Overview

Fitch Ratings’ assessment of the company profiles of its rated Korean life insurers takes into consideration the insurers’ operating scale, franchise value, business risk profiles and diversification.

High Influence of Company Profile

Hanwha Life and Kyobo Life rank second and third, respectively, by size within the Korean market, with strong franchise value and operating scale. The other rated insurers are mid-sized.

The capital strength of the Korean peer group ranges from ‘Strong’ to ‘Adequate’.

The capital strength of the rated life insurers is partly supported by the capital supplementary bonds in preparation for the upcoming regulatory regime, K-ICS. Consequently, the interest payment burden is gradually increasing, leading to lower debt service capability and financial flexibility credit scores for some insurers.

Earnings Sustainability Remains Key: the peer group’s financial performance is diverse, amid the low but gradually increasing interest rate environment.

Low interest rates have put pressure on the insurers’ ratings because they have a high-influence credit factor. Gradually increasing interest rates will improve investment yields and somewhat ease the burden on reserving.

Capitalisation Commensurate with Ratings

Capitalisation, a key credit factor that drives insurers’ ratings, is measured using Fitch Prism model scores and statutory risk-based capital ratios.

Most of the rated life insurers reported a drop in shareholders’ equity due to losses associated with available-for-sales securities amid interest rate hikes.

Nonetheless, the capital strength of the Korean peer group, measured by the Fitch Prism model, ranges from ‘Strong’ to ‘Adequate’, if a portion of the liability adequacy test surplus is included as available capital.

Higher Debt and Interest Burden

The capital strength of the rated life insurers is partly supported by capital supplementary bonds in preparation for the upcoming regulatory regime, K-ICS.

Consequently, the interest payment burden is gradually increasing, leading to lower debt-service capability and financial flexibility credit scores for some insurers.

Earnings Sustainability Remains Key

Financial performance is an important driver in our ratings assessment of these insurers. Increasing interest rates moderately improved investment yields and somewhat eased the burden on reserving.

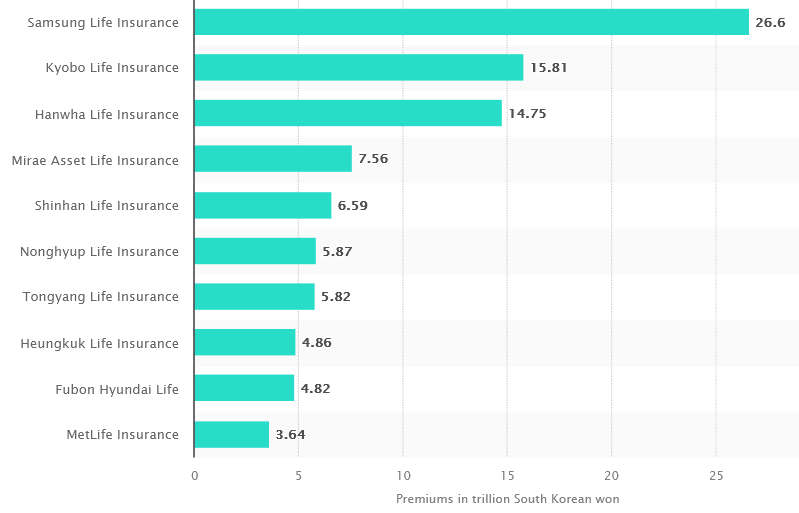

Samsung Life Insurance was the leading insurance company in South Korea with gross written premiums amounting to about 26.6 trillion South Korean won. Kyobo Life Insurance and Hanwha Life Insurance followed with gross written premiums worth around 15.8 and 14.7 trillion South Korean won respectively.

Leading life insurance companies in South Korea, by gross premiums written

What are the largest life insurance companies in Korea?

Samsung Life Insurance is a South Korean multinational insurance company headquartered in Seoul, South Korea, and a subsidiary of the Samsung Group. It is the largest insurance company in South Korea and a Fortune Global 500 company. Samsung Asset Management Co.

by Yana Keller

by Yana Keller