EU insurance markets could gain from a proposed public-private reinsurance scheme for climate-related losses, according to Fitch Ratings.

As climate risks grow, state-backed reinsurance could help insurers maintain coverage in high-risk areas they might otherwise abandon.

A joint paper from the ECB and the European Insurance and Occupational Pensions Authority in December 2024 outlined the plan. It would strengthen insurers’ financial stability by pooling risks across the EU, improving diversification and reducing volatility (see Largest Reinsurance Companies in Europe).

The model follows the example of Spain’s Consorcio de Compensacion de Seguros (CCS), which has helped stabilize Spain’s insurance market by covering major natural disaster losses. The EU scheme would complement national systems rather than replace them.

The proposal seeks to close the widening insurance protection gap for natural catastrophes. Over 1981-2023, only about 25% of economic losses from natural disasters in the EU were insured, and this figure has been declining.

The new EU strategy on adaptation to climate change highlights the fact that affordability and insurability of natural catastrophes insurance coverage is likely to become an increasing concern.

Research shows that in the past only a quarter of the total losses caused by extreme weather and climate-related events across Europe were insured indicating a large insurance protection gap in Europe.

Improved climate projections provide further evidence that future climate change over the coming decades will increase climate-related extremes (e.g. heavy precipitation, droughts, flood…) and thus the related protection gap, if no measures are taken.

It is therefore key to understand the insurance protection gap and identify where it comes from. EIOPA’s therefore developed a pilot dashboard which shows the insurance protection gaps for many natural catastrophes in Europe.

The scheme would improve access to affordable natural catastrophe insurance while easing the financial strain on governments from uninsured losses.

It would provide a financial cushion for insurers and support post-disaster economic recovery. Risk-based premiums from insurers, reinsurers, or national schemes would fund the initiative.

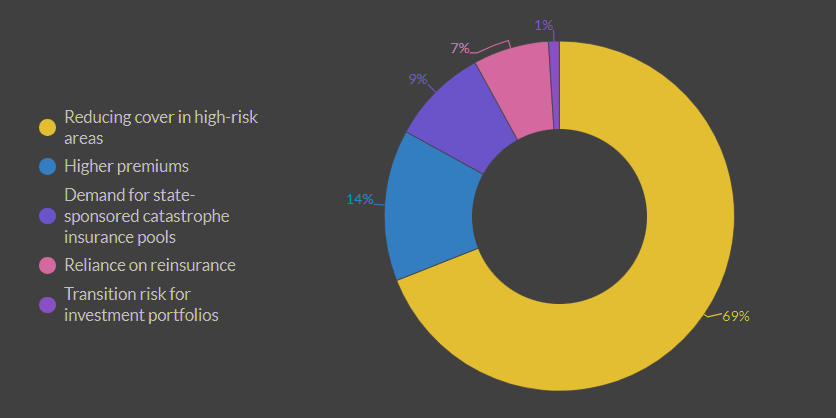

What Will Be the Most Imminent Impact of Climate Change for the Insurance Industry in 2025?

A related proposal includes an EU public disaster risk management fund, financed by member states, to rebuild public infrastructure after disasters. Payouts would be conditional on countries implementing agreed risk mitigation measures.

This combination of reinsurance and public financing aims to reduce macroeconomic and financial risks from uninsured losses by clearly defining public and private sector responsibilities. It also encourages risk reduction at both national and EU levels.

A major challenge remains the affordability and availability of insurance in high-risk areas. Without strong state-backed reinsurance, insurers will likely cut coverage in these regions.

At Fitch’s recent Insurance Insights event in London, 69% of participants in a poll said reducing coverage in high-risk areas would be the most immediate impact of climate change on the sector in 2025.

This concern reinforces the need for state-backed reinsurance to keep insurance accessible and affordable. The floods in Spain in November 2024 showed the effectiveness of state-backed schemes, as the CCS helped stabilize the market by covering flood-related damages.