The U.S. property and casualty insurance industry posted another record in Q1 2026. S&P Global Market Intelligence said the sector’s combined ratio before policyholder dividends was 89.5, the best first-quarter underwriting result in at least 25 years.

The ratio including policyholder dividends was 91.9. That result was stronger than any comparable first-quarter figure recorded since 2006.

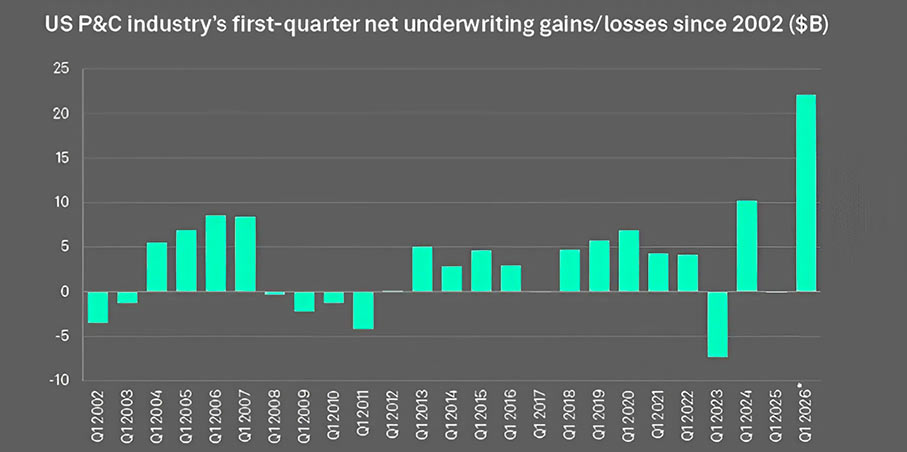

In dollar terms, the underwriting gain reached about $22.1 bn. S&P GMI said the result was driven mainly by exceptional performance in homeowners multiperil and private auto.

The record came as competition increased in major markets. Certain casualty lines also kept showing pressure.

Earlier this year, S&P GMI said the full-year 2025 combined ratio for U.S. P/C insurers was just under 93. That was the best full-year result in nearly two decades, behind only the 92.4 ratio recorded in 2006.

S&P GMI analysts also pointed to large policyholder dividends from State Farm and USAA based on 2025 results. State Farm issued $5 bn, while USAA issued $4 bn.

The analysts described both payouts as historically large for the industry and for the companies. State Farm recorded its dividend in Q1 2026, pushing the industrywide policyholder dividend ratio to nearly 2.4.

That was the second-highest first-quarter dividend ratio in 25 years. The highest recent comparison came in Q2 2020, when several mutuals and reciprocal exchanges used dividends to rebate auto premiums during the early COVID-19 period.

The homeowners multiperil loss ratio improved sharply. S&P GMI said the first-quarter 2026 ratio fell to 44.3, compared with 102.3 in Q1 2025.

Other property lines also improved. Fire and the property portion of commercial multiperil showed significant gains.

Private passenger auto remained profitable but changed less dramatically. The direct incurred loss ratio for the quarter was 60.4, down 0.6 points from Q1 2025.

That figure was 15.4 points lower than Q1 2023. At that time, the industry was still dealing with rapid loss-cost inflation.

Large personal auto insurers recorded strong underwriting results. Progressive, Allstate, GEICO parent Berkshire Hathaway, State Farm, USAA, Farmers Group, and Liberty Mutual each posted underwriting gains above $1 bn in Q1.

State Farm stood out with an underwriting gain of almost $2 bn. That marked a swing of more than $7 bn from a wildfire-hit underwriting loss above $5.0 bn in Q1 2025.

For the industry, the $22.1 bn underwriting gain was more than double the $10.2 bn gain recorded in Q1 2024. S&P GMI calculated the figure by aggregating individual company filings with the National Association of Insurance Commissioners as of May 19.

The Q1 2026 result also exceeded an inflation-adjusted first-quarter underwriting profit from 2006. S&P GMI put that 2006 figure at $14.2 bn.

S&P GMI said the industry still faces major headwinds. Private auto competition is rising, commercial property rates are falling, and casualty lines remain difficult.

Other liability loss ratios reached 65.8, the highest first-quarter result in 24 years. Commercial auto liability also deteriorated, with the direct incurred loss ratio rising to 71.1, up 3.2 points from Q1 2025.