Overview

Hong Kong Insurance Authority is reviewing its risk-based capital framework, with proposals that reach into areas insurers haven’t formally dealt with before, including stablecoins and crypto assets.

The work aims to keep the regime competitive while supporting the insurance sector and broader economic activity, according to the regulator.

The review also looks at capital incentives tied to eligible infrastructure investments. The regulator says these incentives would help insurers diversify risk and channel capital toward targeted projects, with a clear nod to local infrastructure development. It’s a pragmatic angle. Less theory, more balance sheet behaviour, Beinsure noted in December.

Capital treatment sits at the centre of the exercise. The authority says it is studying how recent regulatory developments, including frameworks for specified stablecoins and crypto assets, should feed into capital requirements.

The stated goal is to build a framework that benchmarks against other domestic and international capital regimes. Industry feedback is being gathered now, with public consultation planned later.

The tone suggests openness, not a done deal.

The backdrop matters. Hong Kong’s RBC regime only went live on 1 July 2024, following the Insurance (Amendment) Ordinance 2023 and related rules and guidelines.

Capital Quality

| Capital Tier | Capital Base Composition Limit |

|---|---|

| Unlimited Tier 1 capital | No limit |

| Limited Tier 1 capital | Limited to 10% of the prescribed capital amount (“PCA”) |

| Tier 2 capital | Limited to 50% of the PCA |

The framework uses a three-pillar structure and an assessment approach that reacts to how well insurers match assets and liabilities, how much risk they take, and what kinds of products they write. Strong risk management translates into lower capital pressure. Weak controls don’t.

Capital Requirements

From cryptocurrencies to Non-Fungible Tokens (NFTs) – the crypto assets market is growing. From an underwriting perspective, crypto assets may lead to unexpected losses and opportunities for new forms of insurance coverage, according to Beinsure’s Underwriting Crypto Assets report.

Insurance covers damage inflicted by unpredictable events, and cryptocurrency insurance is no different.

Highly volatile cryptocurrency often makes headlines as the target of multimillion-dollar hacks, leading to investors losing millions and the sector shedding billions.

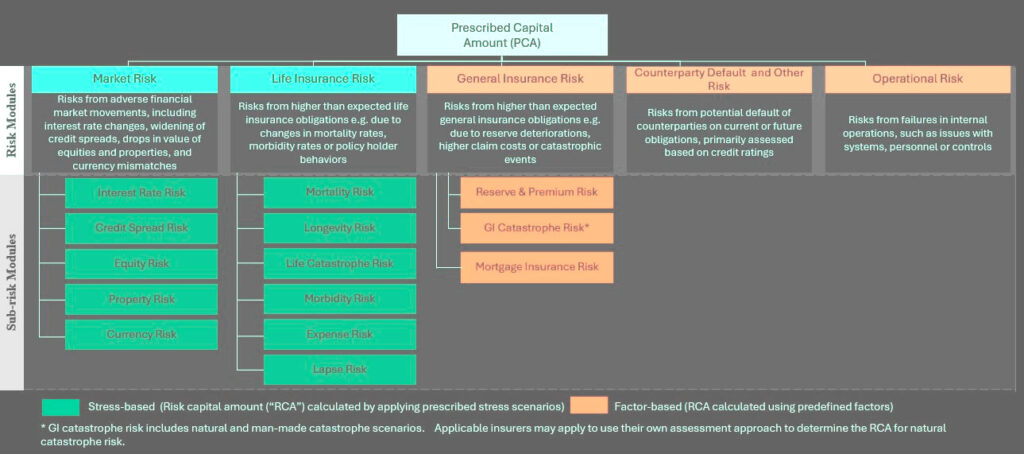

Pillar 1 covers the numbers

Assets and liabilities must be valued on a market-consistent basis under the Insurance (Valuation and Capital) Rules. Capital quality is split into tiers, with limits designed to keep buffers credible. Unlimited Tier 1 carries no cap.

Limited Tier 1 is capped at 10% of the prescribed capital amount. Tier 2 can make up to 50% of that amount.

The capital base must sit above the prescribed capital amount, the minimum capital amount, and HK$20 mn, with carve-outs for marine insurers, captives, special purpose insurers, and Lloyd’s.

Risk charges under Pillar 1 span market risk, life and general insurance risk, counterparty default, operational risk, and other exposures, with diversification benefits factored in. Dedicated rules apply to marine insurers, captives, and Lloyd’s operations, which keeps the system flexible rather than blunt.

Pillar 2 shifts to judgement and process

The authority rolled out its enterprise risk management guideline, requiring insurers to identify and manage risks actively and to run an own risk and solvency assessment at least once a year. ORSA reports go straight to the regulator. No shortcuts there.

Pillar 3 deals with reporting and disclosure

Insurers must submit financial statements, regulatory returns, audit reports, and actuarial reviews under detailed submission rules. Public disclosure requirements are still being shaped and will come back to the market for consultation.

We think the timing of the review says as much as the content. The RBC regime is barely out of the gate, yet the regulator is already stress-testing it against new asset classes and investment patterns.

Stablecoins and crypto might remain niche for insurers, or they might not. The authority appears determined to be ready either way.