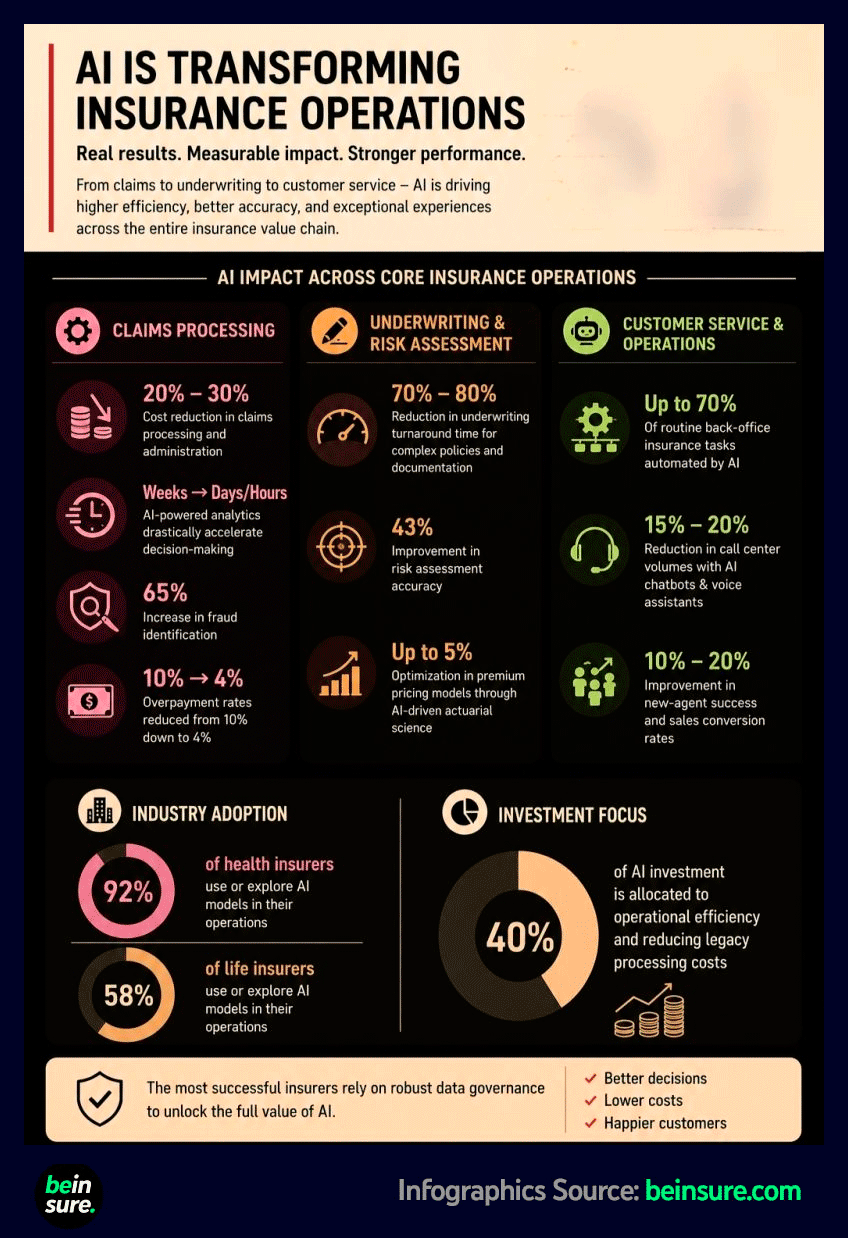

AI is already producing measurable gains across insurance, which makes the slow pace of adoption harder to explain at first glance. Claims processing and administration costs are falling by 20-30%, underwriting turnaround times are improving by 70-80%, and fraud detection performance has increased by about 65%.

Risk assessment accuracy has improved by 43%, claims overpayment rates have dropped from 10% to 4%, and premium pricing has improved by up to 5%. Routine back-office automation now reaches up to 70% of tasks in some operating areas.

According to Beinsure, the slowdown does not come from a lack of proven use cases. It comes from the gap between a working AI tool and a controlled insurance process. Insurers handle regulated decisions, personal data, medical information, long-tail liabilities and customer outcomes that regulators examine closely.

- Claims teams want faster settlement.

- Underwriters want sharper pricing.

- Fraud teams want better pattern detection.

- Senior management, though, needs audit trails, explainable outputs, legal comfort and clear accountability before AI moves from pilot work into daily decision-making.

Customer service already shows the same pattern. AI has reduced call centre volumes by 15-20% in some cases, and agent productivity or conversion rates have improved by 10-20%. The operational case looks obvious, but insurers still need clean data, trained staff and reliable escalation rules when automated systems reach the limits of their judgement.

Health insurers are moving fastest, with 92% using or exploring AI. Life insurers follow at 58%. The difference matters because use cases, regulation, data structure and risk tolerance vary sharply across lines of business.

AI investment budgets also reveal a practical bias. 40% of spending targets operational efficiency, where savings are easier to measure and boards see faster payback. Claims processing, underwriting, fraud detection, customer service, pricing, risk assessment, actuarial modelling and back-office operations attract the most attention.

According to Beinsure, insurers that move slowly often face the same internal blockers: fragmented data, old policy systems, unclear model governance, limited AI skills and resistance from teams that have seen previous technology programmes overpromise.

……………….

AUTHOR: Oleg Parashchak – CEO & Founder of Finance Media Holding