Overview

Asia’s insurance-linked securities market sits in an early phase, even though regulators try to push it forward. The market has seen stellar returns, and those retained earnings are being redeployed into new transactions, according to S&P. There’s also fresh capital coming in, both from existing investors and new entrants, particularly in the cat bond space.

Key highlights

- Asia’s ILS market delivers strong returns and rising capital, yet investors still treat the region as an experiment rather than a core allocation.

- MAS rolls out a tiered 2026-2028 grant scheme that sharply reduces issuance costs and nudges first-time sponsors, especially those bringing Asia-Pacific risk.

- Capacity remains concentrated outside Asia, with North American and European investors shaping pricing while Asia builds familiarity.

- Cyber remains too small to securitise in the region, so nat cat dominates as the practical use case while sidecars quietly regain some momentum.

The ILS market experienced two years of strong returns, leading to reinvestment and an increase in available capital. Additionally, new capital inflows, particularly in the catastrophe bond segment, have contributed to record-breaking capacity. Beinsure has selected the main points of S&P research.

While this trend has been promising, market participants are monitoring how catastrophic events, such as the recent wildfires in California, might shape future developments.

H1 2025 has reinforced ILS as one of the most resilient corners of the capital markets. Even against macroeconomic turbulence and shifting risk landscapes, catastrophe bonds continue to show what investors crave: strong yields, minimal volatility, and almost no correlation to mainstream assets, according to Swiss Re’s ILS Report.

New ILS sponsors

According to Swiss Re ILS Market Insights, most encouraging was the number of new sponsors and ESG developments in the asset class.

Catastrophe bonds have been the most consistent and rapidly growing segment within the ILS market. Tuite attributes this to their appeal among both cedants and investors. Insurers and reinsurers use cat bonds to diversify their reinsurance sources, complementing traditional markets, Beinsure noted.

Over the past few years, a steady flow of new sponsors has entered the market, alongside those returning after extended breaks.

The demand side remains strong, with primary insurers, reinsurers, and even government-affiliated entities like Florida Citizens participating. On the supply side, investors appreciate the low correlations, and recent returns have been highly attractive.

Record issuance was supported by overwhelming growth of the cat bond market. With nearly $11 bn of maturities over the same twelve months, the market required over $6.9 bn of growth to sustain the issuance volume over this period.

Asia’s fresh ILS grant scheme

Monetary Authority of Singapore plans a fresh ILS grant scheme that runs from 2026, and the structure tries to cut issuance friction rather than dress up the asset class.

MAS outlines a sharper, more layered ILS grant structure that runs from Jan 2026 through Dec 2028, and the numbers matter because sponsors watch every basis point of issuance cost.

The scheme starts with a broad promise: ILS deals tied to natural catastrophe, longevity, mortality, operational or cyber risks all qualify. That wide net signals MAS wants traffic, not token listings.

Before the new window opens, the baseline remains simple. The grant covers 50% of upfront cat bond issuance costs, capped at S$1 mn. Sidecars and collateralised reinsurance structures receive 70%, capped at S$ 500k. Straightforward, if a little dated.

The 2026-2028 terms push the incentives further. Property cat bonds that include any slice of Asia-Pacific risk qualify for 70% funding with a S$1 mn ceiling.

Issuances without Asia-Pacific exposure drop back to 50%, also capped at S$1mn. Sponsors writing non-property cat bonds get the 70% rate with the same S$1 mn limit.

It’s a clear nod to issuers who want to explore beyond pure nat cat while still anchoring deals in the region’s regulatory hub.

Collateralised reinsurance and sidecars keep their 70% rate, capped at S$500 k. That consistency might feel mundane, but sponsors like predictability when they juggle brokers, modelling firms and fronting carriers.

Renewals land at 30% with a S$500 k cap. Some issuers grumble that renewals deserve more support because repeat transactions build market depth. Maybe. MAS seems to prefer nudging first-timers through the door, then letting experienced sponsors carry more of their own freight.

It’s a tight, tiered system that tries to reduce friction without rewriting the economics of risk transfer. The scheme won’t magically expand the region’s ILS investor base, though it trims enough cost to make the next wave of issuers pause, run the maths, and say yeah, this might work.

New property catastrophe bonds

New property cat bonds tied to Asia-Pacific risks can receive grants covering 70% of upfront costs, capped at S$1 mn. Deals without Asia-Pacific exposure get 50%, also capped at S$1 mn. Renewals land at 30% with a S$500 k ceiling.

It’s a tidy package, and it applies to a wide mix of risk types – natural catastrophe, longevity, mortality, operational, cyber – which tells you MAS wants breadth, not just another tropical cyclone trade.

- SGX already lists a modest cluster of ILS deals.

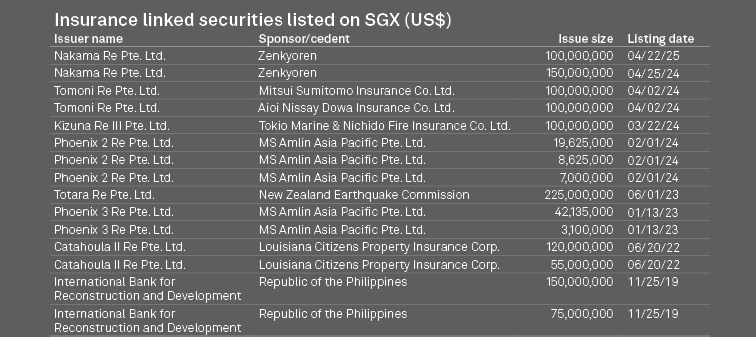

- Japanese nonlife carriers – Mitsui Sumitomo Insurance, Aioi Nissay Dowa Insurance, Tokio Marine & Nichido Fire – each issued $100 mn cat bonds in 2024.

- Zenkyoren pushed Nakama Re deals of $150 mn in 2024 and $100 mn earlier this year.

Insurance linked securities listed on SGX

Issuers like Louisiana Citizens, the New Zealand Earthquake Commission and IBRD also placed >$100 mn transactions on the board. The flow isn’t tiny, but investors still treat the region as something they’ll get to later.

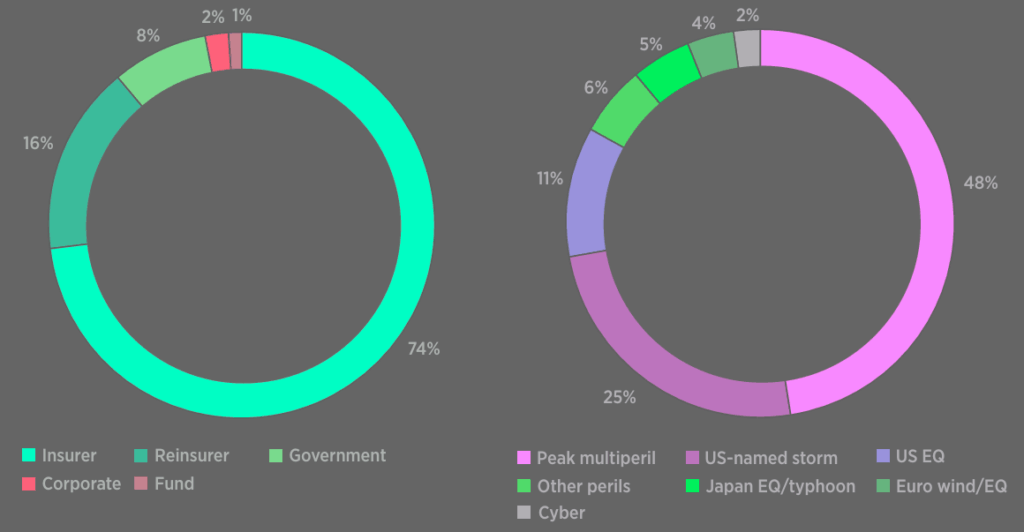

Catastrophe bonds capacity by sponsor type

Aon’s Soeren Soltysiak says the market’s main hurdle isn’t structure or price. It’s knowledge.

While catastrophe bonds dominate discussions, other ILS structures, such as sidecars, are also gaining traction.

These collateralized quota share arrangements offer investors another way to access insurance risk. Tuite points to a slight increase in sidecar capacity in 2024, likely driven by improvements in underlying insurance pricing.

Property CatBond issuance

Investors don’t ignore ILS

Investors don’t ignore ILS; they just aren’t fully comfortable with it in Asia, and education moves slowly when institutions worry about mandate creep, Beinsure analysts said.

We think that hesitation shows up everywhere, even when the data screams that the asset class works. The sense of “newness” persists, although the global market has run for 25+ years.

The regulatory push comes with limits. Steve Tunstall at PARIMA argues the MAS scheme doesn’t solve the return-visitor problem, a sticking point that stops sponsors from committing year after year.

Asia’s biggest cities sit on coastlines, so natural catastrophe exposure piles up fast. Tunstall says private markets can only do so much unless governments step in alongside insurers.

Singapore hosts plenty of reinsurance vehicles with exotic branding but, according to him, many behave like plain-vanilla balance-sheet machines. MAS needs to stretch the market’s “appetite” if it wants depth.

Gallagher Securities notes that more than 100 investors track and trade cat bonds, yet roughly 20 of them set the tone. Capacity clusters in North America, then Europe, with Asia pulling in a sliver.

According to our data, that geographic skew limits how quickly Asia can build its own ILS base because pricing power follows capital, not ambition.

ILS regulators in the region trimmed friction

Regulators in the region trimmed friction by scrapping fund-setup hurdles and rolling out grants. ILS managers hustle harder during fundraising rounds, and Australian and Japanese asset managers already funnel more money into these structures.

Still, Asia’s cyber exposure remains too small to securitise, so no one expects cyber cat bonds to show up soon. Soltysiak says natural catastrophe remains the sensible use case for the next few years. Maybe longer.

The market will thicken once investors stop treating ILS as something exotic and start viewing it as another diversifier that behaves when everything else misbehaves. That shift isn’t happening overnight, but the pieces are on the table.

FAQ

Because investors in the region still treat ILS as unfamiliar territory. The asset class posts strong yields and low correlation, yet institutions hesitate when mandates feel stretched. That lag slows local capital formation even as global returns stay robust.

Two forces. Retained earnings from strong performance recycle into new deals, and fresh capital flows in from both seasoned and first-time investors. Cat bonds draw the biggest share because cedants diversify reinsurance, and investors chase steady pricing and minimal volatility.

According to Swiss Re’s ILS insights, the Government of Jamaica, Farmers in California and Dutch insurer NN joined the roster. They sit alongside long-time sponsors and those returning after multi-year breaks, giving the market a broader mix of transactions.

It strips out a chunk of upfront costs. Asia-Pacific property cat bonds get 70% funding capped at S$1mn, while deals without regional exposure receive 50%. Sidecars and collateralised reinsurance structures hold at 70% with a S$500k cap. Renewals land at 30%. Sponsors run the numbers and suddenly the hurdle looks lower.

Because those regions built the institutional habit early. More than 100 investors follow the space, yet about 20 drive most pricing. Asia has capital, sure, but it arrives slowly because investors want confidence in modelling, structure and local risk data before committing size.

Yes, quietly. Some managers report a small lift in sidecar capacity as underlying insurance pricing improves. They offer a collateralised quota share path that sits beside cat bonds, and investors seem more open to mixing structures as performance stabilises.

Scale. Cyber exposure in the region isn’t large or consistent enough to securitise. Soltysiak says nat cat remains the practical use case for the next few years, and until cyber loss data matures, issuers won’t package it into cat bonds.

……………

AUTHORS: Oleg Parashchak – Editor-in-Chief at Beinsure Media, Nataly Kramer — Lead Editor at Beinsure Media