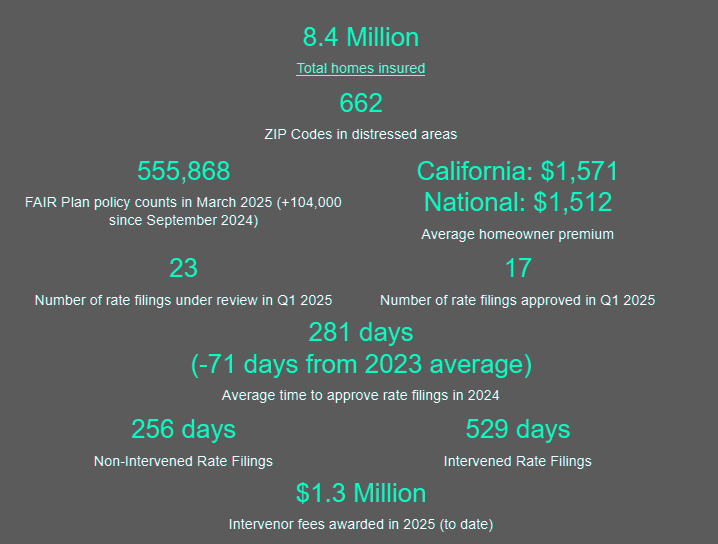

California’s homeowners insurance market keeps shifting under pressure, and the latest snapshot shows how uneven the recovery remains. Roughly 8.4mn homes carry coverage statewide, yet 662 ZIP codes now qualify as distressed, according to California Department of Insurance.

FAIR Plan enrollment hit 555,868 policies in March 2025 – up about 104,000 since September 2024 – a jump that tells its own story about risk, retreat, and limited carrier appetite.

Average annual premiums sit at $1,571, slightly above the $1,512 national figure, though that gap hides the wild variation between coastal suburbs and wildfire belts.

Rate activity picked up in early 2025. Regulators reviewed 23 filings and approved 17. Approval times improved to an average of 281 days in 2024, down 71 days from the year before.

Non-intervened filings cleared in about 256 days; intervened filings dragged to 529 days. Intervenor fees reached $1.3mn in 2025, which, depending on who you ask, either boosts accountability or slows badly needed adjustments.

All of this funnels into the Sustainable Insurance Strategy, Commissioner Ricardo Lara’s attempt to modernise rules that haven’t evolved much since voters passed Proposition 103 more than three decades ago.

Climate change drives up loss volatility, inflation pushes repair costs past what old pricing models can handle, and carrier pullbacks leave whole regions dependent on the FAIR Plan.

Something had to give. Lara took that feedback – gathered during thousands of town halls and meetings – and drafted a set of regulatory updates built to get carriers writing again.

The most disruptive rule forces insurers to offer more policies in wildfire-distressed ZIP codes and shrink the FAIR Plan’s footprint. Before this, no law obligated carriers to write in high-risk regions.

Coverage availability lived or died on business strategy. That freedom helped fuel the availability crisis, especially as global inflation and repeated wildfire seasons hammered balance sheets.

The new mandate changes the calculus by tying future rate flexibility to stronger participation in difficult markets.

Regulatory modernisation sits at the centre of the strategy. The Department pushed transparency reforms for intervenors, updated FAIR Plan governance, issued a bulletin to overhaul rate review, and created space for catastrophe modelling in rate-making – a shift long demanded by carriers who argued that historical loss data can’t price today’s wildfire seasons.

Reinsurance and rate rules reached the Office of Administrative Law by the end of 2024, setting the stage for the next round of filings in 2025.

Climate risk remains the anchor issue. Wildfires, drought and heat waves shape the state’s exposure map far more aggressively than they did a decade ago.

California now tracks distressed exposures more closely: about 1.47mn earned exposures sit inside distressed areas when counting both voluntary carriers and the FAIR Plan.

The statewide figure excluding the FAIR Plan comes in at 8.134mn. These tallies help determine how much coverage carriers must provide under the new rules.

Transparency and accountability appear repeatedly in the strategy. New reporting requirements make it harder for companies to quietly retreat from markets while seeking rate relief.

FAIR Plan modernisation expands available coverage types, strengthens financial stability, and offers better visibility into pool operations.

Governor Newsom’s earlier executive order set the groundwork for these changes, but Lara’s enforcement rounds pushed them into daily practice.

Taken together, the reforms aim to stabilise availability without letting premiums drift unchecked. It’s messy, and even supporters admit the rollout tests everyone’s patience, but California now has a regulatory playbook that matches the scale of its climate-driven insurance problems.

The Sustainable Insurance Strategy keeps evolving, and the market data – FAIR Plan counts, approval times, rate filings – shows just how big the challenge remains.