Overview

Cyberattacks on companies, governmental entities, and research institutions often dominate media coverage, but cyber-threats to private individuals are also significant. Hackers and their criminal activities increasingly target personal digital lives, making individual protection essential, according to Munich Re’s Global Cyber Risk Survey 2024.

While the overall economic losses from cyberattacks on private persons are generally lower compared to those affecting companies, the impact on individuals can be just as severe. The personal damage can be existential or, at the very least, painful. Therefore, mitigative and protective measures such as cyber insurance and robust personal digital hygiene should be fundamental requirements for anyone going online.

The survey, with over 7,500 respondents from 15 countries, provides a comprehensive overview of the current state of personal cybersecurity and the role of insurance in mitigating these risks

The survey reveals a heightened awareness of cyber threats among individuals. Only 12% of respondents reported being unconcerned about their digital security, while a significant 53% expressed concern or extreme concern about their digital safety.

This growing anxiety is a reflection of the increasing cyberattacks targeting personal digital lives, not just corporations and institutions.

The cyber threat landscape for private individuals

Personal cyber insurance can help you recover from data breaches, online fraud, cyberbullying and other cybercrimes. Say you click on a link in an email that installs malicious software on your computer, giving a hacker access to your data.

Personal cyber insurance could reimburse you for professional IT services to recover your data or even help you pay a ransom if the hacker holds your files hostage.

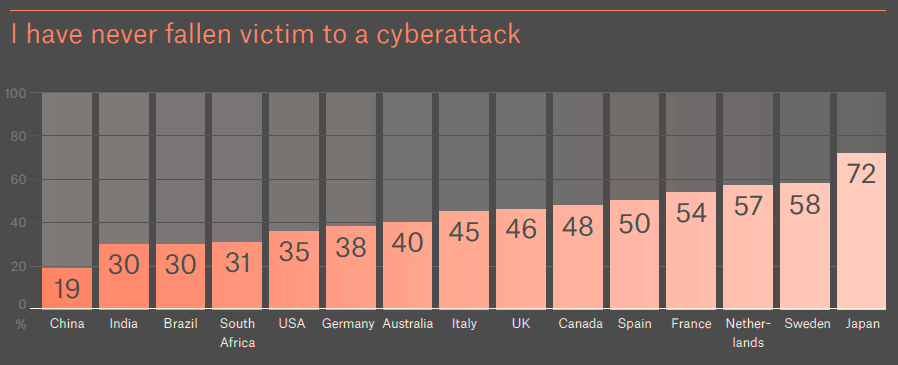

The high level of concern is understandable, with 57% of respondents stating that they have already been the victims of cyberattacks in their private lives.

Online fraud and malware, often distributed via phishing emails, were the most common types of attacks, with increases observed in all attack categories compared to 2021.

In a world where our digital lives are increasingly intertwined with our personal and professional activities, safeguarding personal digital security is paramount.

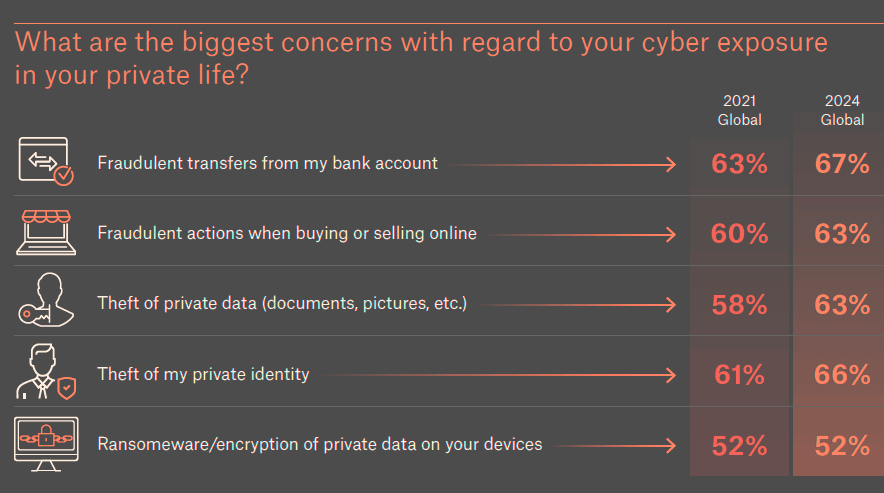

What are the biggest concerns with regard to your cyber exposure in your private life?

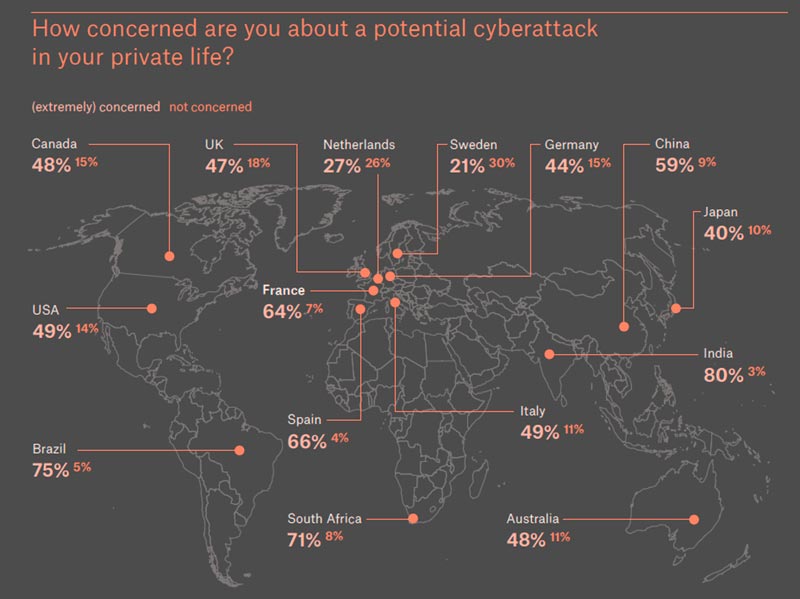

Looking at the different countries, there is a considerable divide in the question whether the survey participants have already been affected by a cyberattack and cyber risk detection.

Whereas a large majority already has become victim of cyberattacks in China, India, Brazil, South Africa and the USA, this proportion is significantly lower in Japan.

Cyberattacks on private individuals and their families

Despite significant concern, there remains a considerable gap in understanding how cyber insurance can enhance personal digital security. Many individuals underestimate threats affecting them and their families, highlighting the need for better education and awareness about cyber insurance solutions.

Cyber security and the level of protection

Surprisingly, Japan is the country where only 5% of the respondents rated their personal cyber security status as “very good”, indicating significant room for improvement.

Equally striking is that India (35%) and China (20%) have the highest percentages of respondents feeling very well protected, despite these countries having the highest rates of cyber-attack victims.

The potential for improving personal cyber security becomes evident when considering the low number of respondents who rated their protection as “very good” overall: just 14%.

86% of respondents acknowledge that they are not fully protected, with the majority rating their own cyber security as merely “average”.

Concrete Steps to Improve Personal Cyber Security

The high global threat level and often inadequate personal cyber security necessitate significant improvements. What specific actions can individuals or families take to enhance their cyber security? Cyber insurance solutions with affiliated services are crucial here.

A 2021 survey revealed a strong demand for additional protective measures and assistance.

Only 10% of respondents stated they did not need any precautionary services, and only 12% said they did not require assistive services in the event of a cyberattack.

Over half of the respondents consider preventive services like firewalls, anti-malware tools, and backups valuable components of a cyber policy. For post-crisis measures, data recovery, help hotlines, and legal advice ranked as the top three services valued by interviewees. The need for post-incident services has slightly increased year-over-year across all measures.

Cyber insurance to protect private digital footprint

A cyber insurance policy leverages many essential services in addition to risk transfer. The ultimate goal is to strengthen private cyber resiliency and preparedness, protecting individual digital assets and preventing online fraud.

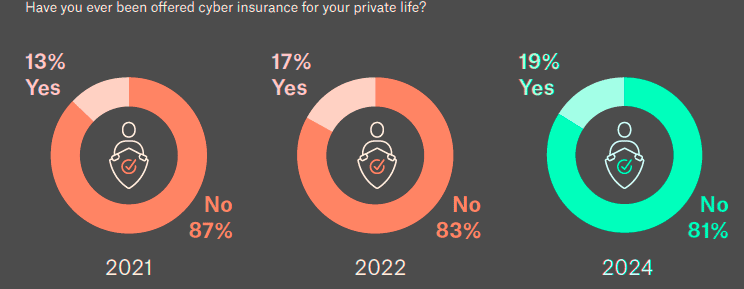

It is encouraging to note that the proportion of individuals offered private cyber insurance has increased significantly between 2021 and 2024.

Personal cyber insurance offering

Despite the high level of concern about becoming a victim of a cyberattack, the understanding of how cyber insurance can enhance personal digital security remains disproportionately low. Many individuals continue to underestimate the cyberthreats that affect them and their families directly.

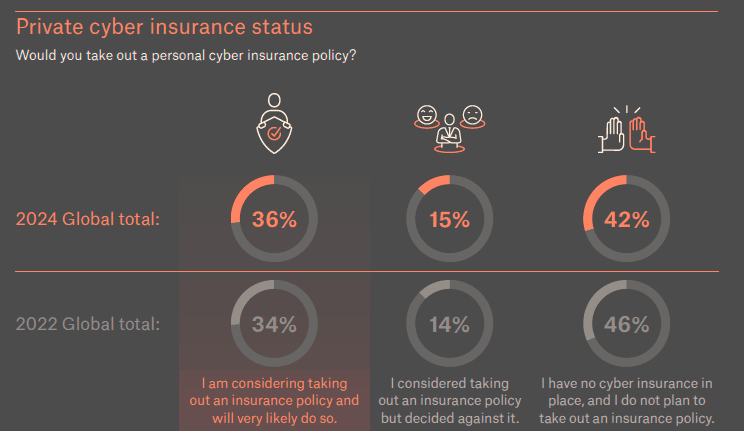

Private cyber insurance adoption

The survey highlights a slow but steady increase in the adoption of private cyber insurance.

In 2024, 19% of respondents reported being offered cyber insurance for their private lives, up from 17% in 2022 and 13% in 2021.

However, 42% still have no intention of purchasing such insurance, emphasizing the need for the insurance industry to enhance transparency and simplify offerings to make the benefits more apparent.

What personal cyber insurance covers?

Personal cyber insurance policies vary, but they generally cover:

- Cyberattacks: Coverage includes costs to restore systems and recover data if malware infects your laptop or someone hacks your home network.

- Cyber Extortion: This covers ransom payments if someone holds your computer access, files, or other data hostage. The policy offers professional assistance to evaluate and respond to threats, reimbursing the ransom up to the coverage limit if the threat is credible.

- Online Fraud or Identity Theft: Coverage may include illegal bank or credit card transfers, counterfeit money, check forgery, or phishing attacks. Some insurers offer identity theft insurance separately, while others combine it with personal cyber coverage.

- Data Breaches: If someone steals your personal information, publishes it online, or posts false information about you, the policy can cover legal fees, lost wages, and a forensic IT review to identify the breach.

- Cyberbullying: If you or your child face online harassment, the policy can reimburse expenses for counseling, temporary relocation, private tutoring, or social media monitoring.

- Deceptive Transfer Fraud: If you mistakenly send money to a criminal, thinking you are helping a family member or paying a legitimate company, the policy can reimburse the lost funds.

Note that insurance generally covers only new events. You cannot buy a policy after a cyber incident to clean up the problem.

Cyber scenarios where personal cyber insurance can help

- Online Shopping Fraud: You find a website offering the latest smartphone at an unbelievably low price. Excited, you make the purchase but soon realize the site was a scam. You never receive the phone, and your money is gone. This scenario is common as fake websites proliferate, tricking individuals with attractive offers and leaving them with empty wallets.

- Theft of Funds: Imagine waking up to find your bank account drained. Cybercriminals phished your email, captured your login details, and accessed your bank account. They made multiple unauthorized transactions, leaving you scrambling to recover your money. Innocent-looking emails or links can turn a regular day into a financial nightmare.

- Identity Theft: Discovering that someone has opened credit card accounts, taken out loans, and even bought a car using your personal information is shocking. Cybercriminals stole your social security number and other personal details, wreaking havoc on your financial life. Reclaiming your identity involves endless paperwork, legal battles, and a heavy emotional toll, affecting your sense of security and peace of mind.

According to Munich Re’s survey, 42% of the survey participants have no intention of purchasing personal cyber insurance for their private lives.

For the insurance industry, these results underscore the importance of enhancing cyber risk transparency, better explaining the offering and the benefits from holistic insurance solutions, and further improving the sales process.

The insurance industry needs to ensure that the 36% who are interested receive appropriate insurance coverages and services. In addition to that further efforts are necessary to convince the ones who are not showing interest in cyber insu-rance so far.

Positive outlook on cyber Protection and Insurance

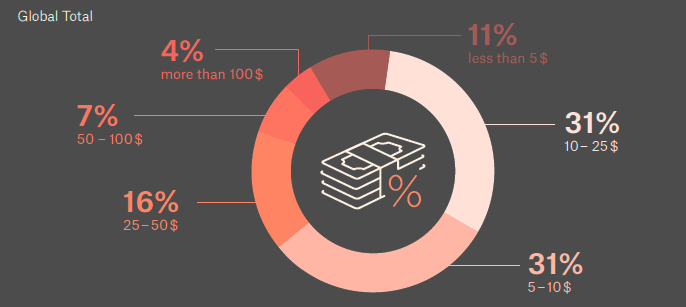

Many interviewees recognize the value and cost of mitigating and protecting against online fraud and cyberattacks. The price is not a major obstacle.

Nearly one-third (31%) of surveyed individuals are willing to pay $5-$10 per month to enhance their and their family’s cyber resilience through cyber insurance and affiliated services.

An equal percentage consider $10-$25 a reasonable range. Most personal cyber insurance products fall within this range, suggesting that the protection gap is likely to close further in the future.

How much are you willing to pay per month for increased cyber resilience through cyber insurance and affiliated services?

Personal cyber insurance is essential for protecting against the financial impact of hacking and online fraud. It is often complemented by comprehensive security support, such as 24/7 hotlines and data recovery assistance.

Security for privacy and family comes at a cost, but the survey shows that respondents are willing to pay a reasonable amount for it. This willingness allows insurance companies to demonstrate the concrete benefits of cyber insurance policies effectively.

Survey Methodology

The survey was conducted by Munich Re, in partnership with Statista, and covered 15 countries, including Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, the Netherlands, South Africa, Spain, Sweden, the UK, and the USA.

Over 7,500 participants provided globally and nationally representative results, with a focus on both commercial and private sectors. The respondent pool included a mix of C-Level executives and employees.

Company sizes varied, with 8% having 1-9 employees, 33% having 10-249 employees, 29% having 250-2499 employees, and 27% having more than 2500 employees. Annual revenues ranged widely, with 13% of companies earning over $1 mn, 30% between $1 mn and $200 mn, 14% between $200 mn and $1 bn, 10% between $1 bn and $5 bn, and 7% earning more than $5 bn.

The survey included various industries: 15% from consumer products and services, 21% from information technology, 9% from finance, 8% from transportation, communication, and utilities, 13% from industry and manufacturing, 9% from education, 7% from healthcare and pharma, 6% from public authority and defense, and 11% from other sectors.

……………….

AUTHORS: Martin Kreuzer – Senior Risk Manager Cyber Risks at Munich Re, Axel von dem Knesebeck – Corporate Underwriting Cyber at Munich Re