Overview

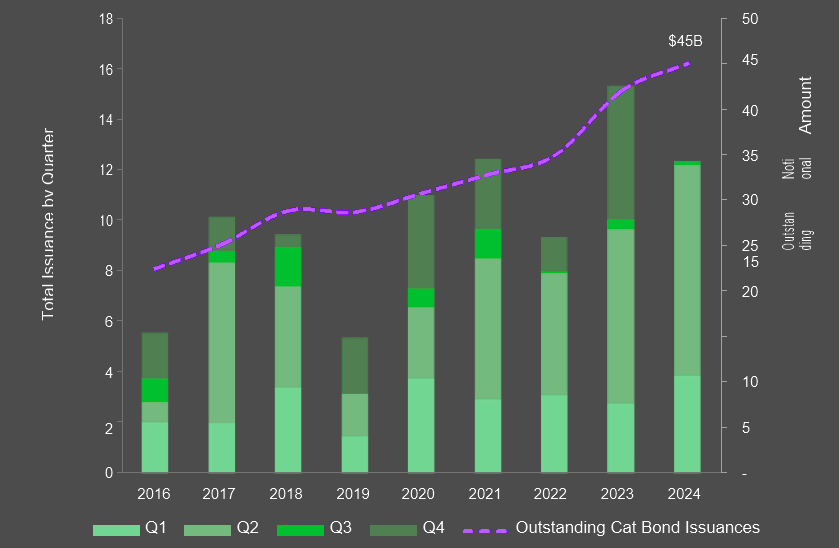

The ILS market remains a significant capital source for insurance and reinsurance companies in 2024. Aon estimates alternative capital at $110 bn, with the catastrophe bond market growing to $45 bn (up $3 bn since January 1, 2024) and an annualized growth rate of 17% since early 2023. Increased capital inflows into catastrophe bonds reflect improved investor returns, according to Aon Report.

Aon Securities’ Cat Bond Total Return Index shows a 6.3% return in the first seven months of 2024, following an 18.5% return in 2023. These returns stem from higher premiums and better collateral returns, now exceeding 5% for $ transactions.

ILS and Global Property Catastrophe Market

The lack of significant catastrophe events in 2023 and 2024, with no principal impairments among the 294 outstanding catastrophe bonds, also contributed to these strong returns.

Alternative capital, which includes instruments such as catastrophe bonds, collateralized reinsurance, and sidecars, continues to gain traction. Investors are drawn to the sector by its non-correlated returns compared to traditional asset classes.

The growing interest in ILS has helped increase the overall capital pool, contributing to more competition and flexibility in pricing.

The global property catastrophe market is in a period of transition, although various markets are at different stages of the cycle. With attractive returns, reinsurers have turned their attention to growth, increasing competition for higher catastrophe layers, according to Global Reinsurance Market Report.

Underlying ROEs were materially higher due to a further reduction in underlying combined ratios and higher recurring investment income. Whether viewed on a headline or underlying basis, reinsurers’ ROEs now comfortably exceed the industry’s cost of capital.

Given recent rate increases and reinvestment rates, it is likely that reinsurers’ underlying ROEs will continue to trend upwards and remain meaningfully above the cost of capital.

Property Catastrophe Bonds Issued and Outstanding

As Aon approach the mid-point of the North Atlantic hurricane season with limited hurricane activity to date, it’s tempting to conclude that a quiet hurricane season will further encourage investors to inject additional capital into the market.

In such a scenario, it’s likely that the catastrophe bond market will continue to grow, and we may see an easing of issuance spreads. Investors will, however, likely continue to seek to maintain overall terms and conditions.

In other parts of the alternative reinsurance capital market, the sidecar market continues to look favorable to investors, largely due to the adequacy of underlying premium margins and relatively limited catastrophe activity of late.

Aon Securities expects this market to maintain its attractiveness through year-end, particularly if the hurricane season only incurs limited losses subject to such sidecars.

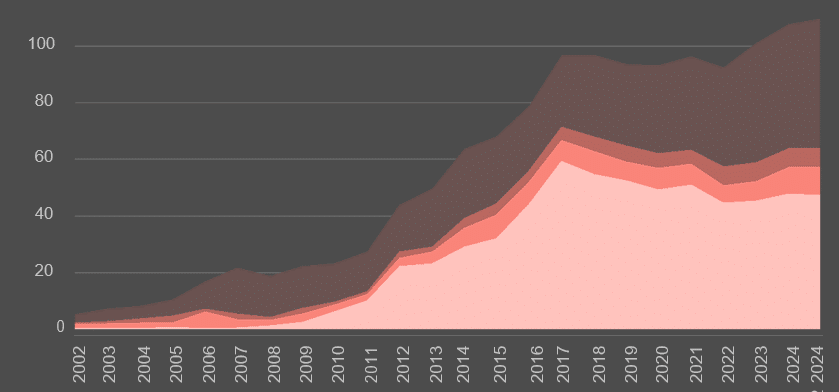

Alternative Capital Deployment (Limit)

Additionally, casualty sidecars are developing based on the combination of improved casualty insurance pricing, higher interest rates, and substantial risk spreads for private credit investments which make these structures possible.

There is less movement in the collateralized reinsurance market and investors continue to prefer the more liquid catastrophe bonds or the well yielding sidecar market.

ILS market saw capital inflows

The ILS market saw capital inflows starting in early 2023, following Hurricane Ian’s landfall in September 2022. The storm’s impact was less severe than expected. Investors gained from wider risk margins, and the benefits of insurance-linked securities (ILS) remained clear to allocators. This led to record returns in 2023, a trend that has continued into 2024.

Insurers, reinsurers, corporations, and governments benefited from the sector’s strong performance as demand for ILS capacity surged due to higher prices in both the insurance and reinsurance markets.

From Q4 2023 through Q2 2024, these conditions fueled new issuances across the market, with 64 sponsors launching 76 transactions, a record high.

Newcomers to the market, along with some returning after a decade, attracted investor interest by offering diverse coverage options and new risks. Notably, the introduction of cyber risk to catastrophe bond investors marked a significant step forward for both risk buyers and investors.

This new area of growth positions the ILS market for further expansion, with cyber risk expected to become a growing concern for businesses worldwide.

………………..

AUTHORS: Mike Van Slooten – Head of Business Intelligence at Aon, Richard Pennay – CEO of Insurance-Linked Securities at Aon