Frequent natural catastrophic (nat-cat) events, such as the heavy rainfall in July 2023 in Northern India and the cyclone Biparjoy that hit Gujarat and parts of Rajasthan in June 2023, will challenge the profitability of the Indian property insurance industry.

According to GlobalData, the Indian property insurance industry’s loss ratio is expected to remain high at 75.2% in 2023.

The trend is expected to continue over 2023–2027, with a higher average loss ratio of 76.8%

Aarti Sharma, Insurance Analyst at GlobalData

The profitability of insurers is expected to remain challenging due to rising inflation and high claims payout due to the increased frequency of nat-cat events. Further, the recent floods in North India will prompt (re)insurers to reassess their risk and increase property insurance premium rates.

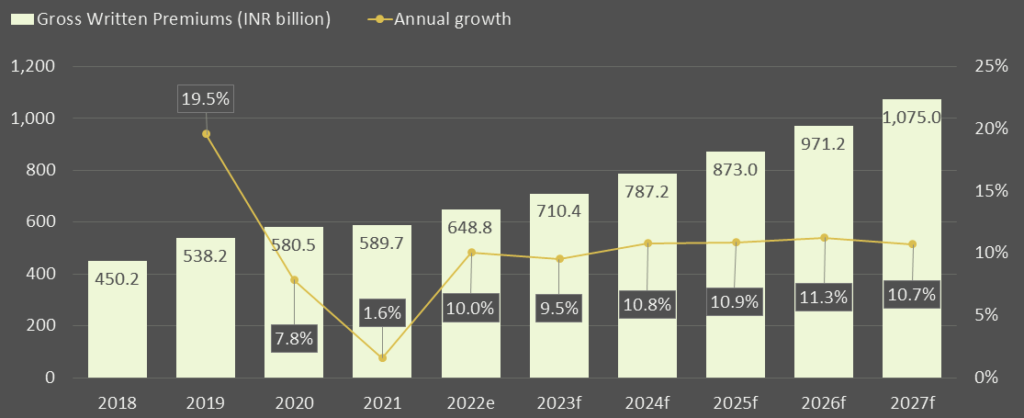

Indian property insurance premiums

Preliminary official data indicates losses from the floods in North India at around INR150 billion ($1.9 billion) with heavy damage to public and private properties. In June 2023, cyclone Biparjoy caused damage worth around INR10.1 billion ($126 million). As a result, the claims payout from both calamities is expected to be high.

Despite these challenges, the property insurance industry in India is forecast to grow over the next five years, supported by new product launches and favorable regulatory developments.

The property insurance industry is expected to grow at a compound annual growth rate (CAGR) of 10.9%, from INR710.4 billion ($9.1 billion) in 2023 to INR1,075 billion ($12.7 billion) in 2027 in terms of gross written premiums (GWP).

Agriculture insurance has been the largest contributor to property insurance premiums in India. It is expected to account for 49.3% of property insurance premiums in 2023.

The launch of Saral Krishi Bima, a parametric insurance product, in May 2023 by the Agriculture Insurance Company of India (AIC), and the proposed launch of other parametric products will broaden the coverage of agriculture insurance.

The premiums generated from the parametric products will also help property insurers partially mitigate the losses due to the high frequency of nat-cat events.

AIC received a license to launch products that cover livestock, aquaculture, and the sericulture industry in April 2023. This will support agriculture insurance growth, which is expected to record a CAGR of 11.5% over 2023–27.”

Fire and natural hazards insurance is expected to account for 44.1% of the property insurance premiums in 2023. It is expected to grow at a CAGR of 10.8% over 2023–27. Its growth over the short term is expected to be impacted by recently enacted regulations aimed at improving market practices.

From April 2023, the IRDAI scrapped the burning cost measure charged by reinsurers to insurers towards fire reinsurance premiums. As insurers don’t have to pay this cost to reinsurers, it will reduce premiums, making fire insurance more affordable.

In the same month, IRDAI also implemented fire insurance policies based on the claims history of policyholders for accurate policy pricing. Over the long term, the change will help in increasing customer confidence and support property insurance growth.

Construction and engineering are expected to account for the remaining 6.7% of the property insurance premiums in 2023.

Extreme weather events are expected to remain a major pain point for property insurers, prompting them to increase prices to maintain profitability. Insurers are likely to engage in alternate propositions such as parametric insurance and risk-based premium pricing to offset their exposure.

…………….

by Aarti Sharma – Senior Insurance Analyst at GlobalData