Overview

- How Real-Time Data Analytics Impacts Insurance Providers

- Sample Architecture of Insurance Data Analytics Systems

- The Key Features of Insurance Data Analytics Software

- Challenges of Real-Time Analytics for High-Risk Policy Detection

- Costs of Insurance Data Analytics Software

- The Future of Insurance Risk Assessment

Estimates put insurance fraud losses at around $308.6 bn every year. That number is just in the United States. The result is higher premiums and greater risk placed on insurers and reinsurers, which slows the industry and increases premiums to target consumers, according to ScienceSoft.

Every new policy carries some degree of risk. Identifying where that risk lies is crucial to identifying potential threats and reducing fraudulent claims.

Integrating real-time data analytics through big datasets, artificial intelligence, and machine learning technologies empowers companies to detect high-risk policies before solidifying agreements.

How Real-Time Data Analytics Impacts Insurance Providers

Covering someone for health, travel, auto, life insurance, or other policies requires a dynamic view of historical, current, and real-time data. Policyholders must be carefully assessed so that several risk factors enhance claims maintenance and improve underwriting accuracy.

For example, the black box traditionally used in vehicles and airlines provides assessment information before, during, and after an accident.

While that can help weed out responsible parties, insurance companies need to personalize information to the user to better match policies with behaviors.

With real-time data through AI and app-connected telematics, premiums are based on more accurate behavior. Information like how frequently a driver brakes, average speed, and even the number of times a vehicle is used informs insurers how much coverage is necessary and at what rate.

AI offers dramatic gains in efficiency for tasks like data processing, tracking financial trends, calculating reserve requirements, and adjusting operational budgets in response to changes

Olga Vinichuk, Business Analyst and Insurance IT Consultant at ScienceSoft

UBI (usage-based insurance, sometimes called “pay as you go” policies) is changing the industry by providing the real-time analytics necessary to identify higher-risk policies. That is why it is experiencing a market growth of $43.38 bn in 2023 to $70.46 bn by 2030.

Sample Architecture of Insurance Data Analytics Systems

To gain the information needed for better policy decision-making, insurers must create a system architecture that supports the flow of that data.

These systems are extremely diverse and require a more structured approach, so numerous data sources, processing techniques, and insights are delivered.

- Data Collection & Sources: Everything from customer demographics to historical claims, credit scores, IoT device reports, and even social media must be collated, cleaned, and organized.

- Data Processing & Integration: Data must be processed through cloud computing solutions so insurers can scale infrastructure when necessary. That includes data lakes for unstructured data and real-time processing engines for a continuous flow of immediate insights.

- AI & ML for Risk Assessment: The ability to analyze all of the collected and cleaned data to automate predicting future high risk. NLP (natural language processing) can be included to accelerate risk scoring and decision-making.

- Visualization & Decision Support: Raw data alone does not benefit insurer decision-making. Interactive visual elements help underwriters make informed decisions and quickly detect emerging risks.

A recent survey from the Cleveland Clinic showed roughly half of Americans wear at least one type of technology to monitor health (primarily heart rate).

Consumers are already comfortable with real-time monitoring of behaviors and key statistics. Dash cameras in cars and rings that measure heart patterns are now commonplace.

All kinds of connectivity are available. The trick is setting up an infrastructure that allows insurers to track, collect, inform, and report on such metrics for better risk assessment.

The Key Features of Insurance Data Analytics Software

Insurers must integrate specialized data analytics software to detect high-risk policies effectively and efficiently.

A generalized reporting or data-gathering solution may not provide the insightful analysis required or the capability to “learn” over time based on the needs of the company.

These software packages should have features like:

- Fraud detection algorithms to flag potentially suspicious claims or anomalies. This lets AI-driven models detect anomalies and behavioral patterns that can be trained over time to improve accuracy.

- Automated underwriting that adjusts policy terms in real time to personalize the experience. Customers receive a fair pricing model while companies reduce expensive underwriting errors.

- Customer segmentation modeling for predicting customer behavior. Policyholders are placed into different risk categories to tailor coverage options and improve marketing strategies.

- Compliance monitoring to remain accurate and “in good standing” with regulatory oversight. These tools ensure the company meets legal and financial standards, even automatically updating policies and documentation to align with changing government guidelines.

- Claims automation so the approval process is streamlined and frees up valuable human asset time. This improves response times and enhances customer satisfaction – boosting a company’s reputation and standing in the industry.

The goal is to refine risk modeling so insurers lower losses while also improving operational efficiency by reducing manual intervention.

The more time team members can spend on other business processes instead of getting lost in endless paperwork, the better.

Unfortunately, not all software solutions are built the same. What works for one provider will likely not be the same for another. There will be challenges to overcome as new integrations are brought online.

Steps to manage these challenges might include:

- Assessing existing infrastructure to evaluate how data is managed and identify potential gaps in flow.

- Investing in scalable solutions that offer cloud-based support or hybrid analytics features.

- Integrating data sources like IoT reporting, public records, and historical customer information.

- Developing AI/ML models that can be trained to predict higher-risk policies better.

- Ensuring full data security and compliance adhering to GDPR, HIPAA, and other regulations.

- Training personnel and customers so everyone is comfortable with the new data literacy integrations.

Challenges of Real-Time Analytics for High-Risk Policy Detection

Insurers do not exist in a box. Plenty of external pressures cause challenges in implementing digital transformation into real-time analytics. In 2020 and early 2021, around 200,000 people had their driver’s license number exposed by well-known insurance company Allstate and its subsidiaries. Safeguards for private information must be in place before onboarding and integrating new data analytics systems.

The costs of cloud-based SaaS (while shrinking due to AI) can be challenging for insurers based on the size and scope of operations.

While they are far more cost-efficient than on-premise infrastructure, the budget for new tools must be considered, and a cost-benefit analysis should be conducted.

Integration complexity is also a challenge. Not every team member or customer may be prepared to use such systems. A phased rollout with pilot programs helps reduce possible disruptions and ensures smoother adoption of technologies.

In the insurance industry, there’s no room for error. That’s why when building insurance-related software, it’s important to take everything into account, from general terminology to business and location specifics of the client.

Olga Vinichuk remarks

Costs of Insurance Data Analytics Software

There is no “out of the box” fee for developing or onboarding comprehensive real-time data analytics for policy risk detection.

As a small example, most SaaS-based analytics solutions can range from $25,000 for a basic application to $500,000 for more complex solutions.

These costs do not include upgrading infrastructure for cloud services, implementation and training, ongoing maintenance, and data storage.

The manual costs for updates, security, and data retention alone will most likely run 10-20% of the initial investment.

Consideration must be placed on comparing the cost of upgrading with the potential loss of not integrating real-time data. Fraud prevention savings, faster claims processing, and improved underwriting accuracy all offer exponential value for insurers and reinsurers.

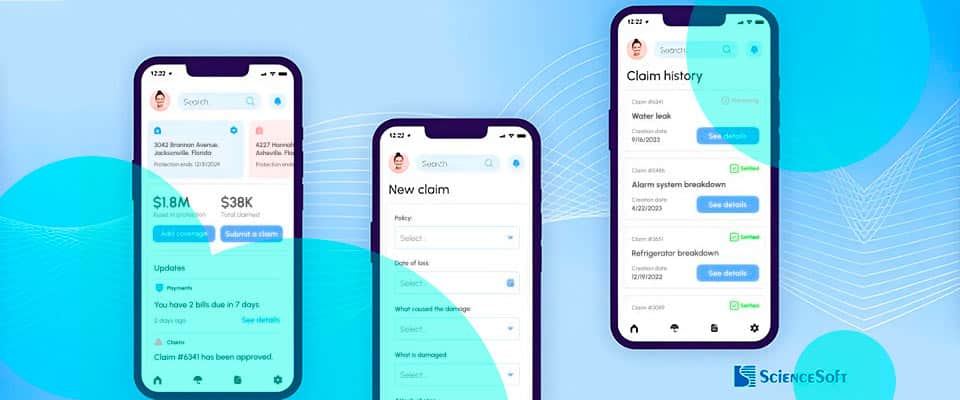

For example, applying real-time data analytics with ScienceSoft draws on their 35+ years of experience, enabling better insights into sales, CRM, underwriting, claim management, financial management, and employee performance.

To implement this comprehensive solution, you should expect anywhere from $100,000 to $1,000,000 and 9-15 months – all based on the solution’s complexity. Once engaged, a business can expect upwards of 300% ROI.

The better a company can target long-term policyholders that pay on time and offer lower risk, the higher the rate of return on each new customer acquisition.

Without real-time data to “green flag” these potential clients, a company only increases the likelihood of paying out to a higher-risk customer.

The Future of Insurance Risk Assessment

Real-time data analytics is revolutionizing how insurers assess risk. Policies are customized and crafted based on information from analytics systems integrated with cloud-based tools, AI/ML technologies, and big data.

These integrations reduce fraudulent claims and optimize underwriting so customers are served accurately, and companies reduce losses.

The best way for a provider to remain competitive in the current marketplace is to integrate real-time data solutions to detect higher-risk policies as quickly as possible.

FAQ

It usually depends on the provider. Customer demographics and historical health results may be more important for life insurance, while real-time telematics and wearable technology benefit a car insurer.

The human brain is capable of impressive calculations, but is not as scalable as AI-powered models. These systems can better identify anomalies in claims data, flagging fraudulent patterns in real-time.

It helps detect high-risk policies, reduces fraud, and improves underwriting accuracy, leading to better financial stability.

Yes and no. Creating a “built from scratch” model may be cost-prohibitive, but using a service that is tailored to the provider will offer more than financial benefits. A cost-benefit analysis is the best way to determine a company’s tool acquisition budget.

Privacy and security are the two primary concerns. Aligning real-time data analytics with regulations like HIPAA while reducing the risk of data leakage to the company is imperative to success.

Training personnel and slowly rolling out new technologies with internal teams and external customers ensures wider acceptance of change.

Data security, high implementation costs, regulatory compliance, and the complexity of integrating new systems.

By leveraging AI-driven automation, predictive modeling, and scalable cloud solutions to optimize operations and reduce losses.

………………….

AUTHOR: Olga Vinichuk, Business Analyst and Insurance IT Consultant at ScienceSoft