Overview

- Large M&A transactions continued to shape the market structure

- Volume of M&A deals completed globallly

- Regional M&A divergence

- APAC leads insurance M&A rebound

- The United States will likely remain the centre of global deal flow

- Europe M&A trends

- Middle East and Africa recorded the smallest share of deals globally

- Insurance M&A market drivers and looking ahead in 2026

Global insurance M&A stabilised in 2025, as insurers and brokers took a more strategic approach to acquisitions amid falling interest rates and a realignment of strategic priorities, Clyde & Co’s annual Insurance Growth Update reveals.

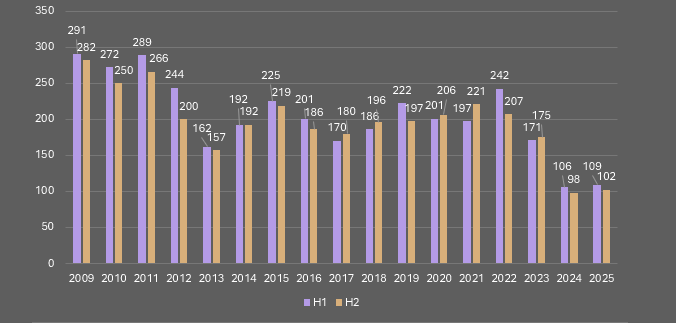

Globally, the market recorded 211 completed transactions worldwide in 2025. The figure rose slightly from 202 deals the year before. Deal flow therefore stabilized after the steep contraction observed during 2024.

Activity still remained well below the recent peak. In 2023 the sector closed 346 transactions globally, the strongest period for insurance M&A in several years.

Large M&A transactions continued to shape the market structure

During 2025, buyers completed 15 deals valued at $1 bn or more. Seven of those transactions qualified as mega deals. Each exceeded $5 bn in total value.

According to Beinsure analysts, the shift toward fewer but larger acquisitions reflects a more disciplined approach among insurers and brokers pursuing scale, distribution reach, and technology capabilities.

Dealmaking was muted over 2024, which marked a 16-year low in response to global instability. Rather than a full recovery, 2025 has represented a stabilisation in markets such as the UK and Europe, with selective acceleration in APAC.

Activity has been driven by portfolio optimisation and geographic refocussing, as carriers have shifted their focus from a ‘growth at all costs’ mindset to evaluating strategic fits.

This has highlighted a clear divergence in the market, with steady and selective carrier activity sitting alongside strong, continued momentum among intermediaries, brokers and MGA platforms.

Volume of M&A deals completed globallly

| Full year regional comparison | |||

| Region | 2023 | 2024 | 2025 |

| Global | 346 | 204 | 211 |

| Americas | 162 | 92 | 77 |

| Europe | 107 | 56 | 57 |

| APAC | 52 | 39 | 59 |

| MEA | 15 | 17 | 15 |

2025 saw four undisclosed deals complete with location anonymised hence a larger global value than the sum of regional deals.

Regional M&A divergence

The APAC region not only saw the strongest acceleration in dealmaking in 2025 at 59 transactions compared to 39 in 2024, the region also held the majority (four) of mega deals valued at over $5 bn.

Japanese insurers have been active acquirers and, following domestic portfolio adjustments, have significant capital available for overseas expansion.

Amongst APAC’s major deals, two took place in Japan, and Clyde & Co expects Japanese groups’ appetite for strategic, cross-border acquisitions to continue in 2026.

| Mega deals (exceeding $5 Bn) | ||

| Region | Country | Value ($ Bn) |

| Americas | United States | 5.101 |

| United States | 5.31 | |

| Europe | Switzerland | 10.21 |

| APAC | Japan | 8.2 |

| Japan | 6.95 | |

| Taiwan | 8.25 | |

| Hong Kong | 10 | |

APAC leads insurance M&A rebound

Yvonne Lam, partner at Clyde & Co, said the Asia-Pacific region delivered the strongest insurance M&A performance during 2025.

Deal activity recovered across the region, with several large transactions occurring in Japan.

- Australia also benefited from growth across the broader APAC insurance market. According to Lam, insurers and brokers increased strategic acquisitions as new specialty players entered the sector and international groups reorganised regional structures to simplify operations.

- Japanese insurers continue driving expansion across Asia. Strong capital positions and ongoing international growth plans support outbound acquisitions. Lam expects APAC to remain a major engine of global insurance deal activity during 2026.

- The region’s traditional financial centres, including Hong Kong, Singapore and China, remain focal points. Emerging markets such as India and Thailand also attract growing interest from insurers seeking higher growth opportunities.

Peter Hodgins, another partner at Clyde & Co, expects insurance M&A to accelerate modestly during 2026. He said pent-up demand and large pools of private capital will likely fund bolt-on acquisitions across insurance distribution and specialty underwriting.

In 2026, we expect a cautious but clear uptick in insurance M&A, driven by pent-up demand and abundant private capital targeting strategic bolt-ons.

Peter Hodgins, Partner at Clyde & Co

“Activity should stay US-led, but we’ll see more cross-border moves into higher-growth emerging markets, for example, in the Middle East, where access to licences, talent and local partnerships is commanding a premium”.

The United States will likely remain the centre of global deal flow

Hodgins added that cross-border acquisitions should expand, especially into higher-growth markets including the Middle East, where insurers place premium value on licences, local expertise and partnerships.

The Americas recorded 77 transactions during 2025, compared with 92 in 2024. Even with the decline, the region still produced the largest share of global insurance deals.

The United States continues shaping international M&A activity

Multinational insurers headquartered there often drive large global transactions. In 2025 the U.S. market recorded 52 deals, including eight valued above $1bn.

American managing general agents and insurers increasingly pursue international expansion strategies. Clyde & Co expects outbound acquisitions from the U.S. to continue during 2026.

In Latin America, the market recorded six completed transactions during 2025. Deal numbers remain limited, though structural growth drivers continue strengthening.

Large populations, expanding access to digital banking and rising financial inclusion create opportunities in segments such as warranty and indemnity insurance. According to Beinsure analysts, these structural shifts could support higher deal volumes over time.

Europe M&A trends

Europe recorded 57 transactions during 2025, slightly above the 56 deals completed the previous year. Several insurers have renewed interest in accessing the Lloyd’s of London platform.

Some companies that previously reduced their presence in the market now consider returning.

The largest European transaction occurred in Switzerland and reached a value of $10.2 bn.

Middle East and Africa recorded the smallest share of deals globally

The region produced 15 transactions in 2025, slightly below the 17 deals completed the previous year.

Cross-border acquisitions formed a visible portion of global activity. Data shows 43 cross-border transactions completed during 2025.

Clyde & Co expects international dealmaking to expand further in 2026. Broader financial sector conditions support this shift. Cross-border consolidation trends already appear in European banking, where macroeconomic conditions increasingly favour international acquisitions.

Insurance M&A market drivers and looking ahead in 2026

In 2025, acquisitions were partly driven by strategic considerations, such as the drive to diversify or as an opportunity to add new capabilities and deepen expertise in market segments, such as speciality.

We saw this begin in 2024 with Zurich Insurance Group’s acquisition of AIG’s travel business, which represented a move to cement its global position in business travel insurance.

This trend in strategic moves to strengthen specialisations ramped up in 2025 and will continue to shape dealmaking in 2026.

“This past year has almost been a “tale of two cities”, as activity has been selective and steady on the carrier side, but in the intermediary space, particularly with MGA’s and brokers, we’re seeing continued momentum and a real depth of interest in the sector,” Eva-Maria Barbosa, Partner at Clyde & Co, said.

Insurers have sharpened their focus on specialty lines resulting in a clear emergence of strategic opportunities across energy transition-related risks, cyber and AI exposures, and contingency business tied to large multinational events.

We expect this to continue into 2026 resulting in steady deal flow and targets thoughtful M&A.

Companies are divesting from markets where they no longer see sufficient value or where regulatory changes allow them to operate more efficiently through alternative licensing structures.

Insurers are investing in regions

Meanwhile, firms are investing in regions where they believe they can achieve growth by diversifying their businesses or strengthening their position within niches.

Significant deal flow stems from intermediaries, brokers and MGA platforms, and many of these businesses are backed by private equity and are actively seeking expansion opportunities.

Geopolitical instability, however, remains a risk to the trajectory of dealmaking, as it could disrupt sector confidence, and the prospect of rising interest rates could increase the cost of capital and dampen deal appetite.

In 2026, following on from the year’s first ‘mega deal’ with Zurich’s acquisition of Beazley, there is expected to be strong activity rather than a dramatic acceleration.

Clyde & Co expects firms to seek expansion into Africa and parts of APAC outside the established hubs of Hong Kong, Singapore and China. With capital abundant, there will be continued momentum as insurers and brokers continue to pursue growth opportunities.

FAQ

Global insurance M&A stabilised in 2025 after the sharp slowdown seen in 2024, with 211 completed transactions compared with 202 deals the year before. Despite the slight increase, activity remained well below the 2023 peak of 346 transactions.

Insurers and brokers shifted away from a “growth at all costs” mindset and began prioritising acquisitions that improved strategic fit, strengthened capabilities, expanded distribution, or supported geographic refocusing.

Yes. In 2025, the market recorded 15 deals valued at more than $1 bn, including seven mega deals exceeding $5 bn, showing a shift toward fewer but larger and more strategic acquisitions.

The Asia-Pacific region led the rebound in deal activity, with transactions increasing from 39 in 2024 to 59 in 2025, and the region accounting for the majority of mega deals.

The United States remained central to global M&A activity, recording 52 deals in 2025 and continuing to drive large international transactions and outbound acquisitions.

Europe recorded 57 transactions in 2025, slightly higher than the 56 deals completed in 2024, with renewed interest among insurers in accessing the Lloyd’s of London platform.

Insurance M&A is expected to increase modestly in 2026 as pent-up demand and large pools of private capital support bolt-on acquisitions, cross-border expansion, and strategic investments in specialty insurance segments.

…………………….

AUTHORS: Peter Hodgins – Partner at Clyde & Co, Eva-Maria Barbosa – Partner at Clyde & Co, Yvonne Lam – Partner at Clyde & Co