Overview

The insurance-linked securities (ILS) market reached a record $107bn in capacity by the end of 2024. AM Best Director of ILS Matt Tuite attributes this expansion to strong investor returns, rising catastrophe bond issuance, and shifting investor appetite. However, uncertainties, such as the impact of California wildfires, could influence market dynamics in 2025. Beinsure has selected the main points of his interview.

Key Highlights of the ILS Market Growth

- The insurance-linked securities (ILS) market hit $107 bn in capacity by the end of 2024, driven by strong investor returns, increased catastrophe bond issuance, and renewed investor interest.

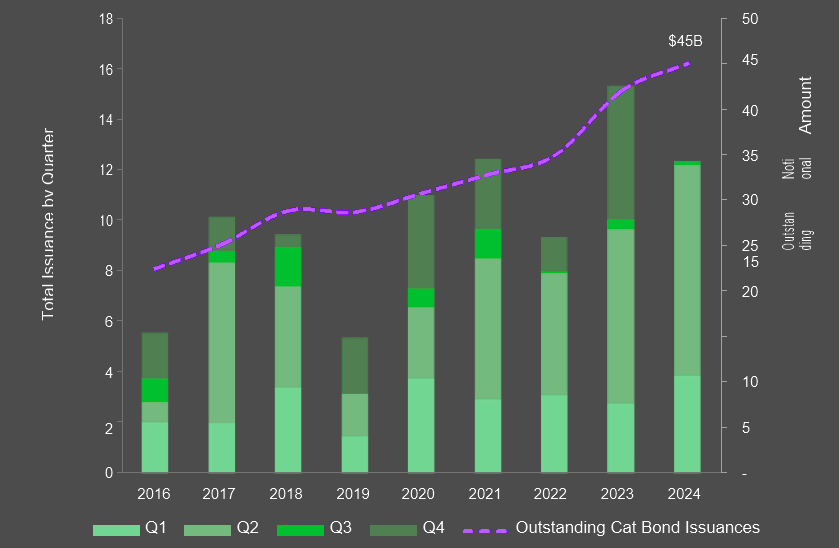

- Cat bond issuance set new records, with market size growing to $45.6bn—an 18% increase. Investors were attracted by higher premiums, low correlation with traditional assets, and improved collateral returns exceeding 5%.

- Some long-time investors returned after observing strong returns, while new entrants saw opportunities in alternative risk transfer. Demand for capital outpaced supply, encouraging more sponsors to issue cat bonds.

- Beyond catastrophe bonds, investors explored sidecars and collateralized reinsurance for exposure to insurance risk. Improved pricing and strong cat bond performance encouraged capital to flow into these areas.

- The impact of catastrophic events like the California wildfires remains uncertain. While no widespread panic has emerged, industry players are closely monitoring how these events could affect market dynamics in 2025.

Investor Returns and Capital Inflows Drive Market Growth

Tuite highlights the role of investor earnings in fueling growth. The ILS market experienced two years of strong returns, leading to reinvestment and an increase in available capital. Additionally, new capital inflows, particularly in the catastrophe bond segment, have contributed to record-breaking capacity.

While this trend has been promising, market participants are monitoring how catastrophic events, such as the recent wildfires in California, might shape future developments.

The market has seen stellar returns, and those retained earnings are being redeployed into new transactions. There’s also fresh capital coming in, both from existing investors and new entrants, particularly in the cat bond space.

In 2024, global natural perils resulted in total direct economic costs of $417 bn. Of this, $154 bn was covered by private insurers and public insurance entities. From 2017 to 2024, insurers faced an average annual loss of $146 bn from natural catastrophes, indicating a “new normal” near $150 bn annually, according to Gallagher Re’s Natural Catastrophe and Climate Report.

Significant natural catastrophes in 2024 affected both developed nations and non-traditional insurance markets. The year began with a strong El Niño phase, transitioning into weak La Niña-like conditions.

Cat Bonds Maintain Momentum

Catastrophe bonds have been the most consistent and rapidly growing segment within the ILS market. Tuite attributes this to their appeal among both cedants and investors. Insurers and reinsurers use cat bonds to diversify their reinsurance sources, complementing traditional markets. Over the past few years, a steady flow of new sponsors has entered the market, alongside those returning after extended breaks.

The demand side remains strong, with primary insurers, reinsurers, and even government-affiliated entities like Florida Citizens participating. On the supply side, investors appreciate the low correlations, and recent returns have been highly attractive.

Record issuance was supported by overwhelming growth of the cat bond market. With nearly $11 bn of maturities over the same twelve months, the market required over $6.9 bn of growth to sustain the issuance volume over this period.

Aon Securities’ Cat Bond Total Return Index shows a 6.3% return in the first seven months of 2024, following an 18.5% return in 2023. These returns stem from higher premiums and better collateral returns, now exceeding 5% for $ transactions. Alternative capital, which includes instruments such as catastrophe bonds, collateralized reinsurance, and sidecars, continues to gain traction. Investors are drawn to the sector by its non-correlated returns compared to traditional asset classes.

Property Catastrophe Bonds Issued and Outstanding

Market participants are closely watching pricing trends and investor sentiment. While uncertainty remains around the impact of California wildfires, there is no widespread panic among industry professionals.

Investors have benefited from wider risk margins, benefiting from the clear value of insurance-linked securities (ILS) diversification. This led to record returns in 2023-2024, a trend persisting into 2025.

Catastrophe bond issuance set records in three of the past four quarters, pushing the market to $45.6 bn—an 18% rise. The catastrophe bond market drew capital inflows starting in early 2023 after Hurricane Ian’s landfall in September 2022, whose impact was less severe than anticipated, according to ILS Annual Report by Aon Securities.

New issuance came from all corners of the market with a record-breaking 64 sponsors bringing 76 transactions in the past year. Issuing entities coming to this market for coverage for the first time along with several who brought their first transactions in a decade drew investor interest with more diverse offerings, and new perils all together.

Shifting Investor Appetite and New Entrants

Investor interest in ILS appears to be evolving. Tuite notes that some long-standing investors had slowed down their activity but are now re-engaging after observing multiple years of favorable returns. Meanwhile, new investors are entering the space after gaining a better understanding of the market and recognizing potential opportunities.

We’re seeing different investors coming in at different points in the cycle. Some have stepped back and are now returning, while others are just getting started after doing their research.

Sponsors, noting the relative value of the cat bond market to traditional reinsurance and the well-known benefits of purchasing cat bond protection seized the opportunity to bring new deals to market, ultimately leading to a demand for capital that outpaced supply by 2024.

Sidecars and Alternative ILS Structures Gain Attention

While catastrophe bonds dominate discussions, other ILS structures, such as sidecars, are also gaining traction. These collateralized quota share arrangements offer investors another way to access insurance risk. Tuite points to a slight increase in sidecar capacity in 2024, likely driven by improvements in underlying insurance pricing.

Cat bonds get a lot of attention, and they’ve delivered strong returns. Once investors see those results, some start looking at other ILS opportunities, including sidecars.

Some investors view catastrophe bonds as a gateway into the broader ILS market. Once comfortable with cat bonds, they explore other structures like sidecars or collateralized reinsurance for additional exposure.

Outlook for 2025

As the ILS market moves into 2025, its trajectory will depend on various factors, including investor sentiment, catastrophe activity, and capital inflows. While the recent growth has been impressive, industry participants are watching potential challenges, such as the long-term impact of recent wildfires.

The market is working through these developments. It’s still early days, and we’ll have to see how things unfold.

With record capital levels and sustained interest in catastrophe bonds, the ILS market remains a key space for both insurers and investors looking for alternative risk transfer solutions.

Newcomers to the market, along with some returning after a decade, attracted investor interest by offering diverse coverage options and new risks. Notably, the introduction of cyber risk to catastrophe bond investors marked a significant step forward for both risk buyers and investors.

This new area of growth positions the ILS market for further expansion, with cyber risk expected to become a growing concern for businesses worldwide.

FAQ

Strong investor returns, increasing catastrophe bond issuance, and a shift in investor appetite fueled the market’s record growth in 2024.

Cedants value catastrophe bonds for diversification, while investors appreciate their non-correlation with traditional asset classes and attractive returns.

Events like the California wildfires could influence market capacity and investor sentiment in 2025, but the full impact remains uncertain.

Yes, both new investors and returning participants have driven growth, with many seeing ILS as an opportunity for alternative risk exposure.

Sidecars, offering collateralized quota share arrangements, have gained interest as investors seek additional ways to access insurance risk beyond catastrophe bonds.

Record issuance was fueled by strong demand, a growing number of sponsors, and investor confidence following years of high returns.

Growth depends on investor sentiment, natural catastrophe activity, and capital inflows, but the market remains well-positioned with strong demand for alternative risk transfer solutions.

………………..

AUTHOR: Matt Tuite – Director of Insurance-Linked Securities (ILS) at AM Best