A strategic reinsurance market reset by global reinsurers has led to strong technical profits and altered industry dynamics, according to AM Best’s Market Segment Report, Strong Technical Profits Bolster Momentum for Global Reinsurers.

The report highlights that this reset involved moving away from high-frequency layers, implementing tighter contract wording, and clarifying coverage scope.

These actions have shifted reinsurers’ focus toward providing capital protection to cedents rather than stabilizing earnings.

AM Best predicts that hard pricing conditions in reinsurance will persist longer than in previous cycles. This is mainly due to high claims activity driven by a buildup of medium-sized losses and secondary perils, rather than single major catastrophes.

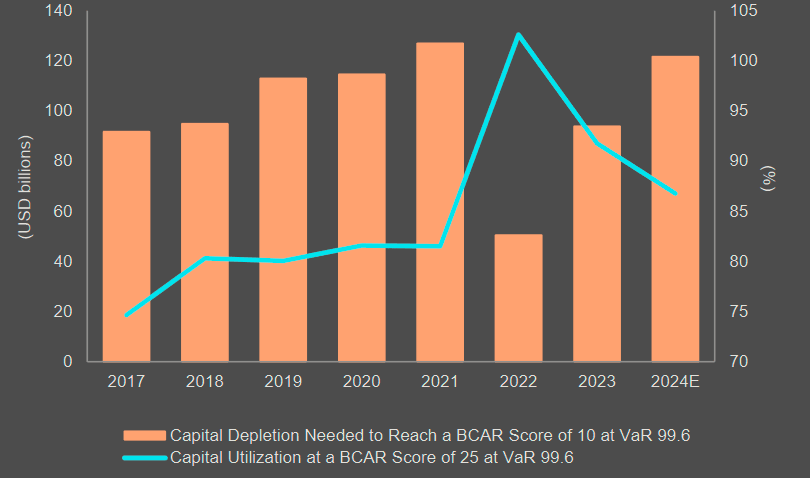

Global Reinsurance – Capital Utilization

The global reinsurance sector remains well-capitalized, with companies maintaining strong solvency positions. The sector has not faced significant pressure, except for unrealized losses on fixed-income investments, which have since reversed.

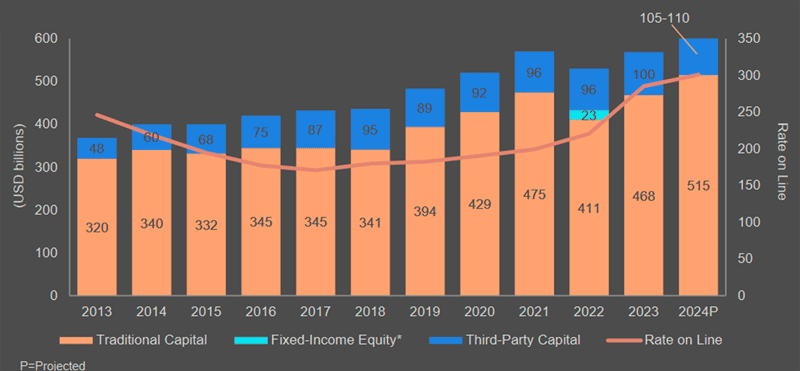

Global Reinsurance – Estimated Dedicated Reinsurance Capital

This hard cycle has not seen capital depletion. Despite attractive pricing, new company formations, particularly in property catastrophe, have been absent. According to Carlos Wong-Fupuy, senior director at AM Best, disappointing results during the previous prolonged soft market discouraged potential new investors.

Aon estimates that global reinsurer capital rose by $25 bn to a new high of $695 bn over the three months to March 31, 2024. The increase was principally driven by retained earnings, recovering asset values and new inflows to the catastrophe bond market, according to Aon’s Report about the Reinsurance Market Dynamics.

Underlying ROEs were materially higher due to a further reduction in underlying combined ratios and higher recurring investment income.

Whether viewed on a headline or underlying basis, reinsurers’ ROEs now comfortably exceed the industry’s cost of capital.

The current hard cycle has not been characterized by capital depletion. Unlike previous hard cycles and despite the very attractive pricing environment, new company formations have not materialized, particularly in the property catastrophe space

Carlos Wong-Fupuy, senior director, AM Best

“Disappointing results during the previous, prolonged soft market deterred potential new investors”, Carlos Wong-Fupuy commented.

AM Best noted a clear shift confirming the current hard market conditions following the market disruption during the January 2023 renewals.

Although reinsurers are now challenged by the adoption of IFRS 17 accounting standards, the segment continues to grow, producing returns on equity well above their cost of capital. Meanwhile, strong combined ratios reflect substantial profit margins, offsetting concerns about adverse reserve development in legacy U.S. casualty books.

by Yana Keller

by Yana Keller