Overview

Central banks to live with inflation, but only after stalling growth. The Great Moderation, from the mid-1980s until 2019 before the Covid-19 pandemic struck, was a remarkable period of stability of both growth and inflation. We were in a demand-driven economy with steadily growing supply. Borrowing binges drove overheating, while collapsing spending drove recessions. Central banks could mitigate both by either raising or cutting rates.

According to BlackRock Investment Institute`s Midyear Outlook, that period has ended, in our view. First, production constraints – stemming from a massive shift in spending and labor shortages – are hampering the economy and driving inflation. Second, record debt levels mean small changes in interest rates have an outsized impact – on governments, households and companies. Third, we find the hyper-politicization of everything amplifies simplistic arguments, making for poorer policy solutions.

The Great Moderation, a period of steady growth and inflation, is over. Instead, we are braving a new world of heightened macrovolatility – and higher risk premia for both bonds and equities.

Black Rock are bracing for volatility in this new regime – our first theme. Central banks are rushing to raise rates to contain inflation that’s rooted in production constraints. They are not acknowledging the stark trade-off: crush economic growth or live with inflation. The Federal Reserve, for one, is likely to choke off the restart of economic activity – and only change course when the damage emerges. We see this driving high macro and market volatility, with short economic cycles.

Equities would suffer if rate hikes trigger a growth downturn. If policymakers tolerate more inflation, bond prices would fall. Either way, the macro backdrop is no longer conducive for a sustained bull market in both stocks and bonds, we believe. We see higher risk premia across the board and think portfolio allocations will need to become more granular and nimble.

We think we will be living with inflation – our second theme. For all the noise about containing inflation, we see policymakers ultimately living with some of it. We remain overweight equities and underweight government bonds in long-term portfolios. We expect investors to demand more compensation to hold long-term bonds in this new regime. We see a near-term risk of growth stalling and reduce equities to a tactical underweight. We prefer to take risk in credit because we see contained default risk.

The Great Moderation was a period of steady growth and inflation. It supported bull markets in stocks and bonds for decades. We think it is over

We see the bumpy transition to net-zero carbon emissions also shaping the new regime – and believe investors should start positioning for net zero, our third theme. Webelieve investors can be bullish on both fossil fuels and sustainable assets, as we see a key role for commodities in the transition. Yet our work finds that changing societal preferences can give sustainable assets a return advantage.

End of the Great Moderation

Academics Jim Stock and Mark Watson coined the term Great Moderation in 2002 to describe the period of steadily lower volatility in inflation and activity. Was this combination due to good policy or good luck? For a long time, people thought it was sound policies. Stock and Watson argued it was mostly luck. We think they got it right.

Steadily expanding production capacity and demand shocks were key features of the Great Moderation.

Exuberance and borrowing binges drove overheating, while souring sentiment and collapsing spending drove recessions. Central banks could mitigate both by raising or cutting rates. The policy response did not involve trade-offs; there was no conflict between stabilizing both. This helped spark a bull market in both bonds and equities.

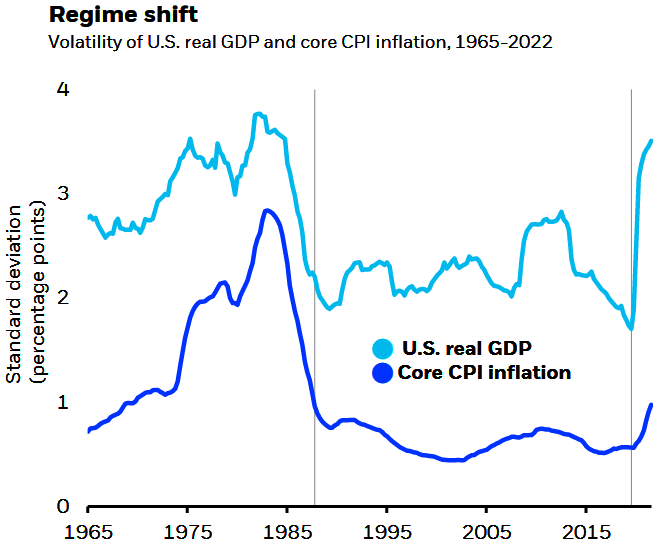

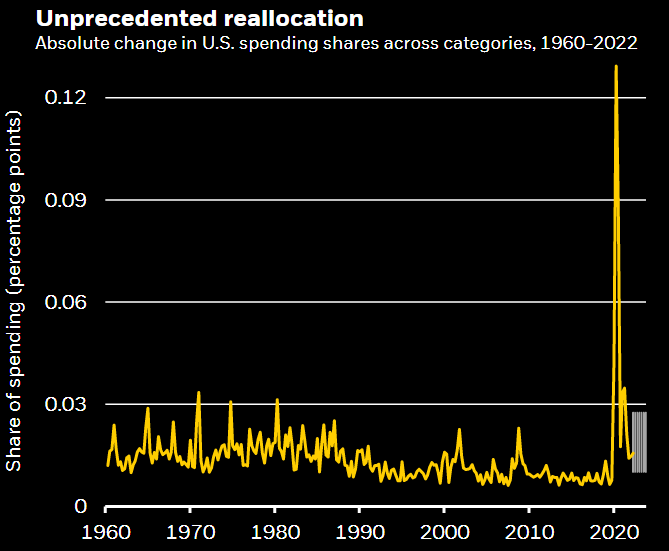

This is no more, in our view. The chart shows the regime of subdued inflation and output volatility is over. Why is this happening?

Production constraints

Production constraints have been hampering the economy in ways they never did during the Great Moderation. The pandemic triggered a massive sectoral reallocation that has yet to normalize. The key bottleneck has been labor supply, rather than supply chain disruptions. Many people are hesitant to go back to work or are taking longer to find a job in a new sector. The constraints have been exacerbated by the Ukraine war’s energy and food price shocks – and are driving today’s inflation (see Most Common Investment Strategies).

We don’t see this changing any time soon. Two powerful structural trends are driving up production costs. First, the pandemic and Ukraine crisis are accelerating geopolitical fragmentation. Think of ongoing sanctions on Russia, the push for energy security and effort to diversify supply chains.

The pandemic upended an unusual period of mild volatility in output and inflation

Second, the transition to reach net-zero carbon emissions by 2050 is likely to create a sectoral shakeout similar to the pandemic. The transition is essentially a handoff from carbon-emitting production methods to zero-carbon ones. This handoff can be rough. Carbon-intensive production can fall faster than lower-carbon alternatives are phased in. The result: periods of supply shortages and high prices for the carbon-intensive outputs the economy still needs. We see these imbalances helping drive macro volatility and persistent inflation in years to come.

Unprecedented leverage

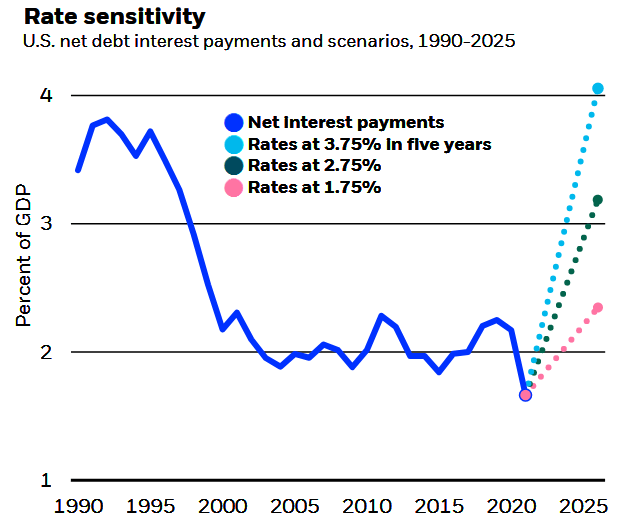

In this new world shaped by supply, trade-offs for policymakers become starker – at a time when their maneuvering room has shrunk. Global debt has surged to new highs as governments sought to limit the fallout from the pandemic. This means that small rises in interest rates can have an outsized and painful impact, as the chart shows (see Strong Smart Investment Strategies). The private sector debt is also susceptible to higher rates, especially via housing. All this makes it tougher for central banks to hike rates – and ultimately more tempting to live with inflation.

Politicization of everything

A more complex world needs nuanced discussion to find the best solutions. The problem: Everything has become politicized – and whoever has the loudest or simplest argument often wins. We believe this is helping bring about the end of the Great Moderation.

The political dialogue oversimplifies many topics. This is true for inflation. There is a loud chorus of critics who claim the inflation threat was there for everyone to see: if only central banks had raised rates earlier, we wouldn’t be in this mess.

Rather than pushing back on this narrative, central banks have resorted to sounding ever tougher on inflation. They appear to solve for the politics of inflation, not the economics. It is also true for controversial topics like climate change or geopolitics. The populism and extremism on both sides of the discourse is not abating, in our view.

All this implies that policy trade-offs are now much harder. Central banks are likely to veer between favoring growth over inflation, and vice versa. This will result in persistently higher inflation and shorter economic cycles, in our view. The end result: higher risk premia across the board.

The sensitivity of high debt levels to higher interest rates makes it harder to contain inflation via rates

Higher risk premia

The Great Moderation fostered a steady macro backdrop that set the stage for decades-long bull runs for both stocks and bonds. Central banks could soften demand shocks and pump up growth with looser policy – facing only a modest trade-off of inflation.

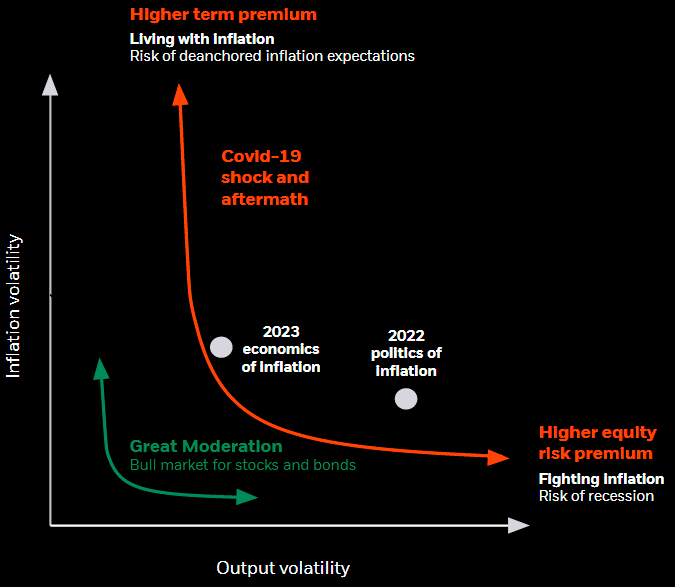

The end of the Great Moderation means the trade-offs become much starker, as the orange line in the chart shows.

The entire curve has shifted and lengthened, magnifying the impact of policy decisions. At one extreme, central banks crush growth to rein in inflation. This raises recession risk and is particularly damaging for equities. It’s a 2022 story, in our view. At the other extreme, central banks go easy and face the risk of inflation soaring. Bond prices fall as investors demand a higher term premium. We expect this to be the main conundrum for 2023.

Higher term premium

Bracing for volatility

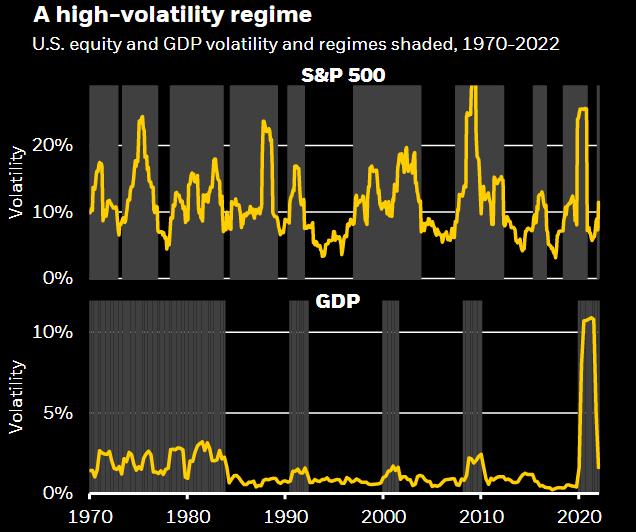

The low market volatility during the Great Moderation was due to that regime’s steady growth and inflation. We argued in 2017 that macro and market volatility regimes are linked. Some saw the low market volatility at the time as a sign of investor complacency – but we pushed back against that view. We saw volatility not having a normal bell curve distribution and behaving as a regime – in this case we break it into four regimes.

We have entered a regime of higher macro and market volatility. This implies that market views may have to change more quickly and get more granular

We didn’t see market volatility breaking into a higher regime unless macro volatility did as well. Now it has – see the gray bands in the chart – and we could go back to the volatility seen in the 1970s. Periods of low market volatility in this higher volatility regime couldindicate investor complacency (see Key Strategies for long-term).

We have laid out why we see the end of the Great Moderation. We see the rewiring of global supply chains and the transition to net zero reinforcing why this is likely to be a more volatile world – and this new regime won’t be temporary.

What are the implications?

- We expect higher risk premia for both equities and bonds.

- This regime is not necessarily one for “buying the dip.” Policy will not quickly step in to stem sharp asset price declines.

- A traditional 60/40 portfolio of stocks and bonds, hedges and risk models based on historical relationships won’t work anymore, we think.

- We believe views should get more granular at the sector level or below. For example, indebted companies may do well if their debt burden is alleviated by persistently higher inflation.

- It is even more important to recognize and overcome behavioral biases, such as inertia, when making big portfolio decisions.

- Market views will have to change more quickly on both tactical and strategic horizons, we believe.

A higher macro volatility regime is typically needed to sustain a higher market volatility regime, as we expect

Living with inflation

We are in a world shaped by supply unlike any we have seen in recent decades. Major spending shifts and production constraints are the driving force of inflation rather than excessive demand. Those constraints find their roots in the pandemic, and worsened after Russia’s invasion of Ukraine and China’s lockdowns to combat Covid-19. Think of how the war caused a commodities price spike and increased inflation.

Major central banks are jacking up policy rates in a rush to get back to neutral levels that neither stimulate nor restrain activity. The Fed is planning to go further, pencilling in rate hikes that go well intro restrictive territory to near 4% in 2023.

The problem: Rate hikes don’t do much against today’s inflation. The Fed has to crush activity in the rate-sensitive part of the economy to bring inflation back to its 2% target. Yet the Fed has so far failed to acknowledge this. The Fed and other central banks face a difficult trade-off: trying to stabilize output or inflation – but not both.

Eventually, we see the Fed living with higher inflation as it sees the effect of its rate hikes on growth and jobs – and it comes under pressure to change course. For now, however, we think the Fed has boxed itself into responding to the politics of inflation, not to the economics of it. This has caused us to reduce portfolio risk.

We will likely see real economic pain – halting the ongoing restart – before the Fed changes course, and there isn’t enough time for incoming data to stop the Fed in its tracks. We see this resulting in the worst of both worlds: persistent inflation amid short economic cycles.

When the macro environment is shaped by production constraints, the Fed and other central banks can’t avoid volatility. With politics and economics shaping their policy priorities over time, central banks will likely add to that volatility. When prioritizing politics over economics, we think the signal from central banks is going to be less useful than during the Great Moderation.

The U.S. economy has seen the largest sectoralshift on record as consumer spending moved from services to goods – and has not normalized yet

The war in Europe is the most significant crisis in decades

Food security and energy needs are key concerns. The conflict is likely to be protracted as both sides expand aims, accelerating the rewiring of global ties in a fragmenting world.

Europe has borne the brunt of the energy and commodity surge after the invasion. We see clearer risk of recession as the energy crunch hits real, or inflation-adjusted, incomes.

The European Central Bank (ECB) looks on the brink of a potential policy misstep – insisting that growth can hold up to justify higher rates. We think the ECB will realize its mistake sooner than the Fed. The euro area should feel the economic shock earlier and has a lower starting point of growth than the U.S.

The ECB already tried to offset its own hawkishness with an emergency meeting on its “anti-fragmentation” tool that aims to contain rising borrowing costs in weak economies. The catalyst? The spread on 10-year Italian bonds is approaching previous stress points, as the chart shows.

It’s not all bad, though. We should not underestimate the strengthened unity of Europe in the face of Russia’s aggression.

According to Global Risk Management Survey, Europe has the opportunity to create a more sustainable and more resilient version of itself – replacing high dependencies on Russian energy and shedding the image of an “old” economy by accelerating the green transition. Rising rates aren’t bad for everyone either – euro area bank stocks could get a boost from interest income as rates finally resurface from negative territory.

The war in Ukraine will have lasting effects, accelerating geopolitical fragmentation and the emergence of blocs.

Tom Donilon, Chairman – BlackRock Investment Institute

We are underweight European equities. The energy shock’s toll on growth will weigh on risk assets. We’re neutral government bonds and think market pricing of rate hikes is still too hawkish.

The old emerging market (EM) investment strategy

The old emerging market (EM) investment strategy of buying broad exposure to growth and “cheap” assets needs to evolve, in our view. First, the EM moniker is a misnomer. China stands on its own, and differences between other countries are set to grow. Second, we think the new market regime suggests a focus on economies than can generate income in the rewired global economy versus the old play on growth and capital appreciation.

Third, many EM central banks hiked early and to well above pre-Covid levels. Inflation could ease as developed market (DM) central banks tighten policy, giving many EM central banks room to pause hikes before the end of 2022.

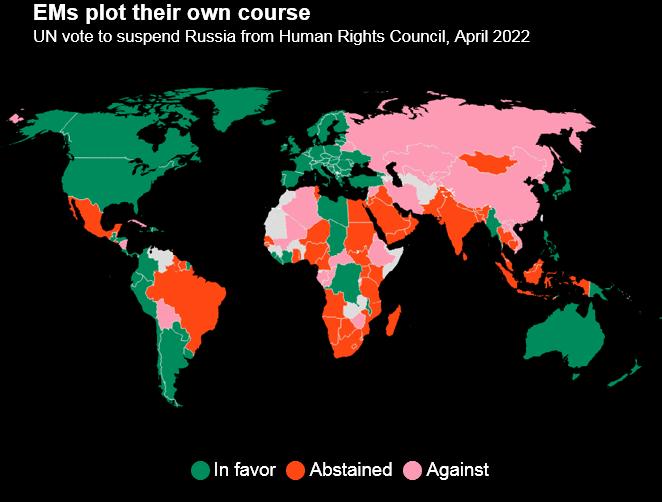

Lastly, EMs are plotting their own course in a world dominated by U.S.-China competition and keeping options open. Many countries didn’t vote on a resolution to expel Russia from the UN Human Rights Council after it invaded Ukraine. See the chart. Many EM nations could become part of a sort of non-aligned movement like in the Cold War.

We could see many EM nations becoming part of a sort of non-aligned movement reminiscent of the Cold War

For China, we see a strong restart of economic activity in the second half as Covid-19 lockdowns ease and the regulatory clampdown on tech and other sectors takes a break. Higher levels of elderly vaccination and more forceful policy support for the economy would be needed for us to upgrade Chinese equities from neutral. We see economic growth below this year’s “about 5.5%” official target.

China’s ties to Russia also have created a new geopolitical concern that requires more compensation for holding Chinese assets, we think.

Cutting risk, being nimble

A new regime is taking hold – but we do not see this yet reflected in the pricing of stocks and bonds.

Heightened volatility creates greater market mispricing, and this is embodied in our tactical views.

We have repeatedly trimmed risk this year – and do so again now. We have cut DM equities to underweight. The reasons: We see an increasing risk of the Fed overtightening, expect growth to stall and see earnings estimates as overly optimistic. U.S. stocks make up the bulk of DM equities, and other markets tend to move in synch with the U.S. market. The exception: We are neutral on Japan equities because of still-easy monetary policy and increasing shareholder pay-outs.

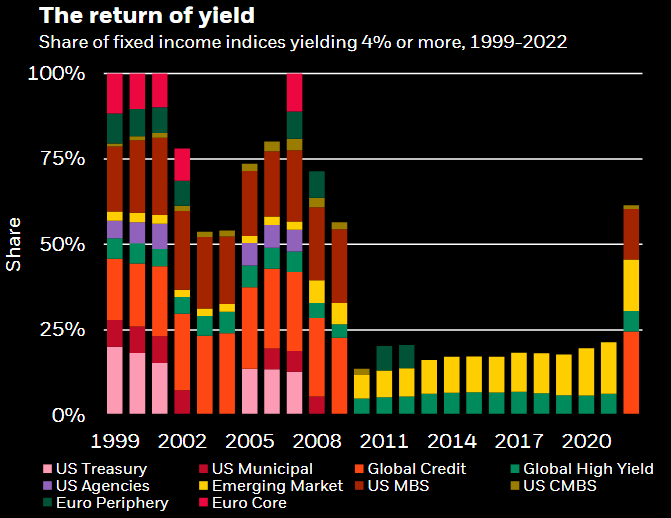

We are upgrading credit to overweight, preferring to take risk there rather than in equities. Why? Investors are compensated for owning credit these days. A majority of fixed income assets are yielding 4% or more for the first time in more than a decade.

A majority of fixed income assets now yield 4% or more for the first time in a decade, making credit more attractive

The policy response to the pandemic allowed companies to build up cash buffers and issue longer-term debt at record-low interest rates. We don’t expect a deep recession, so defaults should be manageable.

We stay underweight long-dated U.S. Treasuries as we see the term premium rising. We are overweight inflation-linked bonds, and now prefer the euro area. We now overweight UK gilts as we see the Bank of England turning dovish.

The new regime requires being nimble and frequent tactical changes, we think. For example: spotting the turning point for stocks when markets eye a dovish pivot by central banks.

Private markets in a new regime

Private market valuations are not immune in this new regime of higher volatility, in our view. Overall, we see a tougher market environment for some private assets than in recent years, just as we do for public assets.

We believe private assets – while not appropriate for all investors – still have a sizeable role to play in strategic portfolios. Allocations should, on average, be higher than what we typically see in institutional portfolios, in our view. But we think selectivity is more important than ever.

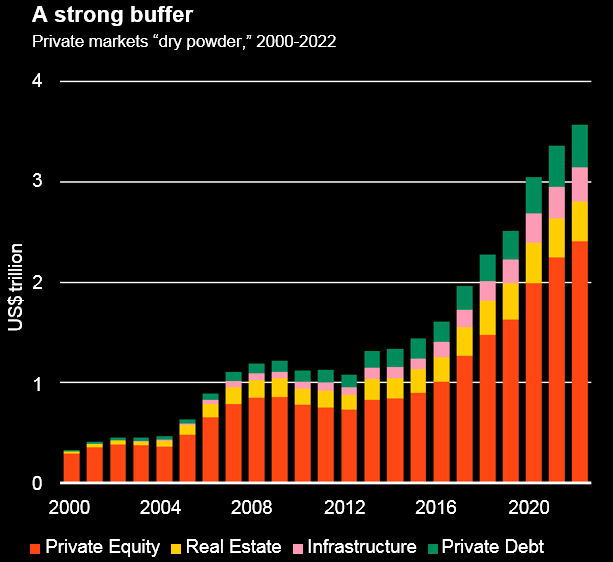

We see both a higher path of policy rates and higher long-term yields over a strategic horizon. This matters most for tech-heavy growth private equity (PE) that has dominated in recent years. Yet ample capital has yet to be deployed. See the chart. We believe this “dry powder” can provide financing options, support the net-zero transition in areas like infrastructure and help troubled companies with fresh capital.

We have seen this before. A 2017 paper on PE during the 2008 financial crisis showed how PE-backed companies received capital injections during bouts of public market stress – and increased investments as a result relative to their peers.

Available capital in private markets can provide a buffer to companies during periods of public market stress

Yet better opportunities may be found in private credit , such as gaining exposure to floating-rate debt. Middle-market loans, made to small- and mid-sized companies, are typically floating rate. This makes them attractive when rates are rising.

Infrastructure assets have the ability to pass on higher prices – key in this environment of persistently higher inflation. We prefer private credit over public on a strategic horizon.

The ability to pick top-performing managers will be more important than ever, in our view, and only some investors will be equipped to do so. We believe central banks are unlikely to provide a backstop to risk assets as they did in the past.

………………………..

AUTHORS: Philipp Hildebrand — Vice Chairman BlackRock, Jean Boivin — Head BlackRock Investment Institute, Wei Li — Global Chief Investment Strategist BlackRock Investment Institute

Fact checked by  Oleg Parashchak

Oleg Parashchak