Overview

Global reinsurance market delivered strong results in the first half of 2024 with further improvement in underwriting profitability, exceptional ROEs and a continued building of capital. Earnings resilience has further increased through a higher underlying ROE which provides reinsurers with additional buffer to absorb headwinds.

According to Gallagher Re Report, the reinsurance industry earned a 7% margin over the cost of capital on an underlying ROE basis at 2024 HY, with the underlying ROE at almost 2x the cost of capital.

Reinsurers have now fully recouped for weaker profit years (2017-2020) and on a cumulative basis for 2017-2024 HY the SUBSET generated a ROE above the cost of capital.

The increase in the underlying underwriting margin is driven by the meaningful improvement in underlying combined ratio. The underlying underwriting margin increased from 2.7% a year ago to 3.9% (see 2024 Reinsurance Renewals).

Reinsurer revenue and combined ratio

Revenue growth remained strong in 2024 at 9%, similar to the 2023 growth rate. Growth was driven primarily by rate increases rather than volume growth. Volume growth was limited due to shifts in business mix and rising attachment points.

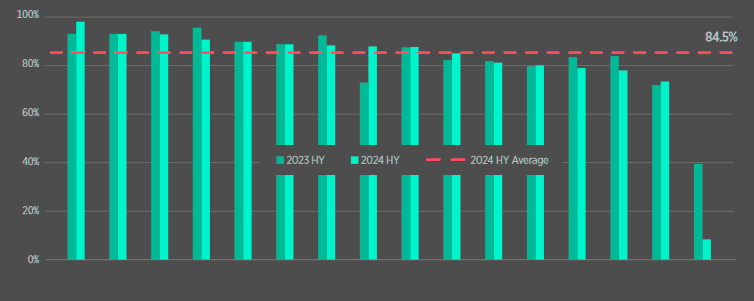

The combined ratio dropped to 84.5%, marking a record low since 2014. This occurred despite a 0.7 percentage point (ppt) decrease in reserve releases and a 0.6 ppt rise in the expense ratio.

The improvement was primarily due to a reduction in the attritional loss ratio (from 68.8% to 66.5%), reflecting rate earn-through and less reserve prudence from some firms, alongside a lower impact from natural catastrophe losses (from 6.8% to 5.6%).

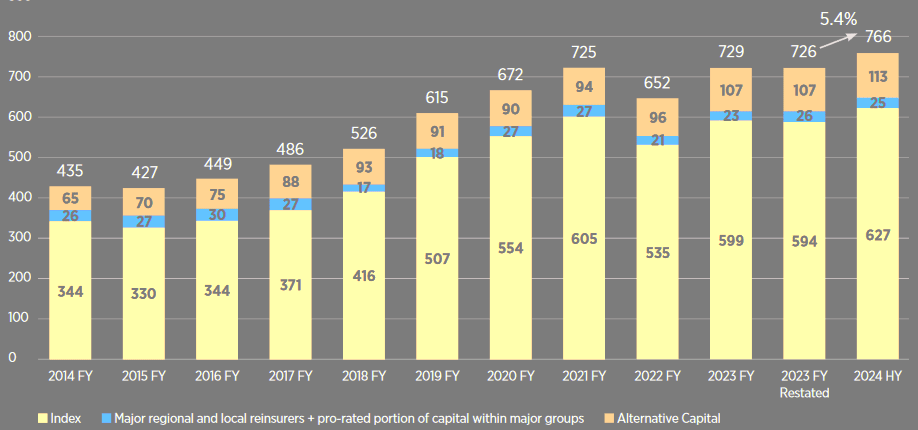

Global reinsurance dedicated capital increases

Global reinsurance capital rose 5.4% in H1 2024, reaching $766 bn. Since 2020, capital growth (+14%) has lagged behind premium growth (+21%) due to rising demand and inflationary pressures.

The reinsurance capital of INDEX companies, which account for 82% of total reinsurance capital, increased by 5.6% to $627 bn.

Non-life alternative capital grew by $6 bn (+5.6%) to $113 bn, driven by higher earnings and capital inflows, particularly in catastrophe bond mandates (see Global Reinsurance Capital & Catastrophe Bond Market Dynamics).

Underwriting margin drives the uplift in underlying ROE

| Year | 2022 | 2023 | 2024 |

| Reported ROE, % | 4.4 | 19.0 | 19.6 |

| Remove impact of discounting | -1.5 | -1.0 | -0.4 |

| Remove nat cats | 3.7 | 4.6 | 3.2 |

| Add in normalized nat cats | -7.2 | -7.2 | -5.3 |

| Remove prior year development | -1.3 | -1.3 | -0.7 |

| Strip out investment gains/losses | 12.1 | -1.6 | -1.0 |

| Underlying ROE, % | 10.2 | 12.5 | 15.5 |

| Composition of Underlying ROE | |||

| Underlying underwriting margin | 1.6 | 2.7 | 3.9 |

| Running investment income | 7.1 | 10.6 | 11.3 |

| Other income/expenses | 1.5 | -0.7 | 0.3 |

| Underlying ROE, % | 10.2 | 12.5 | 15.5 |

- Looking at the components of the underlying ROE, the improvement in underlying underwriting income and running investment income are key factors behind the increasing underlying ROE.

- The increase in the underlying underwriting margin is driven by the meaningful improvement in underlying combined ratio. The underlying reinsurance underwriting margin increased from 2.7% a year ago to 3.9%.

- The increase in interest rates has materially increased the running investment income and as a result the investment margin contribution increased to 11.3%, from 10.5%.

Most reinsurers reported lower combined ratios

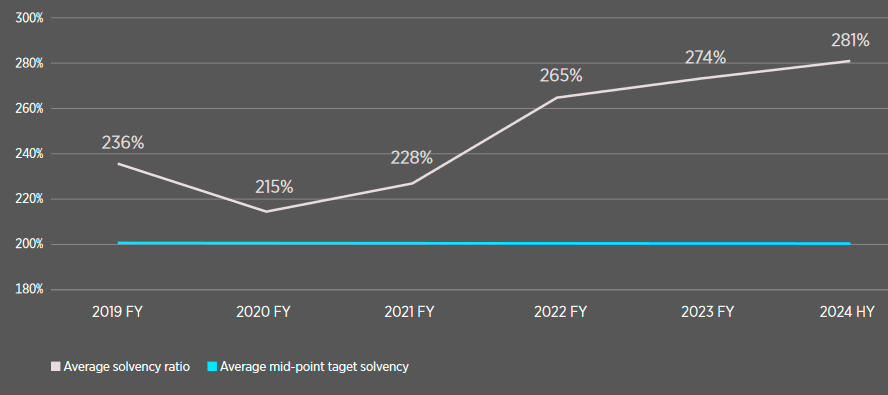

In addition to accounting-based growth, global reinsurers’ capital adequacy remains strong on an economic basis, a metric Gallagher Re considers more relevant for management decisions.

Economic capital adequacy comfortably above target levels for most European reinsurers

The TOP 5 European reinsurers averaged a solvency ratio of 281% (2023: 274%), exceeding most management targets.

Largest European reinsurers, Munich Re, Swiss Re, and Hannover Re, saw further improvements in earnings in 2024, driven by better underwriting results across most business lines.

SCOR reported a loss due to unfavourable changes in its life and health insurance reserving assumptions, according to Fitch Ratings and AM Best.

Fitch Ratings believes largest European reinsurers are well-positioned to handle potentially less favourable market conditions. Their credit ratings remained stable in the ‘AA’ and ‘A+’ range.

TOP 10 Reinsurers by Net Written Premium

| Rank | Reinsurer | Net written premium, $mn |

| 1 | Munich Re | 31 587 |

| 2 | National Indemnity | 16 908 |

| 3 | Hannover Re | 12 171 |

| 4 | MAPFRE | 11 353 |

| 5 | RGA | 9 296 |

| 6 | Everest Re | 7 984 |

| 7 | Arch Capital | 7 866 |

| 8 | SCOR | 7 057 |

| 9 | Renaissance Re | 6 038 |

| 10 | WR Berkley | 5 978 |

TOP 10 Reinsurers by Total Capital

| Rank | Reinsurer | Capital, $mn |

| 1 | National Indemnity | 249 916 |

| 2 | Munich Re | 39 546 |

| 3 | Swiss Re | 29 033 |

| 4 | Fairfax | 27 713 |

| 5 | Great West Lifeco | 22 555 |

| 6 | Arch Capital | 20 665 |

| 7 | Markel | 15 949 |

| 8 | Hannover Re | 15 784 |

| 9 | General Re | 15 528 |

| 10 | China Re | 14 061 |

TOP 10 Reinsurers by Net Income

| Rank | Reinsurer | Net income, $mn |

| 1 | National Indemnity | 55 818 |

| 2 | Munich Re | 4 069 |

| 3 | Arch Capital | 2 369 |

| 4 | Swiss Re | 2 088 |

| 5 | Fairfax | 1 692 |

| 6 | Everest Re | 1 457 |

| 7 | Great West Lifeco | 1 447 |

| 8 | Markel | 1 275 |

| 9 | Hannover Re | 1 255 |

| 10 | Renaissance Re | 860 |

Reinsurers reported a solid average return on equity of 15.5% in the first half of 2024, though slightly below the 20.5% achieved in the same period of 2023.

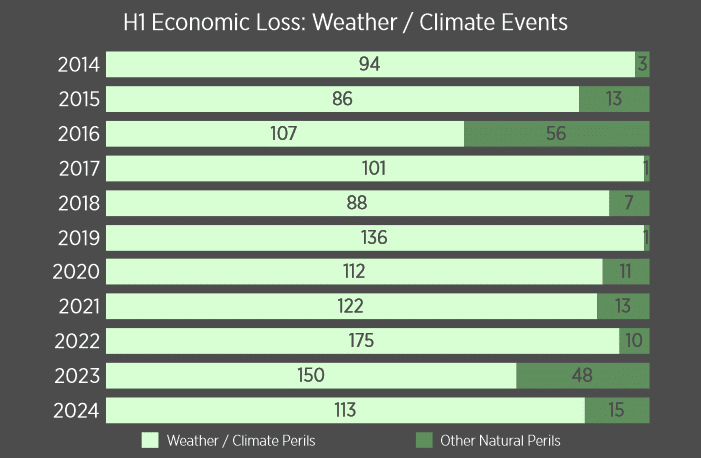

Reinsurers saw a better natural catastrophe outcome

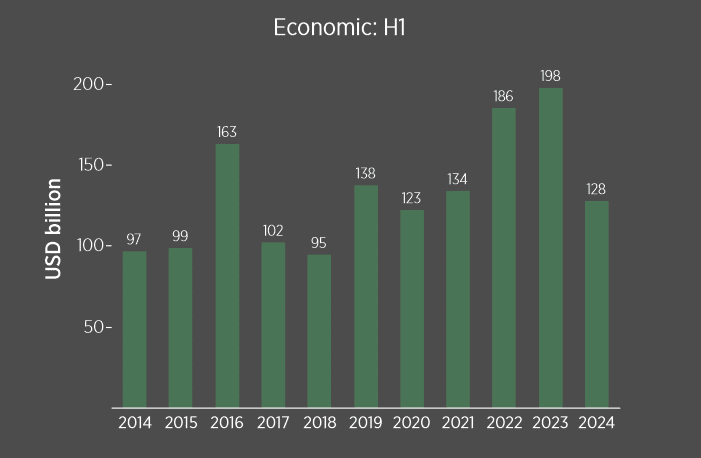

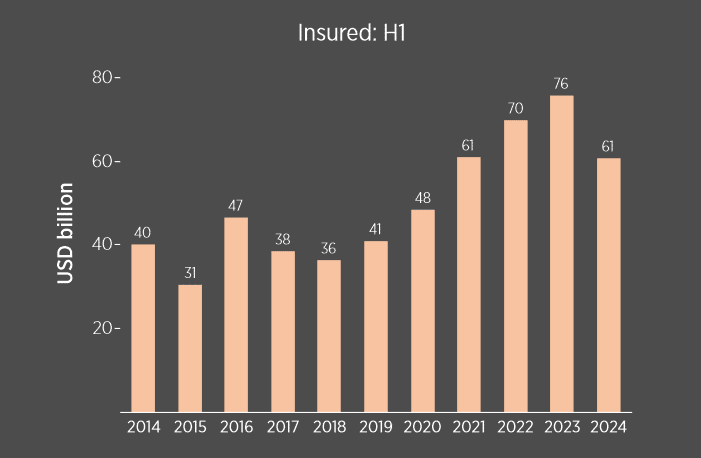

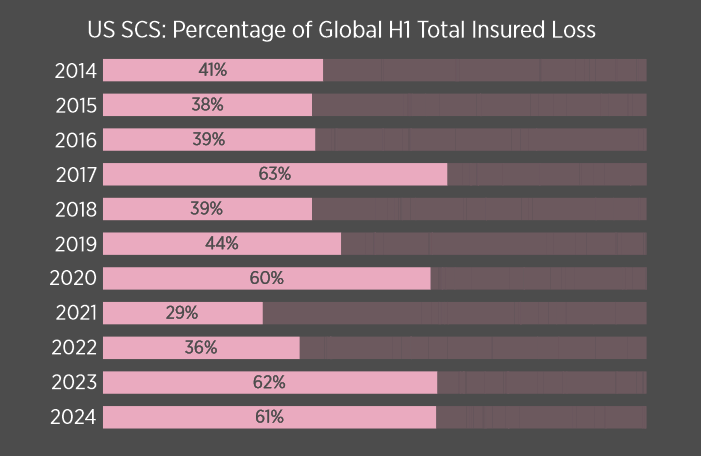

Reinsurers saw a better global natural catastrophe outcome, contrasting with the broader market, where Gallagher Re estimates insured natural catastrophe losses remained high at $61bn in 2024.

Largest reinsurance companies took on a smaller share of these losses, down from 7.7% in 2023 to 5.8% in 2024.

This reduction stems from higher attachment points and the nature of 2024’s losses, which were dominated by secondary perils rather than US hurricanes.

Economic Loss from natural catastrophe

On an underlying basis, the combined ratio improved further, dropping from 96.1% to 93.6%, also a record since the start of the time series. This was supported by a better attritional loss ratio and a reduced charge for normalized natural catastrophe events.

The reported return on equity (ROE) stabilized at 19.6% for 2024, remaining exceptionally strong. The underlying ROE increased by 2 ppts to 15.5%, driven by improved underwriting margins and higher investment income.

The reinsurance industry achieved a 7% margin above the cost of capital based on underlying ROE, which was nearly double the cost of capital. This marks the third consecutive year of underlying ROE exceeding the cost of capital.

Insured Loss from natural catastrophe

As a result of the strong profit improvement over the past 2-3 years, the industry has now fully recouped for weaker profit years (2017-2020) and on a cumulative basis for 2017-2024 the SUBSET generated a ROE that is approximately 110% of the cost of capital.

The running yield is now increasingly in line with new money yield. However, despite the recent decline in interest rates, there still seems to be some modest upward pressure on running yields.

We estimate underlying ROEs could improve by a further 1-1.5ppts as a result of higher running yields over time based on current new money yields. This would imply, other things equal, that underlying ROEs could increase to around 17%.

All of this puts the industry in a strong position to absorb any potential earnings volatility. If interest rates continue to decline this could over time lead to a reduction in running yields again. However, long-term interest rates would need to decline by more than 2ppts from current levels for the underlying ROE over time to reduce to levels in line with the WACC, all else being equal.

It has been predicted that the 2024 hurricane season may be hyperactive. We estimate that even in a scenario where reinsurers’ H2 natural catastrophe losses were very significantly higher than average normalized levels, the SUBSET should be well positioned to still deliver a ROE above the WACC on a full year basis.

Reinsurance capital up due to strong net income

INDEX capital rose by $33 bn to $627 bn, driven by strong net income of $78 bn, partially offset by $34 bn in unrealized investment depreciation, largely from National Indemnity.

Net income of $78 bn, up from $22 bn in the first half of 2023, was primarily boosted by National Indemnity’s $51 bn in realized investment gains.

This increase was further supported by higher underwriting and investment profitability, with the latter benefiting from a 0.6 percentage point rise in the running yield and positive gains yield.

INDEX companies returned 14% of their net income through buybacks and dividends, totaling $11 bn.

The net balance of capital raises versus debt reduction amounted to just $2 bn. However, as shown in Chart 1, non-life alternative capital grew by 5.6%.

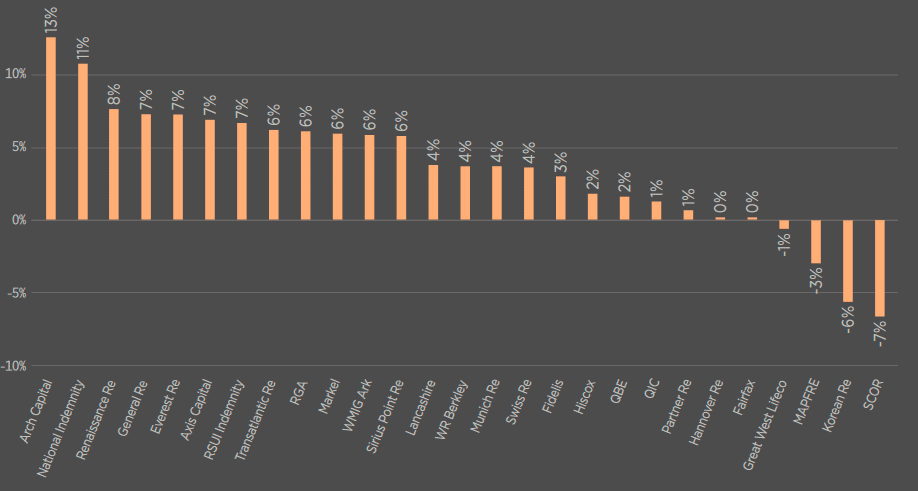

Capital rises for the majority of INDEX companies

Most INDEX companies reported higher capital bases, primarily due to strong net income growth.

Arch Capital’s capital rose 13%, driven by $2.3 bn in net income, supported by solid underwriting and investment profitability. National Indemnity’s capital increased by 11%, with 8 percentage points attributed to gains in its investment portfolio value.

SCOR’s capital fell by 7%, due to a retained loss from reserve strengthening in its Life & Health business. However, SCOR’s Property & Casualty Reinsurance segment remained profitable, with a combined ratio of 87%.

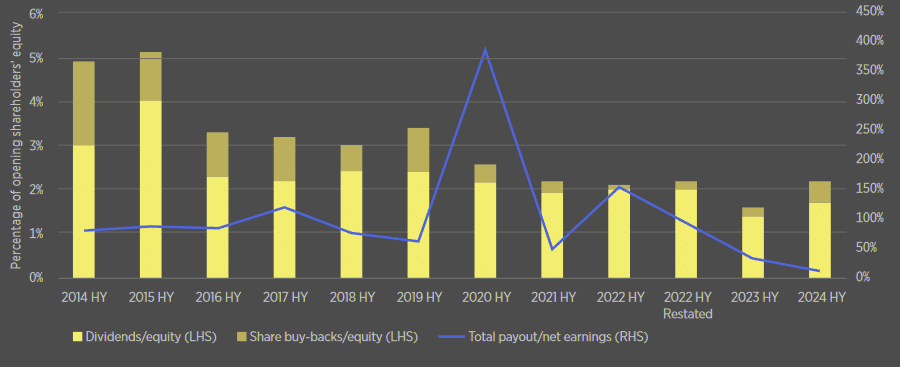

Return of reinsurance capital

Total capital return (dividends plus buy-backs) as a percentage of shareholders’ equity increased to 2.2% (2023: 1.6%).

As is generally the case at half-year, capital return was mainly through dividends, which comprised 77% of the total. The top four European reinsurers contributed almost two thirds of these dividends (2023 HY: 66%).

Despite a 41% increase in total capital returned, the payout ratio as a percentage of net earnings reduced to 13% (2023: 34%) due to higher net earnings driven by an increase in realized investment gains by National Indemnity to $51 bn.

This ratio is typically more volatile than capital return as a percentage of shareholders’ equity because capital levels are usually more stable than earnings. Trends in capital payout as a percentage of shareholders’ equity should therefore be more informative.

………………….

AUTHORS: James Vickers – Chairman Gallagher Re International, Michael van Wegen – Head of Client & Market Insights, International, Global Strategic Advisory