Overview

The total economic loss from global natural catastrophes for H1 2024 was estimated at $128 bn, insured losses totalled at $61 bn, according to Gallagher Re’s report about Natural Catastrophe and Climate. Beinsure Media selected the most important highlights from the report.

US severe convective storm insured losses during past 18 months surpass record $100 bn amid highly active in 2024.

An active first half of 2024 for global natural catastrophes resulted in a near-average financial cost for governments and the insurance industry. The minimum $128 bn in economic loss from all natural perils was slightly lower than the most recent 10-year.

Economic losses from natural disasters reached $128 bn, slightly below the 10-year average of $133 bn. Insurance covered $61 bn of these losses, 25% higher than the decadal average of $49 bn

This increase stemmed from a higher frequency of low- to mid-sized severe convective storm events in the U.S. with strong insurance coverage. Loss totals are expected to rise as more claims are processed throughout the year.

Insurance Industry Face Average Costs from Natural Disasters

Excluding non-atmospheric events like earthquakes and volcanoes, weather and climate-related disaster costs amounted to $113 bn, close to the 10-year average of $117 bn.

This marked the sixth consecutive first half of the year with weather-related losses at or above $100 bn. Insurers covered $57 bn of these losses, 22% higher than the decadal average of $46 bn.

Entering the second half of the year, attention is on the Atlantic hurricane season. Colorado State University, now partnered with the Gallagher Research Centre, predicts a hyperactive season.

This forecast is driven by record Atlantic Ocean warmth and the transition from El Niño to La Niña conditions in the Pacific. The insurance industry must prepare for potential challenges ahead.

H1 2024 global economic loss statistics

Land and ocean temperatures set global records for 13 consecutive months from June 2023 to June 2024, contributing to more unpredictable and extreme events in 2024 due to climate change.

Key points from SCS Insurance Losses:

- Above-average losses for the global insurance industry

- U.S. severe convective storms accounted for 61% of global insured losses

- Over 32 billion-dollar economic loss events

- Over 19 billion-dollar insured loss events, including 12 multi-billion

- El Niño dissipates with La Niña expected in Q3 2024

- Warmest first half of the year on record since 1850

All loss totals are adjusted to 2024 USD, unless stated otherwise, using the U.S. Consumer Price Index, a construction index, and labor cost factors.

Natural Catastrophes Economic Loss

The total economic loss for H1 2024 was preliminarily estimated at $128 bn, which was near the decadal average ($133 bn). This was driven by at least six individual events which resulted in economic losses greater than $5 bn.

Two of these events occurred in Asia, and one each in the United States, Middle East, Europe, and Latin America.

Six events alone accounted for $47 bn (37%) of all economic losses during the first six months. Two other US SCS outbreaks were just under $5 bn.

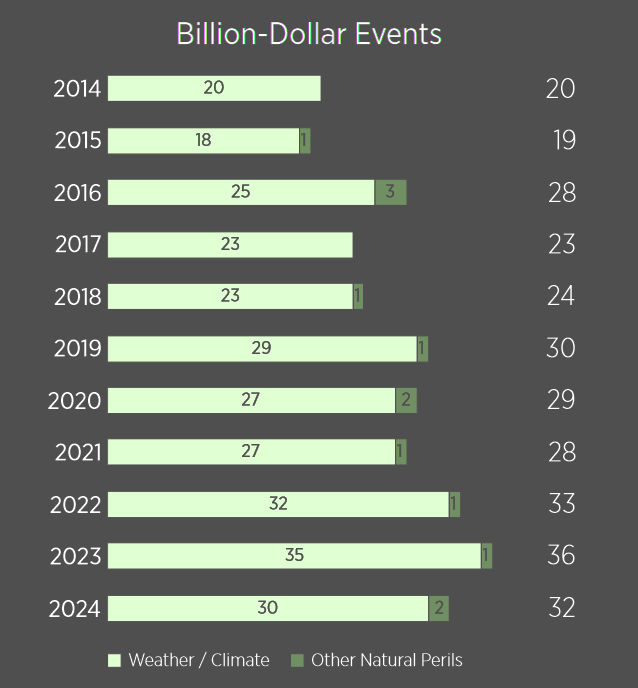

In total there were at least 32 individual bn-dollar economic loss events in H1. This was above the decadal average of 27 such events. These events included 20 in the United States (14 of which were from SCS outbreaks), 6 in Asia, 4 in Latin America, and 1 each in the Middle East and Europe.

Of the 30 significant events, 28 were weather or climate-related, surpassing the 10-year average of 26.

El Niño played a major role in these disasters. Jet stream shifts caused extreme precipitation or drought in parts of South America, Africa, Asia, and the Middle East, leading to substantial costs.

In mid-April, the Middle East, especially the UAE, experienced record-breaking economic losses from flooding, exceeding $8.5 bn.

Summary of natural catastrophe economic loss

Brazil faced similar flooding from April to May, resulting in over $8 bn in losses in Rio Grande do Sul. Intense drought affected Mexico, South America, and Southeast Asia.

The most expensive peril, by far, was again SCS. It accounted for at least 41% of natural catastrophe economic losses in H1. The $53 bn in global SCS losses were 36% higher than the decadal H1 average ($39 bn).

Flooding (30%) and earthquake (12%) were the only other perils that accounted for at least 10% of economic losses. While global inflation rates continued to slowly decline; supply, construction, labor, and claims litigation costs remained elevated and still had sizeable influence on disaster costs.

In the first half of the year, the United States incurred at least $59 bn (46%) of economic disaster costs. This exceeded the decadal average, with further losses anticipated from storms, floods, and droughts in the coming months.

In Asia, economic disaster costs reached at least $31 bn (24%), slightly below the average.

However, an active monsoon season in East Asia at the end of H1 and early Q3 is expected to increase losses. The Middle East experienced above-average losses, Latin America met the average, while Europe, Africa, and Oceania remained below average.

Historically, the first half of the year has been less costly than the second half. From 2014 to 2023, H1 economic losses represented 37% of the annual total. A single major catastrophe can significantly change the annual loss trajectory.

Top 10 Costliest Economic Events

The United States accounted for four of the top 10 costliest events of H1 2024. However, the top three costliest events occurred in Asia, the Middle East, and Latin America.

| Event Name | Region | Economic Loss ($) | Insured Loss ($) |

| Noto Peninsula Earthquake | Asia | 12,000 | 3,000 |

| Arabian Gulf Flash Floods | Middle East | 8,550 | 2,820 |

| Rio Grande do Sul Floods | Latin America | 8,100 | 2,000 |

| China Seasonal Floods | Asia | 7,000 | 440 |

| Mid-March SCS Outbreak | US | 5,900 | 4,700 |

| Central Europe Floods | Europe | 5,000 | 2,160 |

| Mid-May SCS Outbreak | US | 4,900 | 3,675 |

| Early May SCS Outbreak | US | 4,800 | 3,750 |

| Hualien Earthquake | Asia | 3,000 | 1,200 |

| Early Jan SCS & WW | US | 2,800 | 2,225 |

| Grand Totals | 128 bn | 61 bn |

There were six individual events which resulted in at least $5.0 bn in economic losses. All but two of the top 10 events were weather-related.

Natural Catastrophes Insured Loss

H1 2024 insured losses were preliminarily estimated at $61 bn, surpassing the decadal average of $49 bn. This figure, expected to rise in the coming weeks and months, includes payouts from private insurers and public insurance entities.

There were 19 individual billion-dollar loss events, marking the second highest H1 total on record, just behind 2023 and 2022, each with 20 events. Twelve of these events resulted in multi-billion-dollar losses.

The costliest peril was severe convective storms, with global losses exceeding $40 bn, most of which ($37 bn) occurred in the United States. The US recorded 13 individual billion-dollar storm outbreaks, eight of which surpassed $2 bn.

Summary of natural catastrophe insured loss

The costliest event in H1 was a mid-March outbreak, resulting in $4.7 bn in claims. Hail was the primary cause of insured costs across central and eastern US, but tornadoes and non-tornadic winds, including a derecho in Houston, TX, also contributed significantly.

The $37 bn H1 total makes 2024 the fourth costliest year for US convective storm losses, following 2023 ($63 bn), 2020 ($45 bn), and 2011 ($41 bn).

Flooding accounted for over $10 bn, with multiple non-US events causing multi-billion-dollar impacts. Significant events included Japan’s Noto Peninsula earthquake ($3 bn), Arabian Gulf Coast flash flooding in mid-April ($2.8 bn), Central Europe (Germany) flooding in late May and early June (>$2.1 bn), and Brazil’s Rio Grande do Sul flooding in late April and early May ($2 bn).

Weather and climate events drove 93% of H1 2024 insured losses, slightly below the decadal average of 95%.

This percentage is expected to rise as further loss data from Q1/Q2 events are reported. There is a multi-month lag in reporting public insurance payouts, especially in agriculture. As the harvest period arrives in Q3/Q4, farmers assess the impact of early-season weather on yields, leading to more claims.

The US accounted for over $43 bn (70%) of the H1 total, above the decadal average of $32 bn. US losses are expected to increase in the coming months. Other regions with higher-than-average H1 insured losses included Asia, Latin America, and the Middle East.

Top 10 Costliest Insured Events

The United States accounted for six of the top 10 costliest insured loss events of H1 2024. Each of the top 10 events resulted in a multi-bn-dollar insured loss for private and public insurers.

| Event Name | Region | Economic Loss ($) | Insured Loss ($) |

| Mid-March SCS Outbreak | US | 5,900 | 4,700 |

| Early May SCS Outbreak | US | 4,800 | 3,750 |

| Mid-May SCS Outbreak | US | 4,900 | 3,675 |

| Noto Peninsula Earthquake | Asia | 12,000 | 3,000 |

| Arabian Gulf Flash Floods | Middle East | 8,550 | 2,820 |

| Early Jan SCS & WW | US | 2,800 | 2,225 |

| Central Europe Floods | Europe | 5,000 | 2,160 |

| Rio Grande do Sul Floods | Latin America | 8,100 | 2,000 |

| Early April SCS Outbreak | US | 2,550 | 2,000 |

| Houston Derecho | US | 2,550 | 2,000 |

| Grand Totals | 128 bn | 61 bn |

All events but one were weather–related. The six US events were all severe convective storms, which further highlights how this peril continues to drive significant annual loss costs for the US insurance market.

Two additional US SCS events also led to a multi-bn-dollar loss but are not shown in this top 10 table. The Arabian Gulf flash flood event was poised to be one of the costliest, if not most expensive, individual weather events on record for the local insurance industry.

……………….

AUTHORS: Steve Bowen – Chief Science Officer at Gallagher Re, Brian Kerschner – Western Hemisphere Meteorologist at Gallagher Re, Jin Zheng Ng – Eastern Hemisphere Meteorologist at Gallagher Re