Crypto markets still move through familiar cycles. Speculation floods in first, capital follows, and attention spikes fast. Some projects disappear once momentum fades. Others keep building underneath the noise, Andreessen Horowitz says.

That pattern keeps repeating because speculative periods often finance infrastructure that would struggle to emerge under normal market conditions.

Once the hype cools, the surviving systems usually look more practical and more durable than critics expected during the downturn.

The current market phase feels closer to infrastructure expansion than speculative mania.

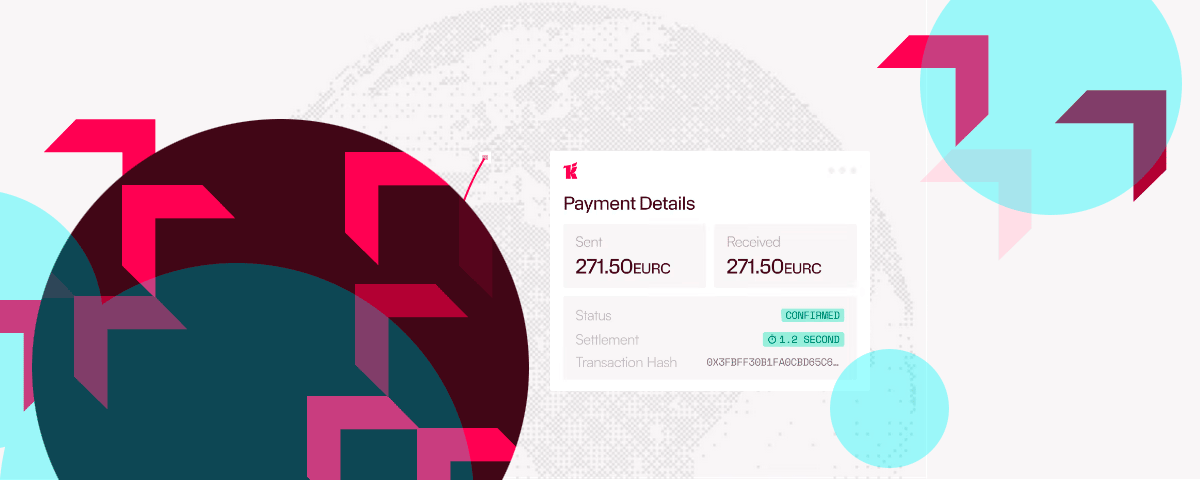

Stablecoins offer the clearest example. Trading activity across crypto markets continues fluctuating sharply, though stablecoin adoption keeps climbing through both bull and bear cycles.

People increasingly use them for cross-border payments, savings, remittances, and commercial transactions where traditional financial systems remain slower, more expensive, or operationally fragmented.

According to Beinsure analysts, stablecoins have shifted from crypto trading tools into broader financial infrastructure products supporting real transaction flows. That distinction matters because usage growth increasingly reflects utility rather than speculative positioning.

The broader financial sector has noticed. Stablecoin transaction volumes already measure in the trillions annually, while payment firms, banks, and fintech companies continue integrating blockchain settlement rails into existing infrastructure stacks.

Capital markets infrastructure is moving onchain too. Perpetual futures markets expanded sharply during recent cycles, giving traders continuous price discovery mechanisms operating outside traditional exchange schedules.

Prediction markets gained traction as alternative information systems tied to probabilistic forecasting rather than centralized editorial structures.

Onchain lending systems also matured beyond niche crypto-native activity. Stablecoin credit markets now support growing pools of collateralized lending activity tied to both digital assets and tokenized financial products.

Traditional financial assets are beginning to migrate into blockchain environments as well. Tokenized bonds, commodities, and other real-world assets increasingly move through programmable settlement systems operating continuously rather than inside limited banking hours.

The appeal is straightforward enough. Blockchain-based financial infrastructure settles transactions almost instantly, operates globally, and reduces dependency on multiple intermediaries sitting between counterparties.

Regulatory conditions have also improved compared with previous crypto cycles.

Supporters of the sector point to legislation such as the GENIUS Act as evidence policymakers increasingly prefer clearer operating frameworks over broad regulatory ambiguity. Industry participants argue structured regulation creates stronger consumer safeguards while giving startups and financial institutions more certainty around long-term infrastructure investment.

That matters because institutional adoption tends to move slowly until regulatory frameworks stabilize.

The larger argument behind crypto infrastructure extends beyond payments or trading markets. Supporters increasingly frame blockchain systems as alternatives to increasingly centralized digital infrastructure environments.

Software systems continue growing more complex, while AI platforms become more opaque and difficult for users to audit directly. Internet infrastructure also sits in the hands of a relatively small number of dominant providers.

Against that backdrop, blockchain systems offer a different model built around transparency, verifiability, distributed ownership structures, and globally accessible participation layers.

These systems also embed economic incentives directly into network operations.

Developers, users, creators, validators, and operators often participate inside shared economic structures rather than fragmented platform relationships controlled entirely by centralized intermediaries.

The practical applications already extend beyond crypto-native communities.

Blockchain infrastructure increasingly appears inside payment systems, creator platforms, decentralized computing networks, financial services, and machine-to-machine transaction environments tied to AI systems and automated software agents.

Startups still drive much of this development. Financial institutions, fintech firms, and large technology companies have started adopting parts of the infrastructure as well, largely because faster settlement, lower transaction costs, and programmable financial logic solve operational problems conventional systems still struggle to handle cleanly.

Crypto markets still carry volatility. That part hasn’t changed much. Underneath the price swings, though, the infrastructure layer keeps expanding anyway.

In practice, this means sending money globally in an instant, holding dollars without relying on a bank, tokenizing assets so they can move frictionlessly anywhere, tapping into composable networks that others can build on, and embedding these capabilities in applications everywhere.

It also includes new models that weren’t possible before: where users can own their assets and identities directly, and hold inviolable digital property rights; where swarms of software agents can decide, act, and transact on a user’s behalf, acquiring compute, data, and services as they go; and where increasingly autonomous networks can fund, govern, and evolve themselves through code.

That’s why we’re announcing our new Crypto Fund 5; it is built for this moment. The founders we’re backing with this $2.2 bn fund are working on the part of the cycle that gets less attention and we believe produces more of the lasting value: turning new infrastructure into products people use every day.

That is how every important computing platform has eventually mattered, and it is how crypto will too.