California FAIR Plan customers will face the insurer’s largest rate increase in years starting in October. Premiums will rise by just under 30% overall for nearly 663,000 residential policyholders.

The final change will vary by property and location. About half of customers will see rates climb 30% to 50%, while one-quarter will see premiums decrease by as much as 80%.

The remaining quarter will see either smaller increases below 30% or larger hikes between 50% and 200%. Policyholders will see the new premium at their first renewal date after Oct. 15, according to The San Francisco Chroniclean.

Some of the largest increases will hit wildfire-exposed communities. In Grizzly Flats, in the Sierra Nevada foothills, nearly 150 customers will see average annual premiums rise from $2,671 to $5,485.

In the 94563 ZIP code covering Orinda in the East Bay, rates are set to rise by an average of 31%. That would bring the average premium in the community to nearly $7,000.

San Francisco policyholders are mostly expected to see lower rates. The FAIR Plan said the largest part of the increase relates to the wildfire portion of premiums, so higher-risk properties will see larger increases.

The plan’s spokesperson said some lower-risk policyholders will receive premium decreases. Individual rate changes range from an 80% decrease to a 200% increase, based on extrapolated March 2025 data.

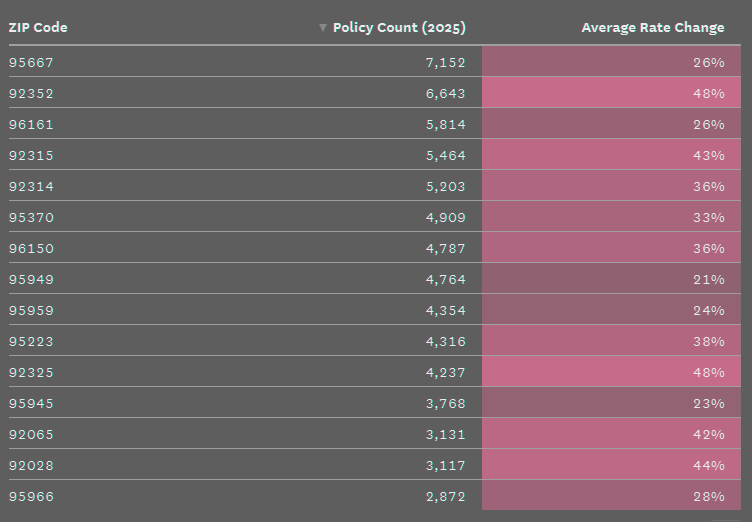

Average rate changes for the California FAIR Plan in late 2026

This is the FAIR Plan’s first statewide rate increase since 2023, when premiums rose 15.7% overall. The plan must submit an updated rate filing at least every two years.

Since the last increase, California’s insurance crisis has pushed FAIR Plan residential policy counts to double. Data show the plan has continued growing over the past year, though at a slower pace.

Insurance Commissioner Ricardo Lara recently told state lawmakers that the slowing growth is a promising sign for California’s insurance market. The FAIR Plan remains a state-created but privately run insurer of last resort.

The plan now insures more homes than nearly every private insurer in California. Its coverage is limited to fire damage, so customers need a second policy for water leaks, liability, and other exposures.

Policyholders are supposed to use the FAIR Plan only when they cannot obtain private-market coverage. In practice, insurer pullbacks in fire-prone areas have pushed many homeowners into the plan.

Rapid growth in wildfire-prone parts of the state has strained the FAIR Plan. After the 2025 Eaton and Palisades wildfires, the plan ran out of money to pay claims.

State law required private insurers to cover the shortfall with a $1 bn assessment. Half of that assessment is currently being passed on to those insurers’ customers.

Even before the Los Angeles County wildfires, FAIR Plan President Victoria Roach warned that the insurer needed a major rate increase. She said the plan had to address growth and prepare for the possibility of a large wildfire.

When the FAIR Plan filed its request last October, it asked regulators for an increase just under 36%. The insurer said it would have requested an 80% increase without recent Department of Insurance reforms known as the Sustainable Insurance Strategy.

Those reforms allow the FAIR Plan and other insurers to price wildfire risk using forward-looking models rather than relying only on historical data. They also allow insurers to charge customers for part of their reinsurance costs.