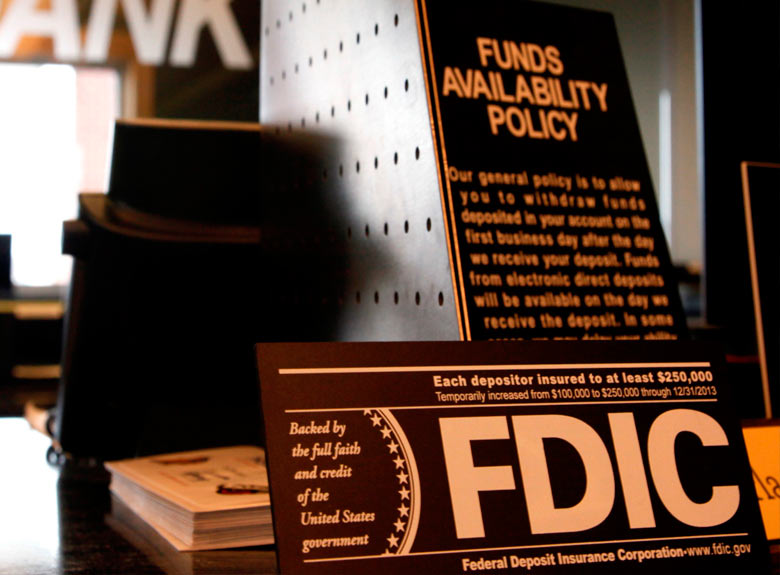

The Federal Deposit Insurance Corporation is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government.

What is deposit insurance?

FDIC deposit insurance protects bank customers in the event that an FDIC-insured depository institution fails. Bank customers don’t need to purchase deposit insurance; it is automatic for any deposit account opened at an FDIC-insured bank. Deposits are insured up to at least $250,000 per depositor, per FDIC-insured bank, per ownership category.

Deposit insurance is calculated dollar-for-dollar, principal plus any interest accrued or due to the depositor, through the date of default. For example, if a customer had a CD account in her name alone with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

FDIC Deposit Insurance Coverage

By federal law, the FDIC only insures deposits held in insured banks and savings associations (collectively, “insured banks”) and only in the unlikely event of an insured bank’s failure.

The FDIC does not insure assets issued by non-bank entities, such as crypto companies.

Since the FDIC began insuring deposits in 1934, no depositor has lost a penny of FDIC-insured funds as a result of an insured bank’s failure.

Deposit insurance applies to products such as checking accounts, savings accounts, and certificates of deposit held at insured banks.

The FDIC only pays deposit insurance after an insured bank fails. Coverage is only available for the deposits that are held in the insured bank at the time of its failure.

How can get deposit insurance?

Depositors do not need to apply for or purchase FDIC deposit insurance. Coverage is automatic whenever a deposit account is opened at an FDIC-insured bank. If you want your funds insured by the FDIC, simply place your funds in a deposit account at an FDIC-insured bank and make sure that your deposit does not exceed the insurance limit for that ownership category. See “Are My Accounts Insured by the FDIC?” for more information about the types of insurable products that are covered by FDIC insurance and the amount of deposit insurance coverage that may be available under FDIC’s different ownership rights and capacities.

What is the difference between “deposit products and “ownership categories”?

Deposit products include checking accounts, savings accounts, CDs and MMDAs and are insured by the FDIC. The amount of FDIC insurance coverage you may be entitled to, depends on the ownership category. This generally means the manner in which you hold your funds. Some examples of FDIC ownership categories, include single accounts, certain retirement accounts, employee benefit plan accounts, joint accounts, trust accounts, business accounts as well as government accounts.

Products and Risks Not Covered by Deposit Insurance

FDIC deposit insurance does not apply to financial products such as stocks, bonds, money market mutual funds, other types of securities, commodities, or crypto assets.

FDIC deposit insurance does not protect against losses due to theft or fraud, which are addressed by other laws.

FDIC insurance does not protect against the default, insolvency, or bankruptcy of any non-bank entity, including crypto custodians, exchanges, brokers, wallet providers, and neobanks.

What happens when a bank fails?

In the unlikely event of a bank failure, the FDIC responds in two capacities.

First, as the insurer of the bank’s deposits, the FDIC pays insurance to depositors up to the insurance limit. Historically, the FDIC pays insurance within a few days after a bank closing, usually the next business day, by either 1) providing each depositor with a new account at another insured bank in an amount equal to the insured balance of their account at the failed bank, or 2) issuing a check to each depositor for the insured balance of their account at the failed bank.

In some cases—for example, deposits that exceed $250,000 and are linked to trust documents or deposits established by a third-party broker—the FDIC may need additional time to determine the amount of deposit insurance coverage and may request supplemental information from the depositor in order to complete the insurance determination.

Second, as the receiver of the failed bank, the FDIC assumes the task of selling/collecting the assets of the failed bank and settling its debts, including claims for deposits in excess of the insured limit. If a depositor has uninsured funds (i.e., funds above the insured limit), they may recover some portion of their uninsured funds from the proceeds from the sale of failed bank assets. However, it can take several years to sell off the assets of a failed bank. As assets are sold, depositors who had uninsured funds usually receive periodic payments (on a pro-rata “cents on the dollar” basis) on their remaining claim.

Deposit Insurance and Dealings with Crypto Companies

To address certain misrepresentations about FDIC deposit insurance by some crypto companies, the FDIC is issuing an Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies (FDIC Crypto Advisory). Additionally, a Fact Sheet on What the Public Needs to Know About FDIC Deposit Insurance and Crypto Companies (Deposit Insurance Fact Sheet) has been posted to FDIC’s website to provide additional information about deposit insurance coverage.

The FDIC seeks to address misconceptions about the scope of deposit insurance coverage and related concerns.

By federal law, the FDIC only insures deposits held in insured banks and savings associations (collectively, “insured banks”) in the unlikely event of an insured bank’s failure.

The FDIC does not insure assets issued by non-bank entities, such as crypto companies.

The FDIC Crypto Advisory reminds insured banks that they need to be aware of how FDIC insurance operates and need to assess, manage, and control risks arising from third-party relationships, including those with crypto companies.

In dealings with crypto companies, FDIC-insured banks should confirm and monitor that these companies do not misrepresent the availability of deposit insurance.

Simultaneous with issuance of this Crypto Advisory, the FDIC issued a Press Release announcing the posting of a Deposit Insurance Fact Sheet to the FDIC’s webpage to clarify for customers of non-bank entities, such as crypto companies, and the public generally, that deposit insurance does not cover non-deposit products, including crypto assets.

The FDIC Crypto Advisory and Deposit Insurance Fact sheet provide a listing of useful resources for bankers and members of the public for more information.

Insurance for Crypto Assets

Insurance covers damage inflicted by unpredictable events, and cryptocurrency insurance is no different. Highly volatile cryptocurrency often makes headlines as the target of multimillion-dollar hacks, leading to investors losing millions and the sector shedding billions.

In its 2022 Crypto Crime Report, Chainalysis noted that cryptocurrency-based crime hit a new all-time high in 2022, with illicit addresses receiving $14 billion during the course of the year, up from $7.8 billion in 2020.

Unlike fiat currencies such as the U.S. dollar, the euro, or the Mexican peso, cryptocurrencies are not backed by governments, and there is no protection baked in to stop theft or loss of those funds. The U.S. Federal Insurance Deposit Corporation (FDIC) protects banks and thrifts from up to $250,000 in losses. However, no such protection exists for cryptocurrency.

Companies such as Lloyd’s and Relm Insurance are sliding into the crypto insurance game. Some insurers cover only crypto exchanges because that’s where the large balances of crypto funds reside.

Though not an insurance company per se, Coincover does offer an individual protection technology and software solution that attempts to prevent crypto businesses from losing crypto due to theft or human error. It covers digital assets against hacking, phishing, malware, device theft, Trojan software, and brute force attacks. The company claims its technology enables the company to compensate for when something goes wrong.

Lloyd’s has written a small number of policies in recent years for cryptocurrencies. Since this is a new and rapidly evolving area, Lloyd’s does require syndicates to proceed with caution and additional underwriting scrutiny.

Recent crypto insurance initiatives from Lloyd’s include the launch in 2021 of a new insurance policy, Lloyd’s Product Launchpad, to protect cryptocurrency held in online wallets against theft or a malicious hack.

As of June 20, 2022, the crypto firm BitGo offers a $250 million policy that covers digital assets wherever it holds private keys. The policy covers losses in the event of the copying and theft of private keys, insider theft, dishonest acts by BitGo employees, or executives’ loss of keys. BitGo’s insurance is provided by Lloyd’s Syndicate.

Insurers’ Policies Are Lacking

The insurance industry has a ways to go before it can offer solid, affordable policies that will reimburse lost crypto investments for individuals. Per an article from ZenGo, The main problem with crypto insurance offerings is that they are not fully comprehensive. For crypto holders to fully protect all of their crypto assets, they must mix and match among several different plans.

They would need one plan to protect against private key loss and another for protection against smart contract faults. They might need a third to protect themselves if their wallet company ever went out of business.

Are Cryptocurrency Accounts Protected by the FDIC?

No. Although the U.S. Federal Insurance Deposit Corporation (FDIC) protects regular checking and savings accounts against losses of up to $250,000, no such protection exists for cryptocurrency.

Is It Possible to Purchase Insurance for Cryptocurrency Investments?

Some insurance companies are offering policies that provide limited coverage against the theft of cryptocurrency funds. However, the insurance policies that are available provide reimbursements for stolen cryptocurrency funds only in certain situations. The policies generally don’t cover losses from fluctuations in the crypto market. They often do not protect against direct hardware loss and damage, the transfer of cryptocurrency to a third party, or the disruption or failure of the blockchain underlying the asset. To obtain more complete coverage, crypto investors would likely need to buy multiple insurance policies.

Revocable and Irrevocable Trust Rule Change Effective

All the rules discussed in this section are current through March 31, 2024. The FDIC approved changes, on January 21, 2022, to the deposit insurance rules for revocable trust accounts (including formal trusts, POD/ITF), irrevocable trust accounts, and mortgage servicing accounts.

For most trust depositors (those with less than $1,250,000), the FDIC expects the coverage levels to be unchanged. However, the new rule may reduce coverage for those depositors who have placed more than $1,250,000 per owner in trust deposits at one insured institution.

The new rule combines the revocable and irrevocable trust account categories into one insurance category, eliminates some complex rules, and utilizes a simple insurance calculation.

The changes are effective April 1, 2024, giving bankers and depositors time to adjust to the new rule, including making any changes to avoid a potential reduction in coverage. We suggest depositors and bankers review the new rules for time deposits with maturities beyond April 1, 2024.

Deposit insurance is one of the significant benefits of having an account at an FDIC-insured bank—it’s how the FDIC protects your money in the unlikely event of a bank failure. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.

And you don’t have to purchase deposit insurance. If you open a deposit account in an FDIC-insured bank, you are automatically covered. Check out the resources on this page to learn more about deposit insurance.

……………

by Peter Sonner

by Peter Sonner