Artificial intelligence, cyber insurance, and climate-driven catastrophe risk will shape the insurance market more than any other forces in 2026, according to new projections from GlobalData. The forecast comes from the firm’s annual outlook on insurance sector trends, released this month.

Insurers that manage to lead on these three fronts should see stronger results, better products, and sharper customer outcomes

Ben Carey-Evans, senior insurance analyst at GlobalData

He described AI as the dominant technology theme in insurance right now. No real debate there.

What changed in 2025 was speed. The rise of so-called agentic AI pushed the technology beyond automation and into live decision-making.

These systems react to real-time inputs and make judgement-like choices, which is why their influence is already visible across underwriting, claims, and distribution. Carey-Evans expects that effect to accelerate in 2026. Fast.

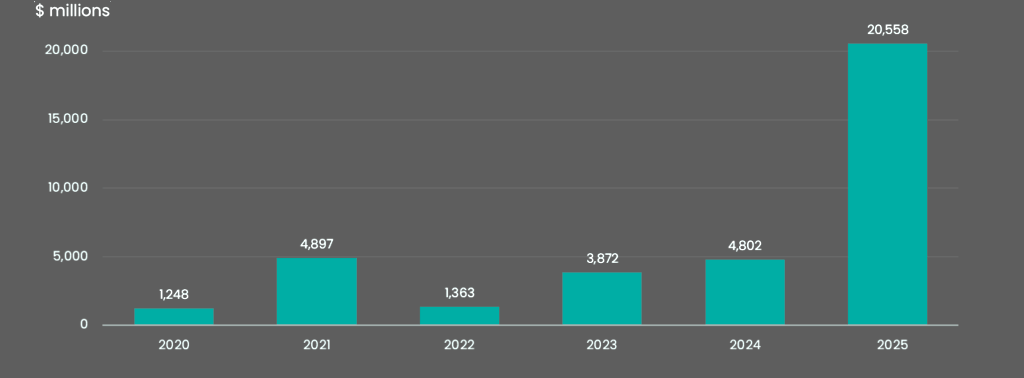

Deal activity followed the hype, then outpaced it. The total value of AI-focused M&A in insurance jumped 328% in 2025, while deal volume rose 125%.

Generative AI played a role, but agentic AI drove much of the interest. GlobalData said the same pattern showed up across its transaction, jobs, and company filings databases.

Value of deals completed within AI in insurance

As generative AI changes the way companies do business, it is creating new risks and new causes of loss that impact not only the companies themselves but also their business partners such as third-party vendors and digital supply chains.

The analysis highlights AI’s potential to amplify systemic risks, such as through polymorphic malware or AI-targeted data breaches, while also providing a framework to quantify these emerging threats.

Leveraging the cyber kill chain model, the report underscores the urgency for insurers to adapt to AI-driven threats, balancing innovation with robust risk mitigation strategies.

Generative artificial intelligence is considered one of the most important technological breakthroughs of the last few decades. Munich Re Group sees great opportunities for insurers – if they explore the possibilities of the new technology and understand its risks.

There are many ways organizations could revolutionize their respective industries by applying Gen AI to routine business functions. For example, in insurance, Gen AI can assist underwriters evaluating risks by analyzing vast amounts of data, including historical claims, customer information and internal/external cybersecurity factors.

Hiring and disclosure trends point the same way. AI capability has moved from experimentation to priority spend. Munich Re’s July 2025 acquisition of Next Insurance, a tech-first commercial P&C carrier built around automation and data-heavy underwriting.

Cyber insurance remains the second major growth engine. GlobalData expects momentum to run through at least 2030. The firm pegs the global cyber insurance market at $22.2bn in 2025, climbing to $35.4bn by the end of the decade. Loss volatility hasn’t scared buyers off. If anything, it’s pulled more in.

Climate risk rounds out the list, and it’s the least abstract. More severe weather, more frequent disasters, higher losses.

Natural catastrophe insurance continues to see sharp annual increases in premiums and claims, trends GlobalData expects to persist. Fire, flood, wind. Pick your poison.

Carey-Evans warned that rising severity creates a structural problem. Large regions are edging toward uninsurability, especially in hazard-exposed areas. That hits consumers first, but insurers feel it quickly through capital strain and retreating capacity.

According to Beinsure analysts, climate risk isn’t just another line item anymore. It’s forcing insurers to rethink where they write business at all.

Put together, the three themes aren’t isolated. AI shapes how insurers price and manage cyber and climate risk. Cyber loss patterns test capital models. Climate volatility stresses underwriting assumptions.

In 2026, insurers that can connect those dots move ahead. The rest tread water.