Overview

Life insurers across Europe are grinding through one of the toughest investment climates in decades. Inflation keeps punching through forecasts, market cycles flip faster than models can adjust, and Solvency II – plus the new Solvency UK rules – keeps rewriting the capital playbook.

Everyone’s talking about tightening Asset-Liability Management, but too many still cling to basic spreadsheet setups that belong to another era.

Ortec Finance just dropped a report dissecting this gap. The company, known for risk and return tech, argues that old-school SAA models can’t keep up. Beinsure analyzed the report and highlighted key trends.

Key Highlights

- Insurers still using static, deterministic SAA models face rising risk blind spots. Markets have outgrown one-path projections, demanding dynamic tools that handle volatility and shifting capital rules.

- Thousands of simulated economic paths expose full distributions of outcomes – from tail risks to liquidity shocks – giving management a live view of balance sheet behaviour under stress.

- Advanced ALM frameworks integrate Solvency II capital charges directly into investment strategy, helping insurers identify assets that boost returns while consuming less capital.

- Scenario-Based Machine Learning (SBML) models capture complex, non-linear relationships across asset classes and liabilities, delivering a more realistic and adaptive view of portfolio performance.

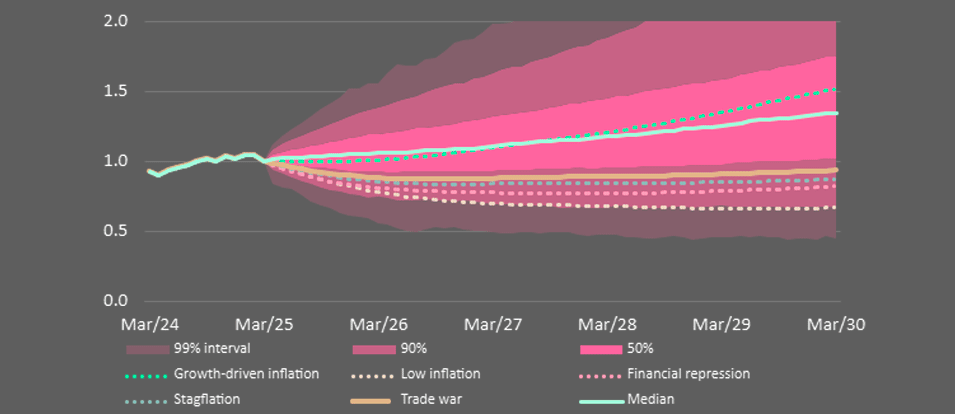

- Insurers can now model bespoke “what-if” worlds – trade wars, stagflation, climate disruption – to test competing economic views and guide decisions in an unpredictable market.

They miss non-linear effects, ignore multiple investment objectives, and fall short when regulatory capital formulas shift midstream.

We think that’s fair. Actuarial teams already use advanced simulations for liabilities, so why keep treating the asset side like a side project.

As portfolios tilt toward private credit, infrastructure, and alternatives, the cracks widen. These assets add yield and spice up diversification, sure, but they also come with headaches – messy cash flows, low liquidity, tricky valuations.

Without heavy-duty ALM engines, insurers risk misjudging stress outcomes. That’s not just bad optics. It warps solvency calculations and eats into capital efficiency.

Sophisticated ALM frameworks – from traditional stochastic simulations to emerging optimization techniques like Scenario-Based Machine Learning (SBML) – give insurers the ability to capture complexity, optimise capital, and align investment strategy with evolving liabilities.

For insurers, the call to action is clear: reassess your ALM processes today. Inertia may feel comfortable, but the firms that embrace advanced modelling now will secure an edge – stronger solvency, greater flexibility to write business, and the confidence to innovate in an uncertain world.

Insurers need to implement more advanced ALM models

To thrive, insurers must look beyond spreadsheets to adopt more advanced ALM models that can capture non-linear risks, optimise across multiple objectives, and support long-term resilience.

Insurers are already accustomed to using sophisticated, model-based approaches on the actuarial valuation side of the business – so it is both logical and timely to bring a similar level of sophistication to asset-focused modelling.

Global insurers are diversifying into private credit, infrastructure, and other alternative asset classes in search of yield and diversification. Surveys consistently show an upward trend in allocations to private markets.

These assets bring unique challenges: illiquidity, irregular cash flows, and default risk. Subtle differences like these can tilt the balance of asset allocation decisions significantly – but they are often missed when relying on simplistic spreadsheet-based tools.

Without advanced modelling, insurers risk misjudging how alternatives perform across different economic cycles, leading to mismatches between assets and liabilities that only surface under stress. This naturally leads to the question of capital optimisation.

Capital optimisation drives survival now

Insurers’ investment strategy is not only about generating returns, but also about managing regulatory capital efficiently.

Solvency II requires insurers to hold additional capital to protect against investment risks and the amount is dependent on the types of assets held, and therefore it can materially affect asset allocation choices.

This further emphasises the need to optimize capital efficiency through investment decision-making. One must also be cognisant of the developments in capital frameworks.

For example, under Solvency II, the matching adjustment allows insurers to adjust the discount rate based on assets held and particularly favours fixed income assets. The use of sub-investment grade bonds and highly predictable cashflow assets can further benefit insurers.

Under Solvency II, every asset class carries a capital hit, shaping how portfolios are built.

Sophisticated ALM models bake those rules into the optimisation process itself. The outcome? A cleaner balance between regulatory load and return targets.

Some insurers, according to our analysts, already pinpoint high-yield, low-capital-consumption assets this way – freeing capital for expansion, dividends, maybe even bold new bets.

Stochastic modelling takes this further

Stochastic models elevate this further by stress-testing capital ratios under a wide range of market conditions, giving management a clear view of trade-offs and ensuring that balance sheet resilience is never compromised in the pursuit of yield.

Thousands of economic paths run through these systems, each testing how solvency ratios twist under shocks or slow burns. Inflation spikes, liquidity crunches, even political gridlock scenarios – the models push them all.

The idea isn’t just safety. It’s to know where the cliff edge actually is before the market makes you find it.

And the uncertainty isn’t easing. Interest rates still drift. Private and public markets decouple more each quarter. Inflation stories split by region.

Through scenario testing, advanced ALM setups let insurers sketch alternate futures, compare them, and plan for what’s plausible, not just what’s tidy.

Insurers turn to narrative-driven ALM for market uncertainty

Markets can’t agree on much right now. Inflation looks sticky to some, fading to others. Interest rates might stay high for years or crash sooner than expected. Private assets, once the golden ticket, now face questions about pricing, transparency, and liquidity.

For insurers, these aren’t just theoretical debates – they rewrite solvency models, product guarantees, and yield expectations in real time.

That’s why flexible scenario testing matters. Advanced ALM systems let insurers throw conflicting forecasts into structured simulations. They can impose alternate market views across timelines, tweak assumptions, and watch how each vision reshapes the balance sheet.

It’s a way to stress-test belief systems, not just portfolios. Management gets a clearer picture of which strategies hold up and which crumble when markets turn weird.

But the real magic sits in narrative-driven analysis. Forget neat historical averages.

Insurers can now craft their own “what-if” worlds – trade wars cutting supply chains to pieces, stagflation grinding growth into dust, or climate shocks pulling liquidity from entire sectors.

Each scenario runs deep, connecting macro chaos to capital positions and solvency buffers.

Insurers shift from deterministic models to SBML for ALM precision

A big flaw in basic SAA setups is their love of simplicity. They pick one path, one forecast, one tidy story. Deterministic by design, they pretend the world runs in straight lines. It’s clean on paper – and wildly misleading in practice.

Real markets don’t behave that way. Inflation jumps, spreads shift, credit melts or rebounds. Stochastic modelling fixes that by running thousands of possible futures, each with its own twists.

You get a full spread of outcomes – not just the shiny mean, but the tails, the liquidity squeezes, the capital strain. Management can actually see how the balance sheet breathes under chaos, not just under ideal math.

Compare the two and the difference is brutal

Deterministic models draw a single “best guess” line, calm and centered. Stochastic ones throw a fan of outcomes on the screen – messy, unpredictable, alive.

That chaos is reality, and it’s where solvency gets tested. Still, even the smartest stochastic frameworks hit a wall. The markets insurers play in now are nonlinear beasts.

Private credit, structured products, hybrid guarantees – all moving in strange, correlated ways. Old optimisation logic can’t keep up.

That’s where Scenario-Based Machine Learning comes in. Ortec Finance built SBML to map these tangled relationships, blending data science with economic modelling. It learns how assets and liabilities react when markets bend out of shape.

Exposing volatility and tail risks that truly matter for solvency management

We think that’s the step insurers have been waiting for – not just better forecasts, but models that finally behave like the markets they’re supposed to explain.

So yes, the spreadsheet era is done. Maybe not everywhere yet, but the direction’s obvious.

The firms leaning into stochastic, capital-aware, data-heavy ALM aren’t chasing buzzwords. They’re building survival tools for balance sheets that now move in real time.

We think this shift changes the game. It’s not about predicting the future – nobody can – but about preparing for several at once. The insurers leaning into this approach aren’t chasing precision. They’re building flexibility, ready to pivot fast in a market where certainty feels almost like nostalgia.

FAQ

Because inflation won’t quit, rates swing fast, and capital frameworks like Solvency II and Solvency UK keep shifting. It’s a brutal mix. Asset-Liability Management (ALM) is now the frontline of stability, and insurers relying on spreadsheets are flying blind in an environment that punishes slow adaptation.

They’re deterministic – one path, one forecast, zero realism. These setups ignore non-linear effects, can’t juggle multiple objectives, and crumble when regulatory capital rules move. They give a neat story, but the world isn’t neat. Stochastic and machine-learning-driven tools expose the real volatility.

They weave capital charges from Solvency II directly into the optimisation process. That means insurers can hunt for high-return assets with low capital consumption, improving solvency ratios and freeing funds for dividends or growth. It’s not just risk control – it’s strategic capital management.

It’s the leap from guessing to simulating. Thousands of market scenarios run through these models, showing full distributions of outcomes – not just averages. Management can see how solvency ratios twist under shocks, how liquidity holds up, and where the cliff edge really sits.

SBML, developed by Ortec Finance, uses machine learning to map the messy, non-linear behaviour of today’s markets. It learns from data how assets and liabilities interact when things get weird. The result – ALM models that finally act like the markets they describe, not textbook simplifications.

Instead of leaning on history, insurers build their own “what-if” worlds – trade wars, stagflation, climate hits, political paralysis. Each scenario runs through capital and solvency layers, showing who survives and who sweats. It’s not theory anymore; it’s tactical foresight.

Drop the spreadsheets. The firms moving to stochastic, capital-aware, SBML-powered ALM aren’t overreacting – they’re future-proofing. Markets are fractured, uncertain, alive. Flexibility beats prediction every time, and the ones who adapt fastest will own the next cycle.

…………………….

AUTHORS: Saiyan Raja – Investment Solutions Director, Hamish Bailey – Managing Director UK, Head of Insurance & Investment

Edited by Yana Keller — Lead Insurance Editor of Beinsure Media