Azos, an insurtech focused on individual life insurance, has raised R$125 mn ($23.8 mn) to grow in a market that remains highly concentrated and still dominated by Bradesco and Prudential.

The Series C round was led by Kaszek and Kevin Efrusy, an early Facebook investor who later served on the company’s board.

Both Kaszek and Efrusy were already on the cap table. Kaszek joined in the seed round and followed with participation in every later raise. Efrusy joined in the Series B round a year ago, though with a smaller check.

Azos still had a meaningful portion of its Series B capital on hand. Even so, the company chose to raise again to accelerate its artificial intelligence projects.

The world is at an inflection point, according to co-founder and CEO Rafael Cló. He told Brazil Journal that traditional insurers remain behind in rolling out AI-based solutions. He said this is the right time to scale those products.

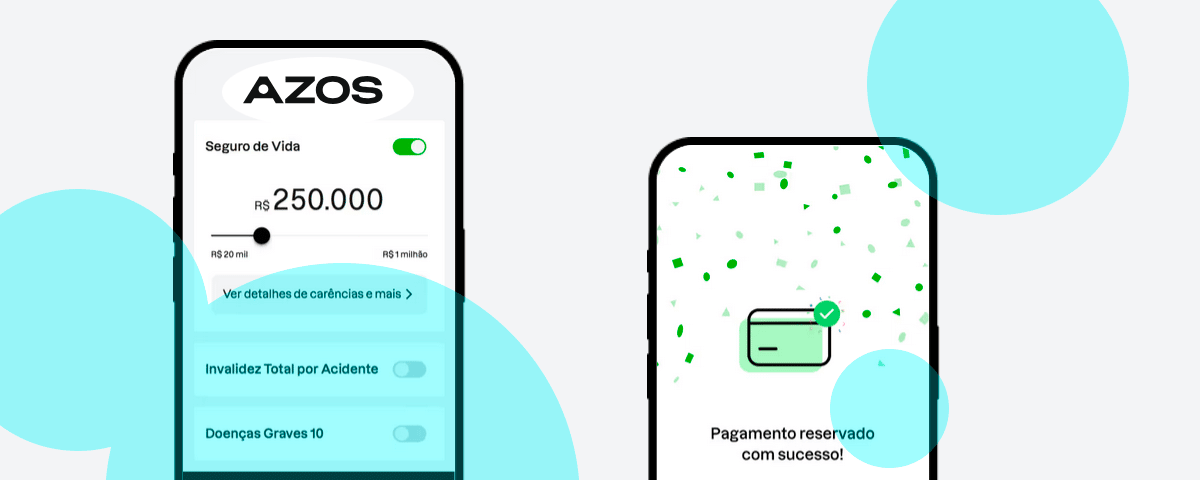

Azos already has several AI initiatives underway. One example is an underwriting tool that uses AI to approve or reject policies within seconds.

Cló said 30% of policies are already approved in just a few seconds. The company wants to raise that figure to 50% by year-end.

The startup is also using AI to process claims. That reduces turnaround time from days to hours. It is also building an AI-based tool to help brokers increase sales.

Other tools focus on customer service and collections. Those systems automate part of the workload and allow the company to grow without expanding teams at the same pace.

Azos was founded in 2020 by Cló, Renato Farias, and Bernardo Ribeiro. The company emerged after Cló went through a drawn-out struggle to reinstate his own life insurance policy after his credit card expired. That experience pushed him to spot a market opportunity.

In the six years since launch, the startup has reached 100,000 active policies and posted R$307 mn in annualized premiums in February.

That gives the company a little more than 1% of Brazil’s individual life insurance market, excluding creditor insurance. That market generated R$25 bn last year and remains dominated by Bradesco and Prudential, which together control 64%.

The startup has 11,000 registered partner brokers and R$110 bn in insured value.

Azos operates under the MGA model, short for managing general agent. It partners with a traditional insurer, Excelsior, which provides the balance sheet and assumes the risk.

That setup removes the need for Azos to secure its own license from Susep.

Azos is mainly responsible for structuring the insurance products it sells, managing customer experience, and pricing risk.

Under this model, the insurer captures all float income. Azos earns revenue in two primary ways. One comes from originating customers. The other comes from pricing risk correctly, which depends largely on claims performance over time.

Cló said Azos is in no rush to obtain its own license. He said other fintech and technology companies show that this kind of transition needs to happen at the right time.

He pointed to Nubank, which only became a regulated bank after 12 years. He said Azos is not rushing that shift because the MGA model is working well for now.

The comparison with Nubank is deliberate. Cló said Azos wants to do in individual life insurance what Nubank did in banking.

That goal will not be easy to achieve. Cló said Azos holds clear product advantages because its policies offer stronger coverage than incumbent products and more competitive pricing.

He also said distribution remains a major challenge. The company needs to win over as many partners as possible and make the brand more familiar to Brazilians so customers trust it.

He added that the business also faces a broader challenge around educating Brazilians on the importance of financial protection.