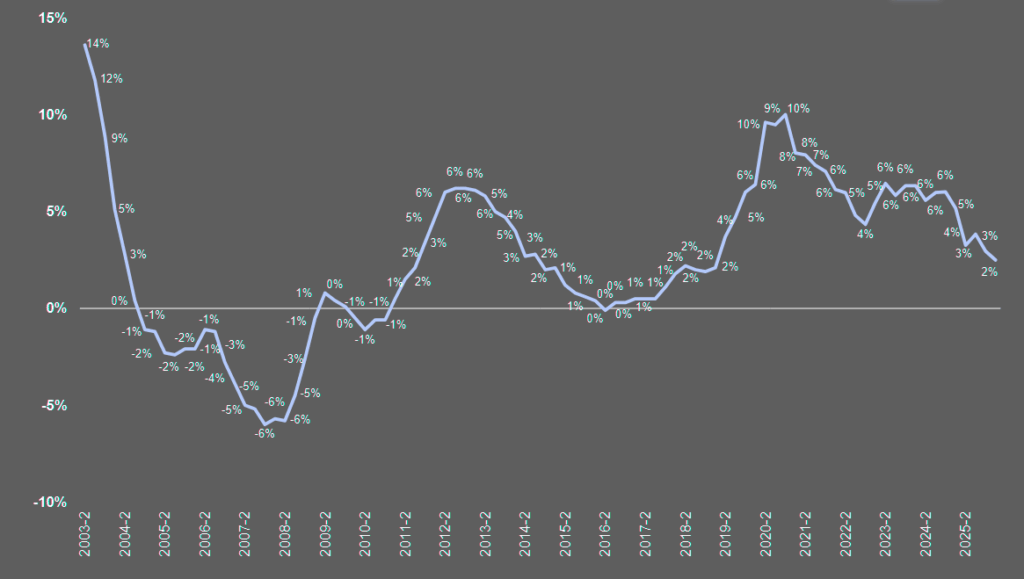

U.S. commercial insurance prices increased again in the first quarter of 2026, though the pace of growth continued to slow, according to WTW’s Commercial Lines Insurance Pricing Survey.

The CLIPS survey compared prices charged on policies underwritten during the first quarter of 2026 with prices charged for the same coverage during the first quarter of 2025.

Carriers reported an aggregate commercial price increase of 2.5%, down from the stronger increases seen across much of the post-2020 market cycle.

Commercial insurance pricing rose sharply in 2020, with aggregate increases climbing to nearly 10% from the second quarter through the fourth quarter of that year. The pace then eased, falling to just below 5% in the fourth quarter of 2022.

Pricing pressure returned in 2023, with the aggregate increase moving above 6% in the second quarter. Through the second half of 2023 and into the first quarter of 2025, commercial price growth stayed around 6% (see TOP 100 Property & Casualty Insurance Companies in the U.S.).

The market began softening during 2025, bringing the latest reported increase down to 2.5%.

Most surveyed lines still showed moderate to significant price increases in the first quarter. The main exceptions were workers compensation, directors and officers liability, commercial property, and cyber.

Those lines either showed weaker increases or price decreases compared with other commercial segments.

Change in Price Level vs. Same Quarter One Year Prior

Most lines recorded similar or lower price changes compared with the previous quarter. Excess and umbrella liability continued to produce the largest price increases, keeping pressure on insureds with higher severity exposure, litigation risk, and complex casualty programmes.

Commercial auto pricing also eased, with the increase dropping below double digits for the first time since the third quarter of 2023.

The line remains under pressure from repair costs, litigation trends, medical inflation, and vehicle technology costs, though the latest data point suggests a slower rate environment.

Commercial property showed the clearest shift in direction. After significant price increases during 2023, the line posted its first price decrease in the second quarter of 2025. That decline continued through the first quarter of 2026, following several quarters of gradually moderating increases.

Pricing also softened across account sizes. WTW said reported price increases for all account sizes were slightly lower than in the prior quarter.

That pattern suggests market easing has spread beyond selected large accounts and into broader commercial insurance placement activity.

Specialty lines still recorded a small price increase. WTW said professional liability price increases offset price decreases in directors and officers liability, keeping the specialty category in positive territory overall.

According to Beinsure analysts, the latest CLIPS data points to a commercial insurance market moving away from broad hard-market conditions and toward more line-specific pricing.

Excess casualty remains firm, commercial auto still carries loss-cost pressure, and property has moved into softer territory after several years of steep rate correction.

For brokers and risk managers, the first quarter result means renewal outcomes now depend more on line, loss history, attachment point, and account quality than on a general market-wide pricing trend.