Global investors still support the AI trade, infrastructure spending and the promise of productivity growth. The risk is that valuations now leave little room for delays in AI monetisation, data-centre expansion, power supply or productivity gains, especially with financing costs still high.

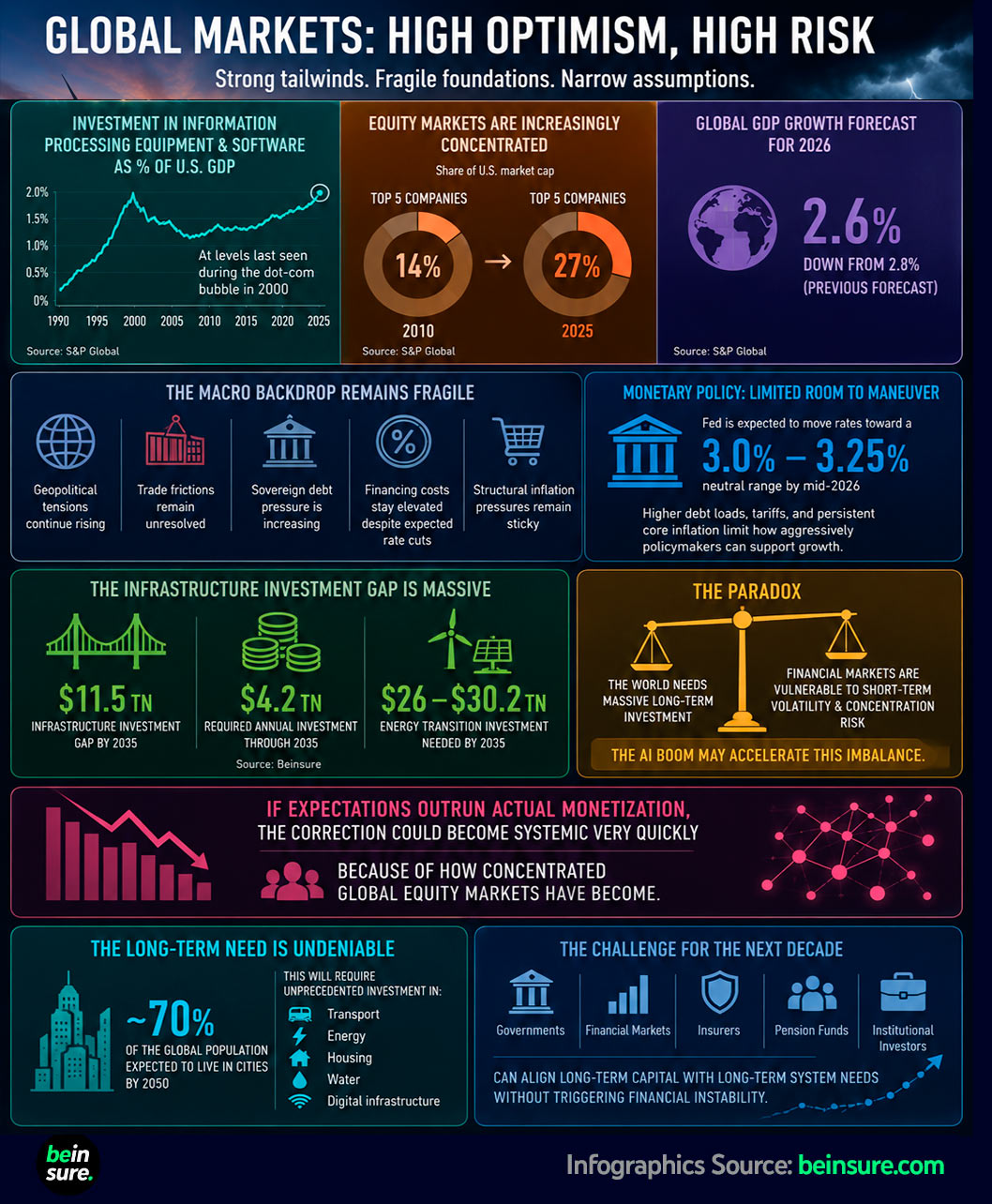

S&P Global data shows U.S. investment in information processing equipment and software, measured as a share of GDP, has climbed back to levels last seen during the dot-com bubble in 2000.

At the same time, equity markets have become more concentrated around a small group of mega-cap technology companies, leaving global indices more exposed to a correction in a limited number of names.

U.S. consumer spending represents nearly 20% of global GDP. A sharp fall in AI-led equity valuations would not remain confined to technology stocks. It would feed into household wealth, consumption, corporate investment plans, credit conditions and global growth expectations.

Markets now appear to treat AI execution risk as manageable, even as the macro backdrop stays fragile. Global GDP growth for 2026 has been revised down to 2.6%.

Geopolitical tensions are rising, trade frictions remain unresolved, sovereign debt pressure keeps building, financing costs remain high despite expected rate cuts, and structural inflation pressure has not faded.

Central bank easing will not remove those constraints by itself. The Fed is expected to move rates toward a 3–3.25% neutral range by mid-2026, but higher debt loads, tariffs and persistent core inflation restrict the amount of support policymakers deliver without creating fresh risks elsewhere.

Infrastructure makes the equation harder.

The global economy faces an infrastructure investment gap estimated at $11.5 tn by 2035, requiring about $4.2 tn in annual investment. Energy transition alone requires between $26 tn and $30.2 tn by 2035, according to Beinsure.

This leaves markets with an uncomfortable mismatch. The world needs long-term capital at huge scale, yet financial assets have become more exposed to short-term volatility, expensive funding and concentration risk. AI spending intensifies that mismatch because it raises demand for chips, power, data centers and networks at the same time investors expect quick financial returns.

If expectations move ahead of actual monetization, the correction might spread fast. Too much market value now sits in few listed companies, and investors have attached a large part of the global growth narrative to a narrow group of technology stocks.

Urbanization adds more pressure to the same investment problem. By 2050, around 70% of the global population is expected to live in cities, forcing heavier spending on transport, energy, housing, water systems and digital infrastructure.

The next decade will test whether governments, insurers, pension funds and institutional investors direct long-term capital into long-term economic needs without adding financial instability.

……………….

AUTHOR: Oleg Parashchak – CEO & Founder of Finance Media Holding