Overview

The Lloyd’s of London market is a globally significant hub for specialty (re)insurance, operating within a complex and dynamic environment. Accurately predicting underwriting performance is crucial for stakeholders, but traditional methods often fall short, according to white paper by Hampden Risk Partners and Insurance Capital Markets Research.

New research reviews the prospective performance potential of its underwritten portfolio, drawing inspiration from sophisticated AI-driven tools used in sports analytics.

The unique characteristics and complexities of the Lloyd’s market present distinct challenges for performance analysis.

While traditional methods often focus on historical absolute performance figures, these can be heavily influenced by market cycles, making it difficult to truly distinguish outperformers from the rest.

Key Highlights

- In soft markets, absolute metrics may inflate performance across the board, while in challenging markets even well-managed syndicates can appear to underperform, making them unreliable indicators of true capability.

- Comparing a syndicate’s results directly to its peer group offers a more stable and meaningful measure of performance, independent of broader market cycles.

- Benchmarking underwriting teams or syndicates against competitors shows greater consistency over time than absolute loss ratios, due to stable renewal books and enduring collaborative relationships.

- ICMR’s Bayesian AI model, inspired by sports analytics, leverages advanced probabilistic programming and market data to forecast relative performance effectively, identifying genuine outperformers.

- By applying relative performance insights, HRP has built a portfolio that outperforms a notional market benchmark, with higher expected returns, better diversification, and lower volatility.

Absolute metrics may inflate performance across the board in a soft market or make even well-managed syndicates appear to underperform in a challenging market.

The Shift to Relative Performance Analysis in Lloyd’s

Recognising this limitation, the focus is shifting to understanding relative performance – how a syndicate performs compared to its peer group.

Understanding who is truly outperforming or underperforming their direct competitors provides a more stable and insightful indicator of underlying capabilities and strategic effectiveness.

Relative performance enables more accurate benchmarking, helps identify genuine competitive advantages and offers a clearer picture of long-term sustainability, independent of broader market fluctuations.

Although the theories have been around for some time – indeed, the founders of ICMR introduced this concept at Lloyd’s while heading up its internal analytics and research function – having access to relevant performance data outside of Lloyd’s internal reporting and the wide availability of probabilistic programming languages is new.

The performance of underwriting teams

The relative performance of underwriting teams, or indeed entire syndicates when benchmarked against their competitors, displays a far greater degree of consistency than their absolute loss ratio performance (see Challenge for Reinsurers’ Underwriting Margins).

This observation is logical, considering the enduring collaborative relationships and size of substantial renewal books.

This is exactly what can be observed in sports as well. The positions of sports teams in league tables can vary throughout the year, but at the end of the season it is more often than not the same teams occupying the top of the leaderboard.

The principle of predicting relative performance, crucial for determining winners in sports, is directly applicable to the Lloyd’s market.

ICMR has curated gross underwriting performance data by syndicate and class of business and developed an innovative AI-powered model, inspired by techniques used in sports analytics, to predict the relative loss ratio performance of Lloyd’s syndicates.

The underlying Bayesian AI model is specifically based on models used in sports analytics to predict relative performance, such as the Plackett-Luce model, which is designed for predicting the rank performance of peers.

The foundation of ICMR’s model consists of the following components:

- Data Ingestion: Collecting and integrating a broad set of publicly available data, including historical syndicate gross underwriting results by line of business, premium volumes, expense ratios, and relevant macroeconomic indicators.

- Feature Engineering: AI algorithms extract and construct key predictive features from the raw data that indicate relative loss ratio performance, extending beyond simple historical averages.

- Probabilistic Programming: Advanced probabilistic programming algorithms, trained on extensive Lloyd’s market data, detect complex patterns and forecast future relative loss ratio performance. These algorithms continuously adjust as new data becomes available, improving predictive accuracy.

- Correlation Analysis: The model learns the rank correlation between syndicates writing similar lines of business, providing insights into diversification among syndicates, which is essential for portfolio management.

- Forward-Looking Performance: Forward-looking relative performance metrics can be combined with absolute market-level performance to better understand the expected distribution of individual syndicate outcomes.

The model assumes that each peer has an ‘ability’ parameter, enabling calculation of the probability of achieving a specific rank or level of relative performance (see Reinsurance Renewals & Rate Reductions in 2025).

The model can also incorporate additional parameters, such as a noise parameter, to emphasize recent performance or results during significant event loss years.

Limitations of the Modelling Approach

While syndicate-level performance data by line of business provides valuable insights, certain limitations should be recognized:

Data Reconciliation and Mapping

Although total performance figures are consistent with audited statements, the detailed business line breakdown in the notes remains unaudited.

Mapping internal underwriting classifications to standardized reporting categories often requires compromises, particularly for syndicates operating in highly specialized niches.

Nonetheless, high annual renewal rates, around 70% for many syndicates, ensure significant portfolio consistency, making peer comparisons a meaningful indicator of relative performance within a given niche.

Reporting Basis

The historical underwriting performance data is presented on a GAAP calendar year basis rather than on an underwriting year basis, which aligns more directly with insurance cycles.

However, GAAP performance has historically served as a reliable leading indicator of underwriting year results over longer periods and relative GAAP performance remains a strong signal of relative underwriting year performance.

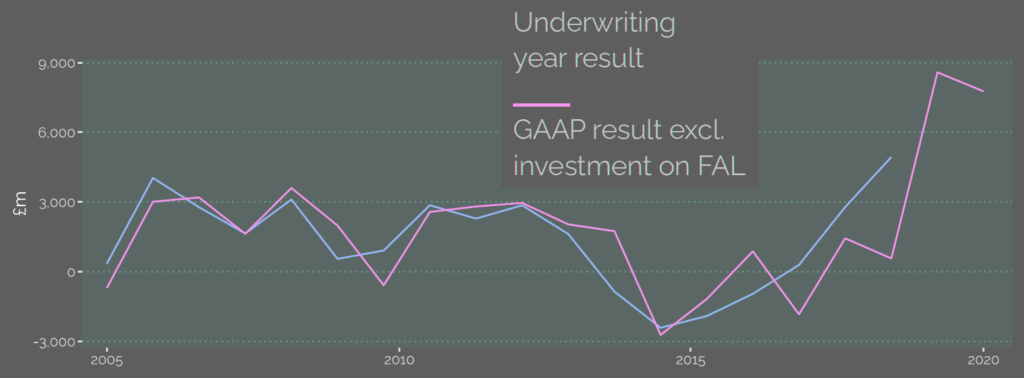

Lloyd’s pro-forma pre-tax results

Lloyd’s pro-forma pre-tax and underwriting year results over the past 20 years. Comparing calendar yearGAAP results with the year of account results, the mismatch for 2022 shows that the underlying underwriting result was still highly positive.

HRP Portfolio Performance Potential

HRP commissioned ICMR to review the underwriting performance potential of its follow-only strategy implemented for Lloyd’s syndicate 2689.

The analysis involved reviewing the impact of the changes to the portfolio since current management took over for the 2023 year of account, adopting its new follow-only business model.

Over the past three years the strategy doubled its premium volume and increased the number of syndicates followed from 11 to 18, while the business mix remained fairly consistent.

Improving risk reward profile

Using its predictive relative performance model, ICMR simulated the performance for all syndicates participating in the same classes as HRP 2689 and market level.

These simulations were then aggregated according to HRP’s business mix to construct a statistical peer group representing a notional Lloyd’s market portfolio with a similar business mix.

This notional portfolio serves as the benchmark against which the HRP portfolio is compared to evaluate its portfolio selection quality.

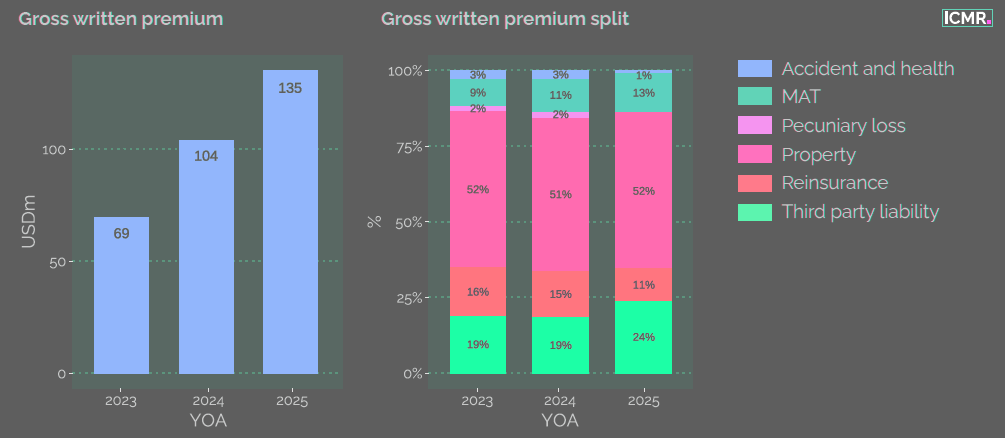

Gross written premium

HRP 2689 GWP is expected to double from YOA 2023 – 2025, while the class of business mix remainslargely unchanged.

ICMR’s analysis shows that the notional HRP portfolio, when compared against the equivalent notional Lloyd’s market portfolio with a similar business mix, is consistently expected to outperform.

Furthermore, the evolution of the portfolio is incrementally improving its potential reward whilst at the same time reducing its volatility. The HRP strategy appears to be successfully targeting its growth with counterparties of proven quality at the same time as improving diversification benefit.

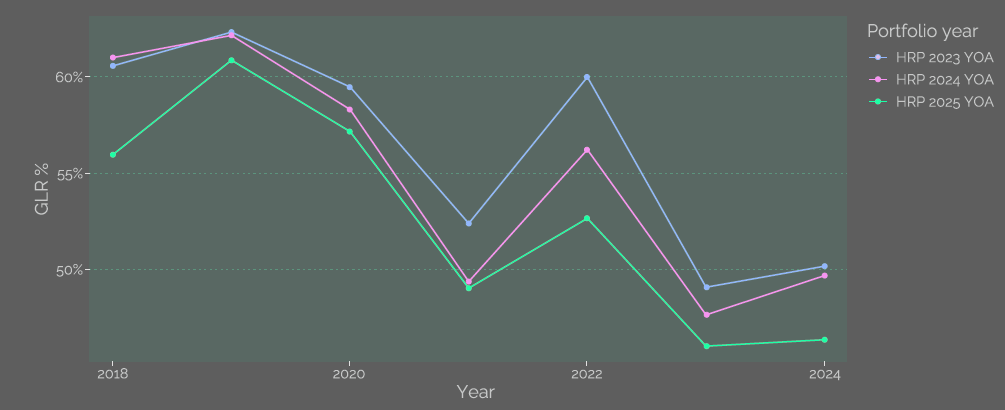

Historical ‘as-if’ gross loss ratio track record

The improving predictive performance is driven by the improving historical track record of the portfolio underwritten over the past three years.

The historical ‘as-if’ track record of the business underwritten by HRP since the 2023 year of account demonstrates improved underwriting quality.

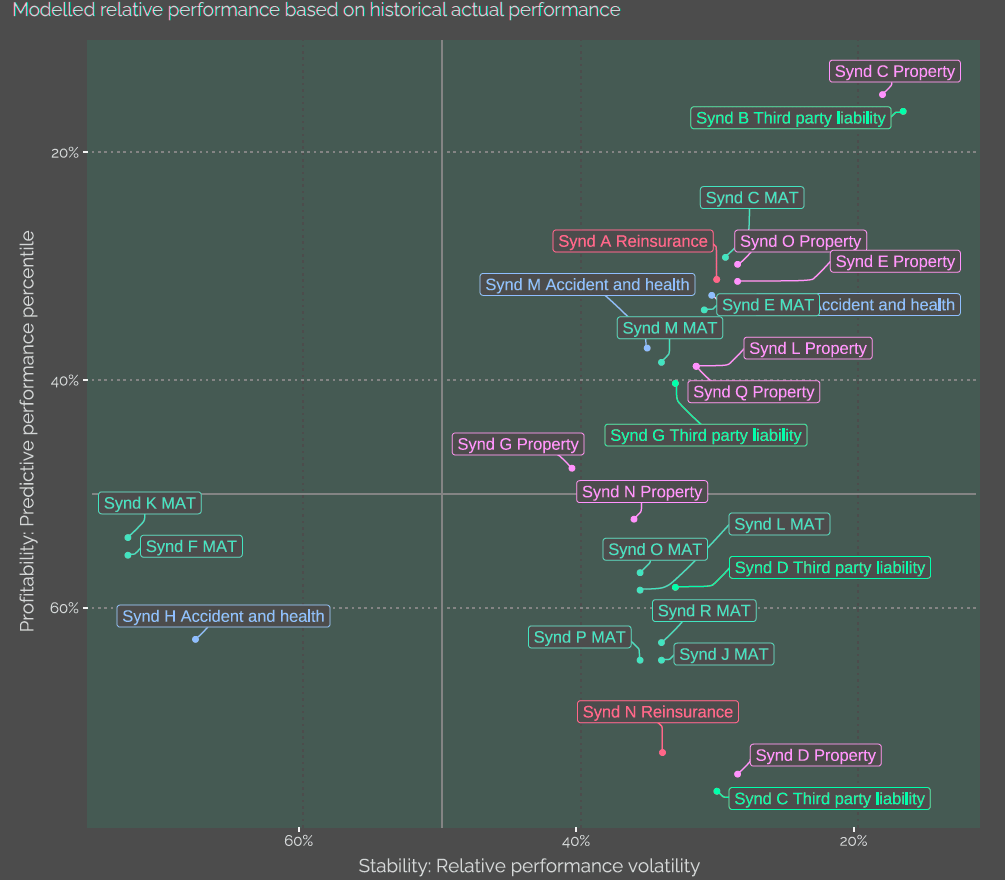

Class of Business Analysis

Reviewing the model output at a class of business level reveals the drivers of the expected performance. The following chart exhibits the predicted performance percentile for the syndicates and classes followed by HRP.

The optimal scenario involves strong relative performance coupled with consistent delivery of that performance, i.e. top right quadrant.

HRP’s portfolio is heavily weighted (70% of premiums) towards investments exhibiting these characteristics.

Profitability vs Stability: Simulated performance perce

Chart shows the predictive relative performance and stability of the syndicates and lines of businessfollowed by HRP for the 2025 YOA.

Aggregating the simulation to a class of business level demonstrates that except for MAT (Marine, Aviation & Transportation) all classes are expected to achieve a performance percentile better than 50%, i.e. top or second quartile gross underwriting performance, with the HRP property book being the ‘star’ performer.

The Winning Strategy – Improving absolute results

The ultimate purpose of this relative performance analysis is to demonstrate improved underwriting outcomes.

This can be achieved by overlaying the relative model with absolute market level perspectives to produce a full market distribution of outcomes, and HRP’s tracking against that.

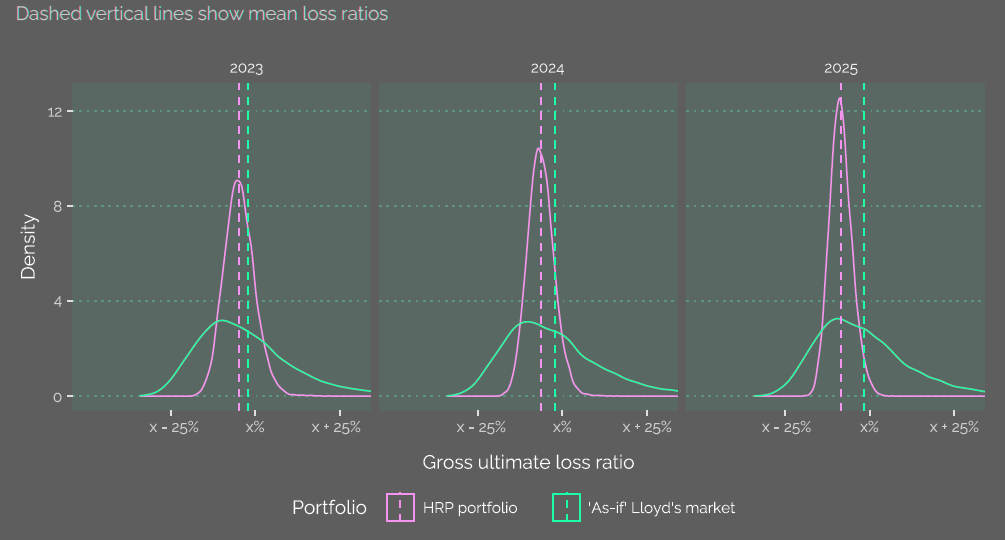

The notional HRP portfolio exhibits lower volatility, and a reduced mean loss ratio compared to the equivalent notional ‘As-if’ Lloyd’s market portfolio.

Simulated Gross Ultimate Loss Ratio Distributions

This analysis evidences the HRP management’s track record in successfully building its portfolio with counterparties of proven quality, so improving underwriting outcomes over time. In addition, it is also improving the diversification benefit with the narrowing of its own distribution.

Strategic Advantages for HRP

Predicting relative performance using ICMR’s AI-powered model provides significant strategic benefits for Hampden Risk Partners (HRP).

- Underwriting Strategy: Identifying syndicates and lines of business that consistently outperform enables HRP to refine its risk selection and identify opportunities for profitable growth.

- Capital Allocation: The analysis highlights syndicates with a high likelihood of sustained relative outperformance, supporting informed capital deployment decisions.

- Syndicate Management: HRP gains objective, data-driven insights into its performance against peers, which supports performance evaluation, target setting, and resource allocation.

- Investor Communications: Delivering a sophisticated, predictive view of future performance improves transparency and strengthens investor confidence.

- Competitive Advantage: A deeper, data-driven understanding of relative performance allows HRP to anticipate market changes, identify emerging risks and opportunities, and strengthen its position in the competitive Lloyd’s market.

ICMR’s analysis aligns directly with HRP’s strategy by showing that its approach successfully targets growth with strong counterparties while reducing volatility and improving potential returns.

Relying solely on traditional absolute performance metrics in the Lloyd’s market provides an incomplete view. Focusing on relative performance and applying AI produces a new level of predictive insight.

Through its collaboration with ICMR and the use of an AI-powered model, Hampden Risk Partners has adopted a more stable, insightful, and valuable method for understanding and forecasting portfolio performance.

ICMR’s analysis demonstrates that HRP’s strategic approach achieves a portfolio with higher expected performance and lower volatility than a relevant market benchmark. For HRP, predicting relative performance represents a decisive and effective strategy rather than a purely analytical exercise.

FAQ

Accurately predicting underwriting performance is crucial for stakeholders because traditional methods often fail to identify true outperformers. Market cycles can obscure performance, making it difficult to distinguish syndicates with genuine competitive advantages.

Traditional methods focus on historical absolute performance, which is influenced by overall market conditions. HRP shifts focus to relative performance — how a syndicate performs compared to its peers — providing a more stable and meaningful measure of underlying capability and strategy.

Absolute metrics can appear inflated during soft markets or make well-managed syndicates appear weak during challenging conditions. Relative performance, by comparing directly against competitors, identifies genuine strengths and weaknesses, offering a clearer picture of long-term sustainability.

The Lloyd’s market features unique characteristics, such as specialized niches, collaborative relationships, and high renewal rates, which complicate performance benchmarking. Traditional data is also reported on a GAAP calendar year basis, which does not align perfectly with insurance cycles.

ICMR uses a Bayesian AI-powered model inspired by sports analytics. It combines data ingestion, feature engineering, probabilistic programming, correlation analysis, and forward-looking metrics to forecast syndicate performance relative to peers. The model accounts for historical data, diversification, and the ‘ability’ of each syndicate.

Data mapping involves compromises, especially for specialized syndicates, and the detailed line-level data is unaudited. Additionally, results are based on GAAP calendar year data rather than underwriting year, though GAAP remains a strong long-term indicator of relative performance.

HRP’s follow-only strategy for syndicate 2689 has doubled premium volume, improved underwriting quality, and reduced volatility. By targeting syndicates with proven performance, HRP has consistently outperformed a notional market benchmark, strengthened investor confidence, and improved its risk-reward profile while enhancing diversification.

……………….

AUTHORS: Markus Gesmann – Co-Founder at Insurance Capital Markets Research (ICMR), Quentin Moore – Co-Founder at Insurance Capital Markets Research, Chris Sharp – Active Underwriter at Hampden Risk Partners (HRP), Ben Ormerod – Chief Data Officer, HRP