Overview

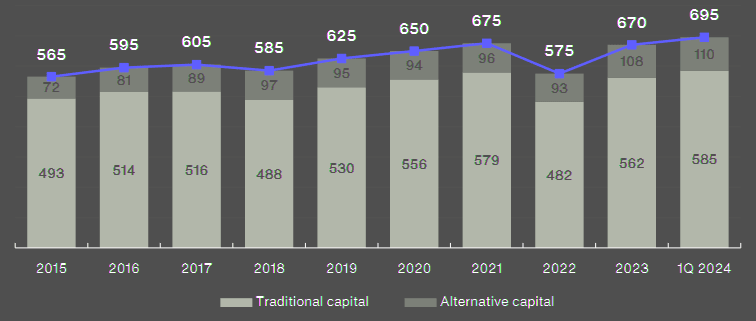

Aon estimates that global reinsurer capital rose by $25 bn to a new high of $695 bn over the three months to March 31, 2024. The increase was principally driven by retained earnings, recovering asset values and new inflows to the catastrophe bond market, according to Aon’s Report about the Reinsurance Market Dynamics.

The better natural catastrophe experience of the reinsurers stands in sharp contrast to overall insured natural catastrophe losses.

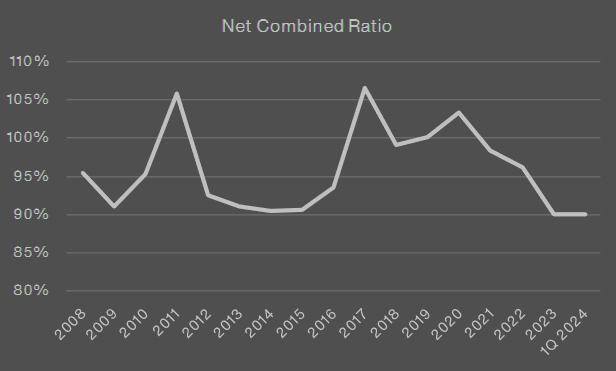

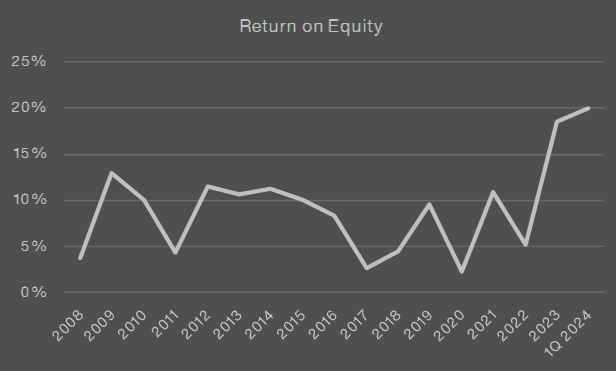

Underlying ROEs were materially higher due to a further reduction in underlying combined ratios and higher recurring investment income.

Whether viewed on a headline or underlying basis, reinsurers’ ROEs now comfortably exceed the industry’s cost of capital.

Traditional capital: equity at record levels and building

Aon estimates that shareholders’ equity reported by global reinsurers increased by $23 billion to a new high of $585 billion over the three months to March 31, 2024.

The main drivers were robust underwriting results and improved total investment yields, which combined to deliver very strong returns on equity.

Global Reinsurer Capital

Attritional claims activity remained stable in the first quarter, with natural catastrophe losses below budget despite some deterioration in 2023 events.

The Baltimore bridge collapse was a manageable loss, but uncertainties around the amount were noted. Evidence suggests increased resilience in long-tail reserving positions.

Reinsurance Sector Performance

Reinsurer results

All companies tracked showed top line growth in property and casualty insurance and reinsurance in the first quarter of 2024. RenRe led the way, following the acquisition of Validus.

Pricing was generally viewed as remaining ahead of loss cost trends, albeit with rate reductions in cyber, directors’ and officers’ liability and workers’ compensation.

Strong margins and good growth opportunities continued in the excess and surplus lines market, particularly on the casualty side. Most companies increased their focus on growing short-tail lines.

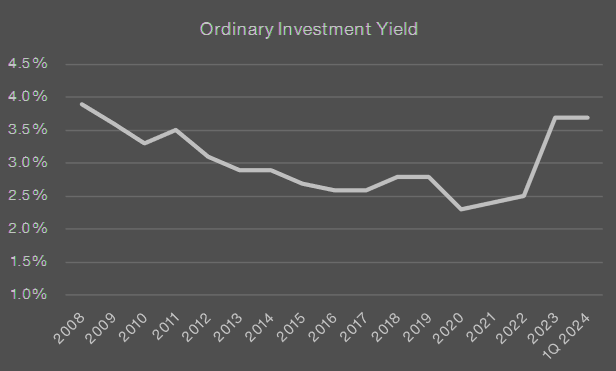

Investment returns are increasingly contributing to overall earnings. Strong operating cash flows are boosting assets under management, and higher interest rates are now having an impact.

Ordinary yields increased by around 1% compared to a year earlier. Recovering bond values and strong stock markets are supporting total returns.

Interest rates are expected to stay high for an extended period, with ordinary yields likely to rise further based on current reinvestment rates.

Overall, business growth, moderate major losses, and favorable capital markets combined to generate strong returns on equity.

Retained earnings are boosting recovery in equity positions from the 2022 lows. Most companies are now stronger than at the end of 2021. On average, the companies tracked saw a 4% growth in total equity in Q1 2024.

New start-ups are still scarce, despite attractive returns, indicating ongoing investor concerns about the challenging risk environment.

Reinsurer capital is building quickly

Given growth and diversification in recent years, most management teams have a range of options on the underwriting side, including in direct insurance and life business.

Risk appetite for property catastrophe business has generally been stable-to-up in 2024, but the focus has mainly been on higher attaching layers, given continuing loss activity from secondary perils.

Some companies with less exposure to soft market years also see an opportunity to grow in casualty reinsurance, despite continuing concerns around the impact of social inflation.

There are competing alternatives for newly generated capital, notably increasing rewards to investors and franchise-building, via mergers and acquisitions. Activity can be observed in both areas.

Nevertheless, in the absence of very large primary peril losses (noting forecasts of a very active Atlantic hurricane season), we would expect an easing of underwriting conditions at the 2025 renewals.

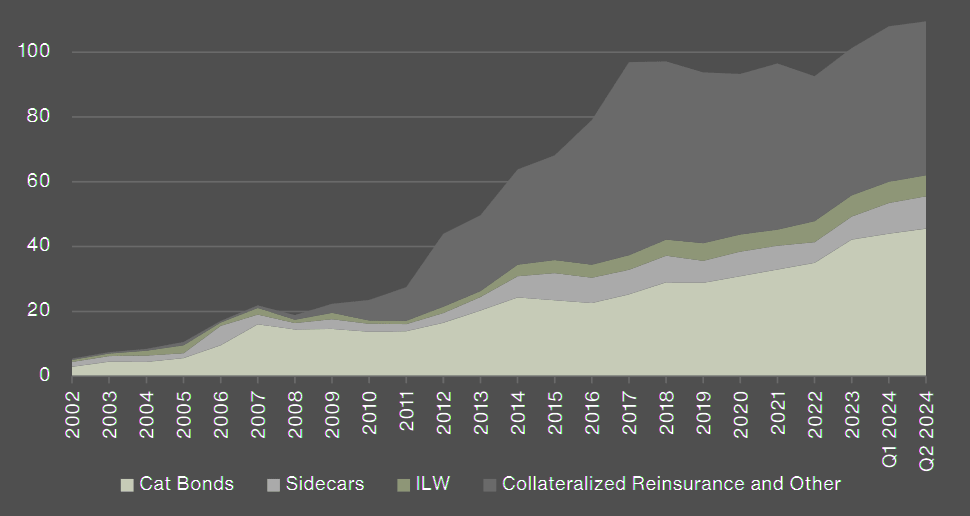

Alternative capital: issuance volume continues to break records

The second quarter of 2024 followed the ongoing theme of major growth for the overall ILS market. Aon Securities estimates that overall ILS capital grew to an all-time high of $110 bn.

Throughout the quarter, ILS investors remained focused on allocating capital ahead of the North Atlantic hurricane season.

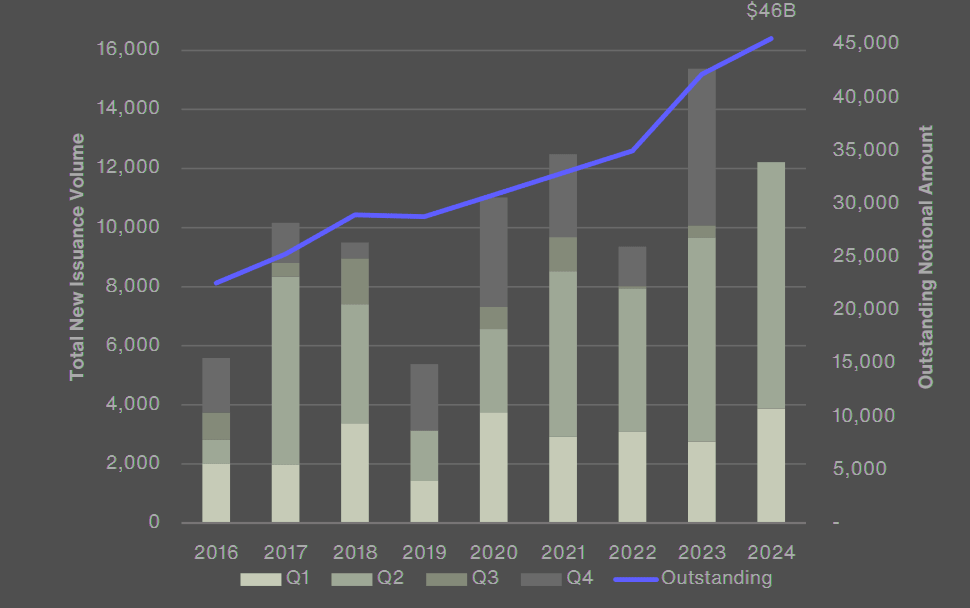

Catastrophe bonds reached a record high, with over $8 bn issued in a single quarter, increasing the total volume from $41 bn to $46 bn.

The sidecar market is also expanding as investors seek returns from the strong margins in proportional structures. Aon estimates ILS capital grew by about 2% this quarter, adding to the significant growth over the past 15 months.

Alternative Capital Deployment

The last three quarters have set records for catastrophe bond issuance. Q2 2024 saw the highest volume, rising by $1.42 bn to $8.34 bn from $6.92 bn in Q2 2023.

Growth came from both supply and demand factors. Insurers issued new bonds before hurricane season, with 27 new issuances from 24 sponsors, including six newcomers. This demand indicates a need for capacity beyond traditional reinsurance.

The market also benefited from three Japanese insurer transactions, though U.S. hurricane bonds dominated. Insurance companies issued $5.78 bn in the first half of 2024.

Reinsurers issuing index-based catastrophe bonds

Reinsurers were also intent on issuing industry index-based catastrophe bonds the first half of this year. During the first quarter of 2024, the capital supply for these products exceeded demand with secondary spreads tightening by upwards of 14%.

Reinsurers in the second quarter sought to extract similar pricing from investors, however the favorable price environment for index buyers was short-lived.

The market quickly reversed course with some very significant spread widening throughout the quarter, and by mid-May the market was back to levels seen in Q4 2023.

Primary insurers also paid increasingly higher spreads as the pricing dynamic which first impacted industry loss transactions spread more generally across the market. Reinsurers hoped for investors to continue growing this part of the market, however investors lacked the capacity to meet demand, resulting in significant spread widening.

The $10.64 bn record issuance since the beginning of 2024 is impressive, though reinsurers would have printed even greater volumes if investors had more capital to deploy for industry-based index catastrophe bonds.

Property Catastrophe Bonds Issued

Investors collaborated with government institutions on several major transactions. Following FEMA’s $575 mn and the North Carolina Insurance Underwriting Association’s (NCIUA) $450 mn deals in Q1, the Texas Windstorm Insurance Association (TWIA) secured $1.4 bn with an indemnity annual aggregate transaction, the second-largest catastrophe bond transaction ever.

Mexico and Jamaica, through the World Bank, issued parametric transactions totaling $745 mn to replace recently matured capacity.

Louisiana Citizens and the North Carolina Joint Underwriting Association (NCJUA) issued indemnity-triggered transactions for U.S. named storms, securing $275 mn and $145 mn, respectively. Florida Citizens issued $1.1 bn ahead of the North Atlantic hurricane season.

The Commonwealth of Puerto Rico benefited from its first catastrophe bond, an $85 mn parametric-triggered bond, protecting against significant named storms and earthquakes.

The sidecar market also grew, attracting significant investor interest. Several key transactions closed in Q2, bringing over $1 bn of capital into the market in the past year.

Opportunistic investors have allocated across a range of strategies as historic reinsurance rate hardening has generated multiple opportunities and encouraged creative structuring.

Expected returns are highest in property catastrophe portfolios, and investors have gravitated towards partnerships based on alignment, track record and collateral efficiency.

Casualty investors consider these factors important as well but are more focused on investment guideline flexibility, leverage and transaction duration as they establish bilateral arrangements where investors can manage the underlying collateral.

Specialty portfolios have also captured the attention of investors as (re)insurers seek growth capital and investors value the diversification benefits combined with reduced volatility (compared with cat-driven investments) offered via specialty portfolios.

With the catastrophe bond market wrapping up its busiest quarter ever, and the sidecar market resurgent, all eyes turn towards the North Atlantic hurricane season. While many have forecasted this season to be active, it’s been promising to see strong investor fundamentals drive continued growth of the ILS market.

……………….

AUTHORS: Mike Van Slooten – Head of Business Intelligence at Aon, Richard Pennay – CEO of Insurance-Linked Securities at Aon