Overview

Global reinsurance pricing softened more than many market participants expected at the Jan. 1, 2026 renewals, according to Moody’s Ratings, as early-year California wildfire losses failed to move the needle and the 2025 Atlantic hurricane season stayed quiet.

Moody’s said property catastrophe pricing landed slightly lower than anticipated. Insured natural catastrophe losses still cleared $100 bn globally in 2025, yet the loss mix mattered.

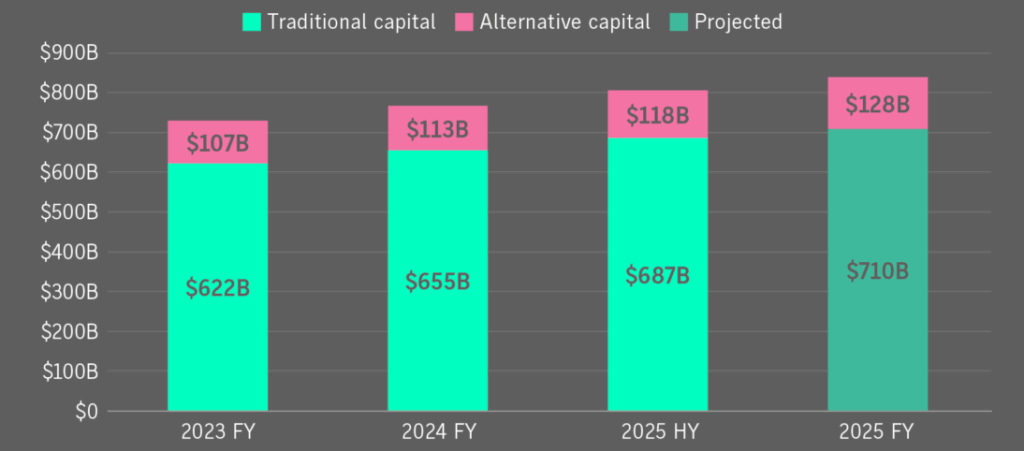

Global reinsurance dedicated capital totaled $769 bn at full-year 2024, a rise of 5.4% versus the restated full-year 2023 base. Reinsurance capital reached a record high at 2025 with about 8% growth in traditional capital to $710 bn while alternative capital grew by approximately 12% to $128 bn.

Key highlights

- Global reinsurance pricing fell more than expected at the Jan. 1, 2026 renewals, with property catastrophe rates down about 15% on average as abundant capital outweighed catastrophe loss support.

- California wildfire losses and over $100 bn in global nat cat losses failed to lift pricing because severe convective storm losses now sit largely with primary insurers after the 2023 market reset.

- Reinsurance capital reached record levels, with total capacity nearing $838 bn in 2025, widening the supply-demand gap and accelerating buyer-friendly renewal conditions.

- Attachment points largely held, but early easing emerged as some reinsurers accepted lower attachments and increased exposure to frequency-linked covers such as aggregate and second- and third-event protection.

- Property renewals favored buyers, while casualty pricing proved more resilient due to litigation pressure and loss development, keeping most casualty renewals flat to slightly higher.

A combination of accelerated price softening in the property segment with a modest relaxation of certain terms and conditions, as well as ongoing challenges in the casualty space, the heightened frequency and severity of natural catastrophes, and ongoing macroeconomic uncertainty, has caused AM Best to revise its global reinsurance sector outlook to stable from positive.

Jan. 1, 2026 reinsurance renewal outcomes

| Segment | Pricing outcome | Key driver |

| Global property catastrophe | −10% to −20% | Excess capital, weak catastrophe support |

| Risk-remote upper layers | Sharper declines | Oversupply, low loss attachment |

| Specialty lines | Broadly lower | Competitive pressure across classes |

| Casualty reinsurance | Flat to +5% | Litigation trends, loss development |

| Retrocession | −15% to −17% | Capital inflow, reduced demand |

Fitch Ratings has changed its outlook for the global reinsurance sector from “improving” to “neutral,” noting that the pricing cycle has likely peaked. However, profitability is expected to stay strong by historical standards through 2025.

Global reinsurance market delivered strong results in 2024 with further improvement in underwriting profitability, exceptional ROEs and a continued building of capital. Reinsurer capital buffers and reserve levels have improved, supported by record profits in 2023 and the first half of 2024.

Reinsurers are well-prepared for price declines, despite rising claims costs and increasing catastrophe losses driven by climate change.

Reinsurers absorbed a meaningful share of the LA wildfire claims

While reinsurers absorbed a meaningful share of the Los Angeles wildfire claims, severe convective storms dominated the year. Those losses now sit largely with primary insurers after the 2023 market reset.

That shift muted pricing support. Convective storm activity didn’t translate into reinsurance momentum, even with headline loss totals looking large on paper.

At the Jan. 1 renewals, primary insurers saw noticeable price declines, especially in risk-remote property layers at the top of programs. Specialty lines followed a similar pattern.

Moody’s said competition spread across regions and classes.

Throughout 2025, AM Best said, reinsurance pricing started to soften from the recent highs following the property market reset in 2023, and this trend accelerated at the recent January 2026 renewals, with property catastrophe rates declining by around 15% on average.

But while competitive pressures have increased in the property cat space, with supply outpacing incremental new demand at 1.1 2026, sellers do remain disciplined with terms and conditions and attachments largely intact, while reinsurers’ risk-adjusted capital position remains robust as a result of retained earnings and prudent capital deployment.

Global reinsurance market has entered a post-peak pricing phase, with earnings expected to moderate in 2025-2026.

Even as rates soften, the ratings agencies maintains a stable outlook on the reinsurance sector, pointing to strong capitalization, underwriting discipline, and sustained profitability above the cost of capital.

Despite pressure to broaden coverage and lower attachment points, S&P noted that underwriting discipline across the global reinsurance industry has remained intact, and reinsurers have retained strong capitalisation.

Global property catastrophe reinsurance rates fell

Broker data shows global property catastrophe reinsurance rates fell about 15% on average at 1.1. Even so, returns remain attractive relative to where pricing started.

Property reinsurance renewals were off 10% to 20% as abundant capital outpaced demand at Jan. 1 reinsurance renewals.

Casualty lines were less forgiving as litigation issues and loss development continues to weigh on markets but still allowed many cedents to renew flat from last year.

Reinsurance capital is expected to reach a record high at year-end 2025 with about 8% growth in traditional capital to $710 bn while alternative capital grew by approximately 12% to $128 bn as of Sept. 30 for a total of $838 bn, a 4.2% increase from year-end 2024.

Global reinsurance capital

“Most insurers and reinsurers are in robust financial health, reaping the benefits of years of structural adjustments and rate rises in both primary and reinsurance markets,” Gallagher Re, the reinsurance business of broker Arthur J. Gallagher & Co., said in a report.

Renewals favored buyers in property markets, while “continued concerns over elevated loss trends and loss development in the U.S. dominated discussions on casualty renewals

Broker Howden also noted the overall buyers’ market. “Conditions are shifting towards buyers as competition intensifies and rates decline, albeit from elevated levels,” Howden said.

Global reinsurance capital position

| Capital type | 2024 | 2025 | YoY change |

| Traditional capital | $657 bn | $710 bn | 8% |

| Alternative capital | $114 bn | $128 bn | 12% |

| Total reinsurance capital | $769 bn | $838 bn | +4.2% |

| Factor | Impact on reinsurance pricing |

| Global insured losses > $100 bn | Limited support |

| California wildfire losses | Partial reinsurer absorption |

| Severe convective storms | Retained by primaries |

| Atlantic hurricanes | Minimal impact |

| Loss mix | Reduced relevance for reinsurers |

AM Best has not observed significantly lower retentions on reinsurance programs. Instead, the changes have been more focused on broadening policy wording and narrowing exclusions.

These changes can have a meaningful, but typically lesser, impact than more substantive structural changes to reinsurance programs.

Aggregate/frequency products have re-emerged more plentifully than last year but have not returned broadly to pre-hard-market structures. Deployment remains highly selective and analytics-driven.

Terms, conditions, and structure reinsurance trends

| Feature | 2023 reset | Jan. 1, 2026 status |

| Attachment points | Raised sharply | Mostly stable |

| Aggregate covers | Reduced | Selective return |

| Frequency exposure | Avoided | Gradual increase |

| Second/third event covers | Limited | More available |

| Underwriting discipline | Tight | Largely intact |

Reductions reinsurance pricing levels

The reductions returned reinsurance pricing levels to where they were about four years ago, according to a renewals report from Howden, which recorded a 14.7% decline in global property catastrophe placements at Jan. 1 along with a 16.5% decline in property retrocession placements.

Specialty markets also saw reductions, although aviation losses in 2024 made negotiations complex and reductions were less universal than in property and casualty, according to both brokers.

Moody’s expects reinsurers to respond by pushing more capital back to shareholders through dividends and buybacks as underwriting margins compress.

The easing comes after a sharp tightening phase. In 2023, reinsurers lifted rates, pulled back from frequency-heavy structures, cut aggregate protections, and raised attachment points.

The goal was balance sheet protection, not earnings smoothing.

That stance held in broad terms this year. Attachment points stayed mostly intact. Still, Moody’s flagged early signs of relaxation. Competitive pressure increased as supply growth outpaced incremental demand.

Reinsurance coverage expands as reinsurers show stronger risk appetite

Some cedents secured reinsurance coverage at lower attachment points. Reinsurers also showed greater willingness to take on frequency-linked exposure, including aggregate covers and second and third event protection. The shift remains selective, but it’s there.

Moody’s pointed back to its September 2025 reinsurance buyer survey. That work already showed momentum swinging toward price cuts in property, with casualty more mixed.

According to industry reports, 2025 is yet another year that saw insured losses from natural catastrophes exceed $100 bn, but as noted by AM Best, with the exception of the costly California wildfires in January, the profile of individual events in the year was insufficient to impact reinsurer results in a meaningful way, driven in part by the higher attachment points enforced by the market.

As a result, 2025 is expected to be another strong year of profitability with the sector poised to exceed its cost of capital for the third year in a row.

“The sustained period of strong results has led to robust capital generation that has reinsurers searching for opportunities to deploy capacity. Reinsurance capacity is projected to enter 2026 at record levels: approximately $540 bn in traditional dedicated reinsurance capital and $120 bn in ILS capital, bolstered by a third consecutive year of robust earnings. As a result, competitive pressures have increased,” says AM Best.

Forward-looking market signals (2025–2026)

| Area | Direction |

| Reinsurance pricing | Continued softening |

| Underwriting margins | Narrowing |

| Capital returns | Increasing dividends, buybacks |

| Buyer leverage | Strengthening |

| Sector outlook | Stable, profitable above cost of capital |

January outcomes leaned even more cedent-friendly

For property reinsurance lines, 75% of surveyed buyers expected price decreases, roughly half anticipating drops of 5% or more. Casualty buyers mostly expected flat pricing or increases capped around 5%.

Final results edged below those expectations. California wildfire losses didn’t provide sustained pricing support. Hurricane losses stayed low. The gap between capital supply and risk demand widened.

The pandemic revealed the fragility of health and liability frameworks. Monetary tightening forced a reset of solvency models and capital distribution. Climate-linked disasters kept stressing traditional approaches to risk.

Softer pricing at reinsurers’ June and July reinsurance renewals supports view that abundant capacity and rising competition will continue to pressure prices.

Declining reinsurance prices, increased claims severity from natural catastrophe events, and slightly looser terms and conditions (T&Cs) in property lines are expected to reduce underwriting margins in 2025, Beinsure noted.

The global reinsurance sector has undergone a notable transformation since the market reset in 2023, drawing sustained attention from investors and analysts. Rather than a surge of new start-up reinsurers, capital has returned through more deliberate channels, according to AM Best’s Market Segment Report.

Reinsurers are still benefiting from elevated reinvestment yields, even as central banks begin an easing cycle.

“Current yields remain above those of longer-dated bonds now maturing from legacy portfolios, allowing reinsurers to steadily lift investment income while the higher cost of capital continues to reinforce underwriting discipline,” says AM Best.

Inflation trends, monetary policy shifts, and broader geopolitical uncertainty leave the future path of interest rates unclear.

Still, with most non-life portfolios concentrated in the three- to five-year duration range, reinsurers are positioned to earn relatively elevated levels of interest income for several more years, providing a durable tailwind even if headline rates begin to drift lower.

Expanding on casualty reinsurance, AM Best says: “Several reinsurers strengthened casualty reserves in 2024 and 2025 and AM Best expects this trend to continue in 2026.

In some cases, unfavorable loss reserve development in long-tail lines has been partially or entirely offset by favorable development from property, specialty, and workers’ compensation reserve releases, although the buffer derived from potential excess reserve positions in other lines may be diminishing.

“Capacity limits have been reduced and rate hikes continue to be observed in the most volatile lines, such as commercial automobile, general liability, and excess liability, but systemic risks nevertheless remain unresolved. Whether the meaningful pricing gains seen for the past several years are keeping pace with loss cost trends is questionable. Casualty therefore remains a fragile area of opportunity, balancing investor appetite for diversification against mounting volatility.”

FAQ

California wildfire losses early in the year failed to support pricing, while the 2025 Atlantic hurricane season stayed quiet. Losses exceeded $100 bn globally, but the mix mattered. Severe convective storms dominated, and those losses now sit largely with primary insurers after the 2023 market reset.

Broker data shows global property catastrophe reinsurance rates fell about 15% on average at the Jan. 1 renewals. In some programs, declines ranged from 10% to 20%, especially in risk-remote upper layers where capacity was plentiful and competition intensified

Capital levels hit record highs. Global reinsurance dedicated capital reached about $769 bn at year-end 2024. By 2025, traditional capital rose roughly 8% to $710 bn, while alternative capital grew around 12% to $128 bn. The supply-demand imbalance widened, pushing prices lower despite elevated loss activity.

Attachment points stayed largely stable, but Moody’s flagged early signs of easing. Some cedents secured coverage at lower attachment points. Reinsurers also showed greater willingness to write frequency-linked covers, including aggregate and second- and third-event protection. The shift remains selective, not broad-based.

Casualty pricing held up better. Litigation trends and adverse loss development limited rate relief. Many buyers renewed flat year over year, with increases generally capped around 5%. Concerns over US casualty loss severity dominated renewal discussions.

Gallagher Re said most reinsurers remain in strong financial shape after years of rate rises and structural changes. Howden described a clear shift toward a buyers’ market, noting pricing has rolled back to levels seen about four years ago. S&P Global Ratings maintains a stable sector outlook, citing strong capitalisation and underwriting discipline.

Moody’s expects underwriting margins to narrow as pricing softens and terms loosen modestly. Capital return through dividends and buybacks is likely to rise. According to Beinsure analysts, abundant capacity, rising competition, and softer mid-year renewals point to continued pressure on reinsurance prices, even as profitability stays above the cost of capital.

…………………

Written by by Yana Keller – Lead Re/Insurance Editor at Beinsure Media