Overview

- Reinsurers are Moving Toward Diversification

- Traditional Reinsurance Capital Increased YoY

- Traditional Reinsurance Capital Grows Despite Market Shifts

- Big Four European Reinsurers – Capital & Profitability

- Third-Party Reinsurance Capital Growth

- 2025: A Softer but Still Profitable Market

- Risk-Adjusted Capitalization Strengthens as Utilization Drops

- Required Reinsurance Capital Growth by Risk Factor

The global reinsurance sector has undergone a notable transformation since the market reset in 2023, drawing sustained attention from investors and analysts. Rather than a surge of new start-up reinsurers, capital has returned through more deliberate channels, according to AM Best’s Market Segment Report, “Momentum Remains for Dedicated Reinsurance Capital Beyond the Market Peak,” is part of AM Best’s look at the global reinsurance industry.

Established players have reinforced balance sheets with secondary equity offerings, disciplined earnings retention, and increased use of catastrophe bonds, which continue to attract strong investor demand.

These measures have improved market resilience and expanded capacity, even through challenging events such as Hurricane Helene in September 2024, Hurricane Milton in October, and the California wildfires in early 2025. Beinsure has analyzed market data and highlighted the key points.

Key Highlights

- Dedicated reinsurance capital rose 7% in 2024, reaching $500bn, supported by strong underwriting results, higher investment yields, and retained earnings despite heavy catastrophe losses.

- Investor appetite for insurance-linked securities drove third-party reinsurance capital up 7% to $107bn in 2024, with projections for $114bn in 2025 fueled by record cat bond issuance.

- Reinsurers are reallocating capital to primary and specialty lines, moving away from reliance on property-catastrophe risks. This trend stabilizes earnings but reduces the share of capital tied to traditional reinsurance.

- Capital utilization improved to 85% in 2024, down from 92% in 2023 and well below the 103% seen in 2022. This reflects stronger capitalization and resilience against extreme stress scenarios.

- Interest rate risk declined 17.9% as reinsurers benefited from higher-yielding investments, while catastrophe risk increased 22.9% due to higher cedent demand and exposure to secondary perils such as convective storms and wildfires.

The interest rate swings that hurt reinsurers’ fixed income portfolios in 2022 have largely reversed. By 2023, most mark-to-market losses were either recovered or strategically reinvested. Higher yields in 2024 boosted reinvestment income, providing reinsurers with stronger retained earnings and more financial flexibility, Beinsure noted.

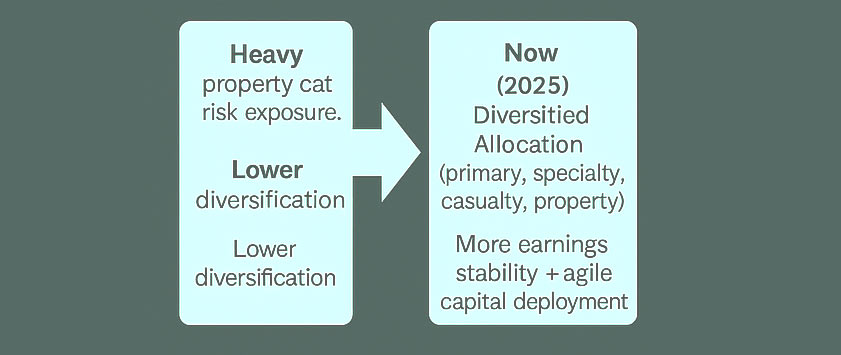

Reinsurers are Moving Toward Diversification

Strategically, global reinsurers are moving toward more diversified and balanced business models. Capital is increasingly allocated to primary and specialty lines rather than heavily concentrated in property catastrophe risk.

This evolution provides earnings stability and allows more agile capital deployment across cycles, though it reduces capital dedicated to traditional reinsurance.

Casualty lines remain pressured by adverse reserve development tied to social inflation and shrinking margins, but strong property results and improved investment income offset those strains.

Reinsurers continue to transition toward more diversified and balanced business models, including a growing allocation to primary and specialty insurance lines, reflecting a deliberate move away from purely relying on property catastrophe risk.

Antonietta Iachetta, associate director, AM Best

“This structural shift supports earnings stability and more agile capital deployment, as well as the amount of capital deployed in the traditional reinsurance market, even with significant catastrophic activity,” said Antonietta Iachetta.

Reinsurance Strategic Shift (2018–2025)

Then (2018) → Heavy property-cat risk exposure → Lower diversification.

Now (2025) → Diversified allocation (primary, specialty, casualty, property) → More earnings stability + agile capital deployment.

Softer pricing at reinsurers’ June and July reinsurance renewals supports view that abundant capacity and rising competition will continue to pressure prices. Declining reinsurance prices, increased claims severity from natural catastrophe events, and slightly looser terms and conditions (T&Cs) in property lines are expected to reduce underwriting margins in 2025, Beinsure noted.

Both traditional and third-party capital-backed reinsurance performed strongly in 2024 and through the first half of 2025.

The ability to absorb losses from multiple large catastrophes while maintaining growth in capital underscores the sector’s improved resilience and broader investor confidence (see Reinsurance Rates in Europe).

The cat bond market has attracted increased interest from investors seeking exposure to short duration and high yield instruments that remain relatively insulated from broader market volatility.

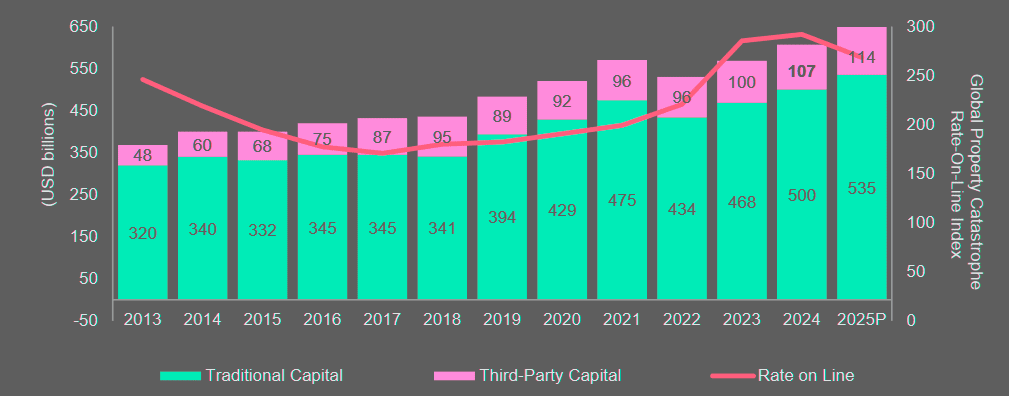

Traditional Reinsurance Capital Increased YoY

According to this report, traditional reinsurance capital increased year over year by approximately $32 bn, or 7%, to $500 bn in 2024, supported by strong underwriting results, retained earnings and higher investment yields.

Reinsurance buyers generally experienced a more competitive reinsurance market at the July 1 renewal compared to recent years, with capacity available even where demand increased

While a wave of new startup reinsurers entering the market has not emerged, established reinsurers have strengthened their capital bases via secondary equity offerings, as well as through disciplined retention of earnings while a surge in investor appetite for catastrophe bonds has bolstered third party capital growth.

Together, these sources of capital have enhanced the market’s overall financial resilience and its capacity for growth, Beinsure noted.

Global Reinsurance Capital Growth (2023–2025E)

| Year | Traditional Capital ($bn) | Third-Party Capital ($bn) | Total Dedicated Capital ($bn) |

| 2023 | 468 | 100 | 568 |

| 2024 | 500 | 107 | 607 |

| 2025 | 535 | 114 | 649 |

Third-Party Reinsurance Capital

Third-party reinsurance capital saw a 7% increase in 2024 to $107 bn, according to the report. AM Best works in conjunction with Guy Carpenter to estimate the total amount of capital supporting the reinsurance industry, according to Global Reinsurers Report.

The third-party reinsurance capital estimate for 2025 is estimated at $114 bn, driven predominantly by record-setting growth in catastrophe bond issuance.

Assuming a more normal level of catastrophic events, reinsurers are on pace to report upper-single-digit capital growth in 2025.

Dan Hofmeister, associate director, AM Best

“Volatility in asset risk and potentially higher reserve charges from continued social inflation could create some negative pressure, but reinsurers are well-positioned to absorb a normal level of volatility in the market,” said Dan Hofmeister.

Implementation of IFRS 17 is Shaping Strategic Conversations

While the standard has introduced material changes in how insurance liabilities and revenues are reported, the accounting methodology has not changed or influenced the assessments of risk-adjusted capitalization or balance sheet strength, and, therefore, credit ratings also remain unaffected, Beinsure noted.

No material change in traditional reinsurance capital has been realized, or is expected, as a direct result of IFRS 17.

The reinsurance market enters the latter half of the decade on a stronger footing, supported by more resilient capital structures, an increasingly diversified business mix, and growing investor interest in non-traditional risk instruments.

As macroeconomic volatility persists and regulatory frameworks evolve, the ability to adapt both operationally and strategically should lead to continued growth in capital levels.

Traditional Reinsurance Capital Grows Despite Market Shifts

AM Best’s latest analysis shows traditional reinsurance capital continuing to build momentum, even as reinsurers diversify into primary and specialty lines.

Dedicated reinsurance capital reached $500bn at year-end 2024, up from $468bn the prior year.

Since 2018, traditional reinsurance capital has represented less than 60% of consolidated shareholders’ equity for groups identifying as reinsurers.

That share slipped further to around 50% in 2024, underscoring the structural pivot toward broader insurance portfolios beyond property-catastrophe risk.

Global Reinsurance – Estimated Dedicated Reinsurance Capital

The increase in absolute capital came despite significant catastrophe losses.

The largest European reinsurance groups were the main drivers, delivering an average return on equity of 16.2% in 2024, down modestly from 17.4% in 2023 but still well above both their five-year average and the cost of capital.

Collectively, they generated $11.6bn in net income, providing a strong foundation for capital growth.

European reinsurers recorded stronger return on equity (ROE) in 2023 and 2025, exceeding their cost of equity in three of the last four years, according to Goldman Sachs. Beinsure analyzed the report and highlighted the key points.

Between 2017 and 2022, the sector only met or exceeded this benchmark in two years. ROE lagged materially behind in 2017, 2018, 2020, and 2022.

Key pressures included large losses from hurricanes such as Irma, Harvey, and Maria in 2017, and Ian in 2022. But systemic issues also played a role.

Big Four European Reinsurers – Capital & Profitability

| Year | ROE | Net Income ($bn) | Share of Global Re Cap |

| 2023 | 17.4% | 12.3 | 20% |

| 2024 | 16.2% | 11.6 | 21% |

Despite modest ROE decline, strong net income supported capital growth.

The Big Four Europeans’ share of global reinsurance capital stood at 21% at the end of 2024, up from 20% the previous year.

While some reinsurers in this group maintain sizable primary insurance operations and pursue more aggressive dividend and buyback programs than their Bermuda-based counterparts, their ability to sustain strong profitability continues to underpin traditional reinsurance capital expansion.

Softer pricing at reinsurers’ June and July reinsurance renewals supports view that abundant capacity and rising competition will continue to pressure prices.

Declining reinsurance prices, increased claims severity from natural catastrophe events, and slightly looser terms and conditions (T&Cs) in property lines are expected to reduce underwriting margins in 2025.

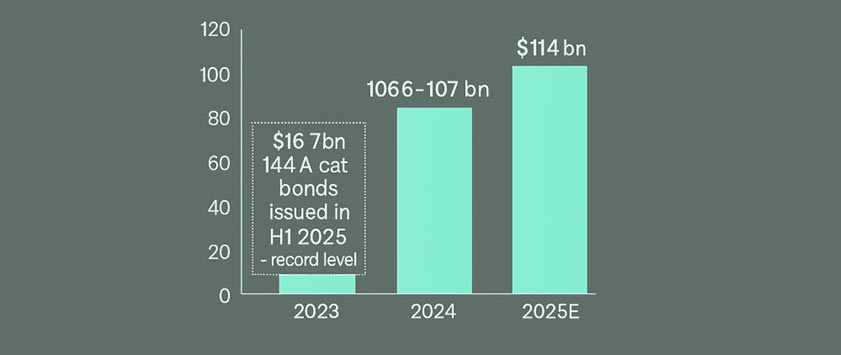

Third-Party Reinsurance Capital Growth

Guy Carpenter and AM Best estimated ILS capacity to have increased modestly through 2024, supported by the recycling of capital from maturing transactions, the reinvestment of a portion of strong 2023 earnings, and the addition of a modest amount of new capital to the market.

In a year where capacity exceeded demand, ILS capital had another recordbreaking year, with $106 bn in 2024, an increase of 6% over 2023.

Guy Carpenter has estimated a slight increase of 7% in net third-party capital in 2025, to $114 bn. Entering 2025, the ILS market has experienced continued growth, with 144A cat bond issuances reaching record-breaking levels at $16.7 bn through June 30, 2025.

Cat Bond & ILS Market Growth

This growth is attributable to investors entering the market during the first half of the year when there is more abundant capacity. A combination of new sponsors and larger deal amounts coming to market has been fostering this growth and demand for capacity.

2025: A Softer but Still Profitable Market

After the recalibration of the January 2023 renewals, the reinsurance market consistently produced

robust operating returns, following years of subpar underwriting and not covering the cost of capital.

Industry capital also grew rapidly, supported by stronger retained earnings and reduced mark-to-

market investment losses. Notably, the absence of new start-up reinsurers enabled incumbents to

preserve market share without resorting to softer terms.

As of mid-year 2025, the property reinsurance market remains stable with signs of modest softening emerging at the highest layers of attachment.

Reinsurers have remained diligent on attachment points and terms throughout the rate softening,

which is believed to be the main factor driving their continued success.

Reinsurance Capital Growth

Capital growth could always be dampened by dividends, as well as a highly active hurricane season.

Despite the uncertainty regarding the remainder of the 2025 hurricane season, the reinsurance market remains well positioned to absorb a reasonable level of losses and still grow capital.

As we approach the height of the US hurricane season, which always brings the potential for outsized losses, the results may affect not just the reinsurance market, but also the insurance market as a whole.

Severe Convective Storms and NatCat Events

Severe convective storms and large cat events have stressed both cedents and reinsurers over

the last year. The market, however, has been resilient despite the impact of the California wildfires

eroding cat budgets and creating uncertainties about the loss costs.

The resilience of reinsurers can be mainly attributed to the accumulation of retained earnings and strong investment yields, which have established solid capital buffers.

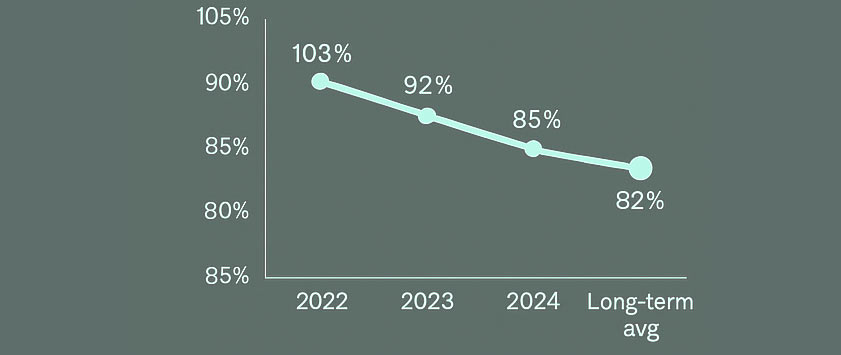

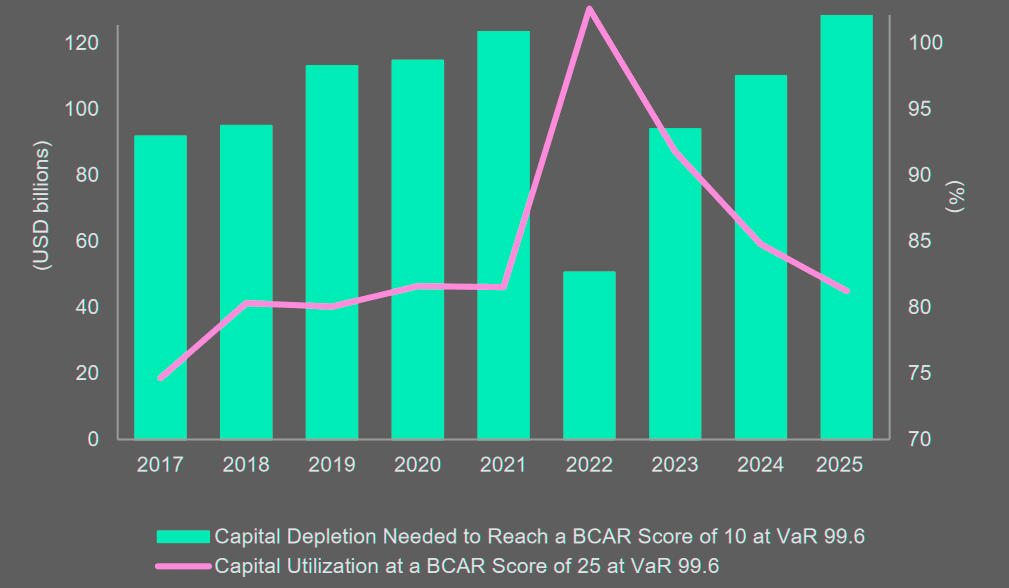

Risk-Adjusted Capitalization Strengthens as Utilization Drops

Assessing reinsurance capital in absolute terms provides only part of the picture. AM Best’s analysis of risk-adjusted capitalization, based on capital utilization, highlights how effectively reinsurers’ balance sheets are positioned against extreme stress scenarios.

Capital utilization compares required risk-adjusted capital with available capital, measuring how much is needed to sustain the strongest BCAR score of 25% at a 99.6% Value at Risk (VaR) level.

The firm also evaluates how much capital erosion would push BCAR down to 10% at the same confidence level, a proxy for stress tolerance.

Capital Utilization Trend (Risk-Adjusted, BCAR at 99.6% VaR)

| Year | Capital Utilization | Interpretation |

| 2022 | 103% | Below “Strongest” BCAR – risk-adjusted cap insufficient |

| 2023 | 92% | Near historic average, improving conditions |

| 2024 | 85% | Stronger capitalization, return to healthier range |

| Long-term Avg | 82% | Stable capitalization trend |

At year-end 2024, traditional reinsurers’ capital utilization improved to 85%, down from 92% in 2023 and well below the 103% seen in 2022.

Utilization above 100% signals capitalization below the “Strongest” BCAR level, making the 2024 result a return to healthier conditions.

Excluding the 2022 spike, which was caused by a 10.7% increase in required capital tied to rising interest rate risk and a simultaneous drop in available capital, the long-term average has been about 82%.

Risk-Adjusted Capital Utilization Path

The 2024 improvement was driven primarily by higher market capital combined with reduced required capital. AM Best expects this more stable utilization trend to continue into 2025.

Required Reinsurance Capital Growth by Risk Factor

Risk-adjusted capital requirements under BCAR at the 99.6% VaR level span eight categories: fixed-income securities, equity securities, interest rate, credit, net loss and loss adjustment expense reserves, net premiums, business risk, and catastrophic risk, adjusted for covariance effects that account for interdependencies.

In 2024, the most significant decline came from interest rate risk, which fell 17.9% as reinsurers shifted toward longer-duration, higher-yielding fixed income portfolios.

Offsetting this was a 22.9% rise in catastrophic risk, reflecting cedents’ demand for higher limits and the growing influence of secondary perils.

Risk Factor Changes in Required Capital

| Risk Factor | Change in 2024 | Commentary |

| Interest Rate Risk | -17.9% | Reinsurers moved to longer-duration, higher-yielding bonds |

| Catastrophe Risk | +22.9% | Rising cedent demand & higher limits, secondary perils |

| Other Risk Factors (credit, equity, reserves, business risk) | Stable | Offset by diversification and improved yields |

The balance between declining financial market risk and rising catastrophe exposure underscores how reinsurers’ capital strength continues to rest on both disciplined portfolio management and their ability to absorb increasing natural catastrophe volatility.

AM Best expects industry conditions to remain steady through the remainder of 2025. Assuming a more normal level of catastrophic events, reinsurers are on pace to report upper-single-digit capital growth in 2025.

This could be offset by volatility in asset risk from a growing investment base and potentially higher reserve charges from continued social inflation and adverse development in the US casualty insurance segment.

Nevertheless, reinsurers are well positioned to absorb a normal level of volatility in the market, as well as handle their relationship with their cedents by providing flexible solutions.

FAQ

Traditional reinsurance capital rose by $32bn, or 7%, reaching $500bn at year-end 2024. Growth was supported by retained earnings, stronger underwriting results, and higher investment yields despite significant catastrophe activity.

Investor appetite for catastrophe bonds surged, pushing third-party reinsurance capital up 7% to $107bn in 2024. AM Best and Guy Carpenter project further growth to $114bn in 2025, supported by record cat bond issuance of $16.7bn in the first half of 2025.

Reinsurers are diversifying beyond property-catastrophe into primary and specialty lines. This shift provides more earnings stability and flexibility in deploying capital, though it reduces the share of capital tied strictly to traditional reinsurance.

After sharp declines in 2022, fixed income portfolios largely recovered by 2023. Higher yields in 2024 boosted reinvestment income, strengthening retained earnings and improving financial resilience.

Capital utilization improved to 85% at year-end 2024, down from 92% in 2023 and well below the 103% recorded in 2022. This indicates reinsurers are holding stronger risk-adjusted capital buffers, with conditions expected to remain stable into 2025.

Interest rate risk declined 17.9% as reinsurers moved into longer-duration, higher-yielding bonds. In contrast, catastrophe risk rose 22.9% amid higher cedent demand and exposure to secondary perils such as convective storms and wildfires.

Assuming a normal catastrophe year, reinsurers are on track for upper-single-digit capital growth. However, volatility from asset risk, reserve charges linked to social inflation, and US casualty developments could weigh on results. Even so, AM Best expects reinsurers to remain well-positioned to absorb normal market volatility while maintaining capacity for cedents.

………………….

QUOTTES: Antonietta Iachetta – Associate Director (Global Reinsurance) at AM Best, Dan Hofmeister, CFA, FRM, CAIA, CPCU – Associate Director at AM Best

Edited by Yana Keller — Re/Insurance Editor at Beinsure Media