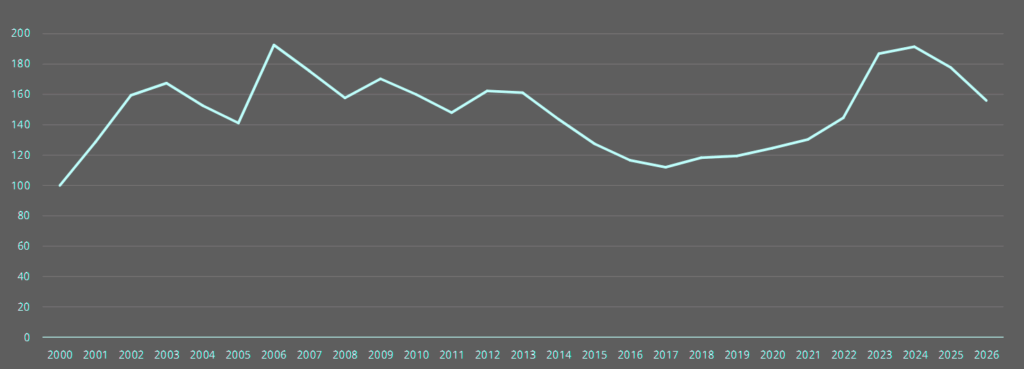

Guy Carpenter says its Global Property Catastrophe Rate on Line Index fell 12% at the Jan. 1, 2026 renewals, with per-risk placements ranging from flat to down as much as 15%, depending on geography.

In its Jan. 1, 2026 Reinsurance Renewal Report, the broker points to persistently high attachment points as a central driver. Reinsurers continue to shoulder a smaller share of catastrophe losses.

That reality, combined with ample capacity, pushed pricing into clear double-digit declines across global catastrophe programs.

In the U.S., the property catastrophe ROL index dropped 12%. North American cedants pressed hard on price and kept reshaping panels, spreading placements more widely rather than leaning on a few markets.

Global Property Catastrophe Rate on Line Index

Savings on core layers didn’t sit idle. Many buyers redeployed them to broaden coverage and refine risk transfer structures.

Europe moved even faster. The regional property catastrophe ROL index fell 15%. At the same time, market participation narrowed.

Clients leaned toward smaller, more focused panels and took a tighter grip on price discovery. Fewer markets, sharper conversations.

Asia Pacific followed a similar pricing path, though the mechanics differed. Loss-free catastrophe excess of loss programs saw double-digit reductions. Reinsurers showed flexibility, often stretching to meet client targets in order to secure line size. Share mattered more than margin.

At Jan. 1, retentions held broadly steady. Demand nudged higher, and that translated into larger total limits placed rather than higher attachment points. Buyers weren’t retreating from risk. They were buying smarter.

Guy Carpenter says some cedants used anticipated savings for add-on protection. Ancillary covers gained traction under favourable conditions, especially where underwriting income faced volatility.

In North America, that meant new placements for underlying catastrophe cover, aggregate XoL, and subsequent event protection.

Europe showed a different nuance. Appetite for aggregate or frequency-based protection is returning, slowly, from near-zero levels after 2023.

Reinstatement premium protection is also back in play for some buyers. In the Middle East and Africa, structures stayed largely unchanged, though cedants pushed for more underwriting capacity rather than structural overhaul.

Across regions, buyers typically sought 5–10% additional limit. About half of that demand went toward traditional capacity.

The rest flowed into aggregate products, catastrophe quota share, or alternative structures.

Capacity wasn’t a constraint. Reinsurers easily met demand for limit, and excess capacity remained a defining feature. Preliminary estimates put surplus capacity above 25% at Jan. 1. That cushion shaped negotiations from the start.

Terms and conditions eased as well. Guy Carpenter reports improved contract concurrency across most regions.

In the U.S., the bulk of non-concurrencies introduced during the 2023 hard market were removed. Coverage language aligned again.

Europe showed similar movement. After a 55% year-over-year jump in unique subjectivities at Jan. 1, 2023, clients have steadily pushed back.

From Jan. 1, 2025 onward, that pressure drove a return toward full-market concurrency, cutting unique subjectivities by about 25% from their 2024 peak.

According to Beinsure analysts, the Jan. 1 outcome reflects a market where capital is plentiful, loss participation is contained, and buyers are once again setting the tone. Pricing softened. Structures adjusted. Discipline now gets tested on the next loss cycle.