Small bumper dings used to be cheap, predictable fixes. A cover, some paint, maybe a headlamp, and the bill usually stayed under a few hundred bucks. That era’s gone.

A light tap today can turn into a four-figure repair because the real damage rarely shows. It sits behind the bumper, inside the grille, or up on the windshield where advanced driver-assistance systems live.

ADAS tech changed how cars behave on the road, and now it’s changing how insurers, repair shops and drivers handle even the most trivial collisions.

Cheap Insurance keeps warning customers about this shift because the price jump blindsides people. A repair that costs $200 on the bodywork might add a $500 calibration charge. Sometimes more. And if the recalibration doesn’t happen, the car’s safety systems can go off the rails.

- Advanced Driver Assistance Systems (ADAS) are a suite of electronic technologies that use sensors, cameras, and other automated systems to help drivers with safety and comfort by providing warnings or taking control of vehicle functions like steering and braking.

- These systems reduce accidents by minimizing human error, and common examples include adaptive cruise control, lane-keeping assist, blind-spot monitoring, and automatic emergency braking

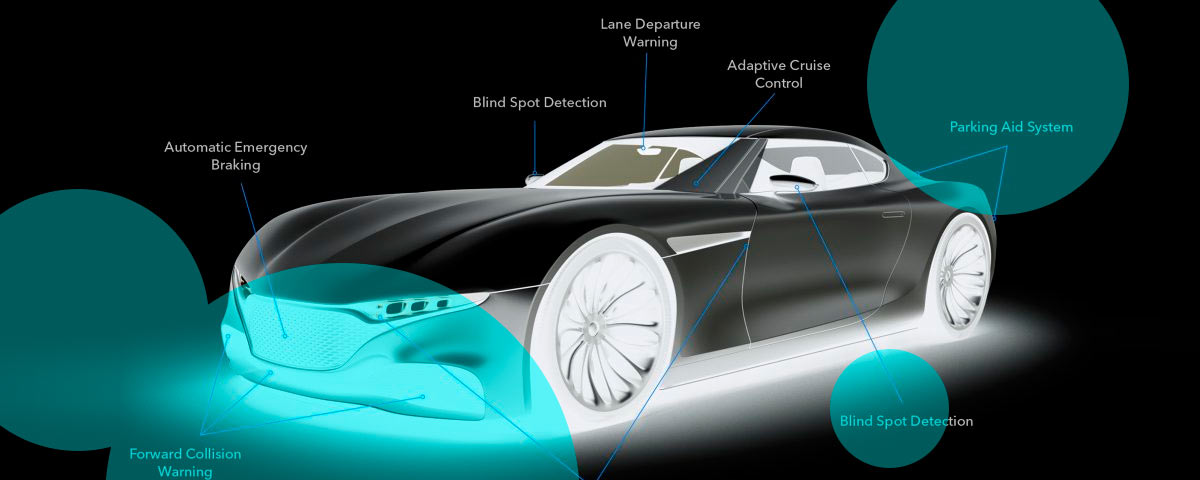

Modern vehicles behave like rolling computers. ADAS uses radar, cameras and ultrasonic sensors to run adaptive cruise control, lane-keep assist, automatic emergency braking and blind-spot monitoring.

These aren’t passive gadgets. Radar modules sit behind bumper covers or grilles. Windshield-mounted cameras run lane markings and pedestrian detection.

Ultrasonic sensors embedded in bumpers watch the low-speed perimeter. Every component plugs into a network that reacts in milliseconds. When a car takes a hit, even a gentle one, the physics get messy.

A millimetre shift in a radar bracket changes the unit’s viewing angle by fractions of a degree. That may sound trivial, but over 100 feet, that tiny error can put the radar’s line of sight several feet off-centre.

Suddenly the car thinks a vehicle in another lane is the one it should follow, or an obstacle that isn’t there deserves an emergency brake slam. That’s why calibration isn’t optional.

Replace a bumper, a windshield, a grille, even some suspension parts, and the system has to be reset. Shops know it. Insurers know it. States are now writing laws to force the disclosure.

Utah set a rule requiring repairers to tell customers when recalibration is needed. Arizona senators pushed for itemised documentation and clear customer notices from auto-glass shops.

Florida banned assignment agreements for post-loss benefits tied to ADAS calibrations, trying to stop inflated claims and keep insurers in control of the process.

California, meanwhile, shows how inconsistent things remain. Comprehensive policies typically cover calibration after a collision, but the burden falls on shops to prove it happened or risk the insurer denying the claim.

All of this funnels into rising premiums. Insurers treat ADAS recalibration as mandatory for safety, not a negotiable add-on.

And as more cars ship with radar, lidar, cameras and ultrasonic sensors packed into fragile spots, the cost of even a minor accident will keep climbing.

According to Beinsure, the insurance industry isn’t fighting that trend anymore – it’s adapting by rewriting policies, tightening claims procedures and leaning heavily on documentation.

The tech promised safer roads, and maybe it delivers that, but the repair economics have changed and there’s no going back to the days when a bumper ding truly was just a bumper ding.