AI has become one of the strongest technologies in cyber insurance. It improves pricing, underwriting and threat detection, but it also gives attackers cheaper tools, faster workflows and better social engineering.

According to Beinsure, cyber insurers now face a difficult trade-off. The same systems that help carriers detect fraud, process documents and assess risk also help criminals write phishing emails, clone voices and automate attacks at scale.

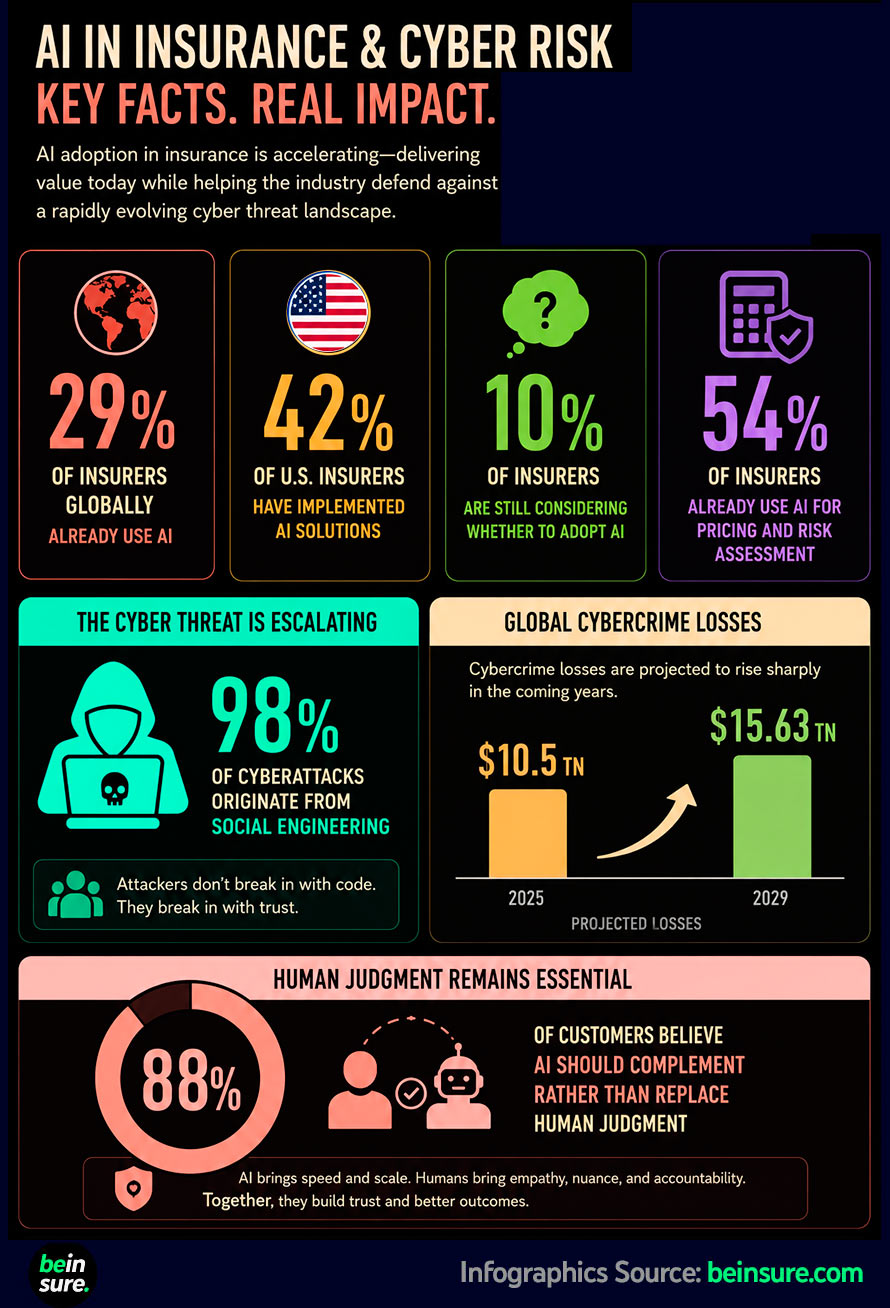

Adoption is already well advanced. Around 29% of insurers globally use AI, while 42% of U.S. insurers have implemented AI solutions. Only 10% still remain in the decision stage, which means the market has already moved beyond early testing.

Pricing and risk assessment sit near the front of adoption. Around 54% of insurers already use AI in those areas, where faster data analysis helps carriers review exposures, identify weak signals and update risk views with less manual work.

The operational benefits are clear. AI improves threat detection, fraud identification, underwriting efficiency, customer communications and document processing. It helps teams handle more information without adding the same level of staffing cost.

That advantage matters in cyber insurance because the risk changes faster than most traditional insurance lines. New attack methods spread quickly, and yesterday’s underwriting assumptions get stale. Slow manual review leaves insurers exposed.

Attackers are moving just as fast. AI supports phishing campaigns, deepfake fraud, social engineering, vulnerability discovery, malware deployment and attack automation. The cost of launching sophisticated attacks is falling, which changes the economics of cybercrime.

Social engineering remains the main problem. Around 98% of cyberattacks originate from social engineering, where criminals exploit human behavior rather than only technical weakness. AI makes those attacks cleaner, more personalized and harder to spot.

The loss numbers explain why insurers are paying attention. Global cybercrime losses are expected to reach $10.5 tn in 2025 and could grow to $15.63 tn by 2029. Those figures put pressure on underwriting, pricing, accumulation control and reinsurance capacity.

According to Beinsure analysts, cyber insurers should treat AI as both an underwriting tool and a source of new aggregation risk. If the same models, vendors or detection systems spread across many firms, one weakness could create market-wide exposure.

Customer expectations also set limits. 88% of customers believe AI should complement human judgment rather than replace it. That matters in claims, fraud review and coverage decisions, where trust breaks quickly when automated decisions look unfair or opaque.

Insurers need stronger governance, better model controls, cleaner data and clear accountability when AI enters pricing, claims and risk selection.

……………….

AUTHOR: Oleg Parashchak – CEO & Founder of Finance Media Holding