The Baldwin Group and Nasdaq released their fifth annual 2026 Directors & Officers Benchmarking Report, showing a more stable D&O insurance market after record premium levels in 2022. Baldwin, listed on Nasdaq under BWIN, is an independent insurance brokerage and advisory firm.

The report found that about 54% of companies saw D&O premiums stay within ±10% year-on-year. Another 30% recorded moderate decreases of 10% to 30%, while only 10% saw reductions above 30%.

That distribution points to stabilization rather than continued broad softening. Insurer competition remains, but pricing discipline has returned in parts of the market.

Mike Tomasulo, senior managing partner at The Baldwin Group, said the D&O market has moved into a more balanced environment. He said insurers still compete, especially on excess layers, while primary carriers appear less willing to reduce premiums and retentions without risk data supporting the move.

Sector differences remain visible. Healthcare and technology companies continue to pay some of the highest premiums and retentions, reflecting heavier exposure to securities litigation.

Materials, consumer discretionary, and industrial companies saw some of the largest premium decreases. Those sectors appear to have experienced sharper pricing correction after recent volatility.

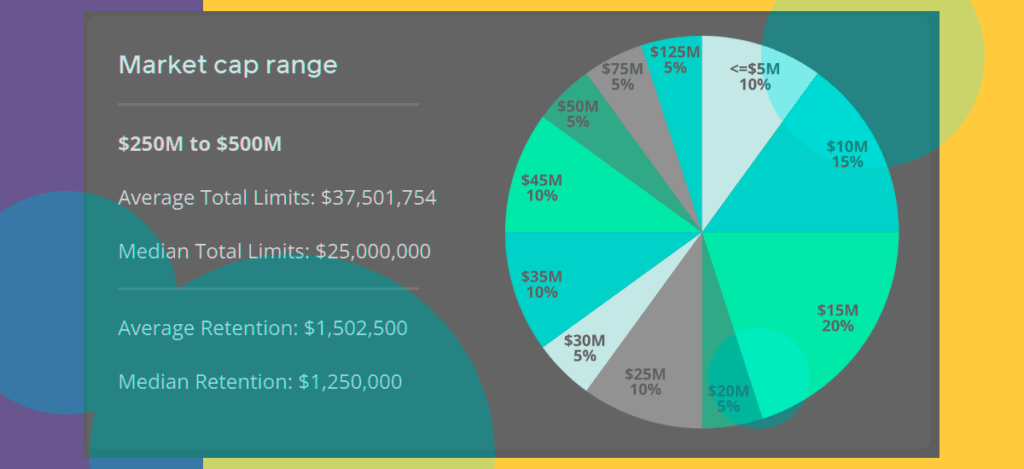

Companies are also changing how they buy D&O limits as pricing pressure eases. The report found average total D&O limits increased to $66 mn in 2026.

Roughly 55% of all companies saw their overall D&O premiums stay within 10% of the previous year. Only 10% of companies enjoyed a rate reduction of over 30%, a drop from almost 13% a year ago.

Most companies that saw significant rate changes were under $500 mn in market cap, as insurers seem to be clearly targeting the micro-cap space more than in previous years.

| Market cap | Significant decrease (> 30%) | Moderate decrease (10% – 30%) | Flat (+/– 10%) | Moderate increase (10% – 30%) | Significant increase (> 30%) |

| $0 – $100M | 11% | 44% | 40% | 4% | 0% |

| $100M – $250M | 29% | 7% | 64% | 0% | 0% |

| $250M – $500M | 14% | 29% | 50% | 7% | 0% |

| $500M – $1B | 0% | 36% | 57% | 7% | 0% |

| $1B – $2.5B | 8% | 31% | 54% | 0% | 8% |

| $2.5B – $5B | 20% | 40% | 40% | 0% | 0% |

| $5B – $10B | 0% | 0% | 86% | 14% | 0% |

| $10B – $50B | 0% | 0% | 100% | 0% | 0% |

| $50B – $250B | 0% | 17% | 67% | 17% | 0% |

| Total | 10% | 30% | 54% | 5% | 1% |

The increase reflects a better pricing environment and a larger share of large-cap buyers in the data. Companies are using improved conditions to reassess program structure and rebuild limits after the hard market cycle.

Future D&O market conditions could depend heavily on capital markets activity.

The report said IPO and de-SPAC activity, often concentrated among companies with $250 mn to $1 bn in market capitalization, has a direct effect on D&O pricing and retentions.

Newly public companies carry higher litigation exposure. If IPO activity continues to recover, it could bring fresh demand into the D&O market.

A sustained increase in public listings could become the next pricing shift for D&O insurers. Growth-stage companies would likely sit near the center of that change.

Tomasulo said companies need to compare D&O programs across pricing, limits, structure, coverage terms, and conditions. He said that helps buyers decide when to use improved market conditions and when to strengthen protection against changing risks.