Overview

Reinsurance plays a vital role in the global risk transfer system by acting as a contingent form of capital. It absorbs volatility, supports underwriting capacity and can reduce the equity and debt capital insurers need to hold, improving weighted average cost of capital.

Despite this importance, reinsurance remains structurally illiquid, with most capital committed for annual contracts and little ability to adjust positions mid-term.

Howden Re’s report, A Secondary Market for Reinsurance, explores how this illiquidity creates financing friction and limits capital efficiency across the market.

Key Highlights

- Reinsurance supports underwriting capacity and can improve a firm’s WACC by acting as contingent capital.

- Structural illiquidity increases the effective cost of reinsurance by limiting mid-term portfolio adjustments.

- A secondary market could create real option value through flexible trading of exposures.

- The model draws on proven lessons from syndicated credit and loan markets.

The report argues that separating origination from ongoing ownership, as seen in mature credit markets, could transform reinsurance into a more dynamic and flexible asset class.

Secondary trading would allow participants to defer, expand, reduce or exit exposures as market conditions change, creating real option value and improving balance sheet management.

The proposed model would benefit cedents, reinsurers and retrocessionaires by enabling more active portfolio rebalancing and better alignment with underwriting views and internal capital models.

Supported by Brokerassist technology, this broker-led framework would preserve market relationships while improving transparency, pricing efficiency and capital deployment. Over time, a functioning secondary market could contribute to more efficient and potentially lower reinsurance pricing globally.

Reinsurance is a primary source of underwriting capital

Reinsurance is one of the primary sources of capital supporting global underwriting. By absorbing volatility, it can increase underwriting capacity and reduce required equity and debt capital thereby improving a firm’s weighted average cost of capital (WACC).

Yet despite its central role in the global risk transfer system, it remains structurally illiquid. Once placed, almost all reinsurance capital is held to maturity over annual contracts, with limited scope for adjustment.

By separating origination from ongoing ownership, as other mature capital markets have done, reinsurance could embed optionality into its contracts, improving capital efficiency and supporting more efficient pricing (see Global Reinsurance Pricing Softens at 1/1).

Why reinsurance matters in the capital structure

| Aspect | Explanation |

| Economic function | Acts as contingent capital |

| Effect on earnings | Reduces volatility by absorbing losses |

| Effect on investors | Lowers risk borne by equity and debt holders |

| WACC relevance | Can be analysed as a third contingent financing layer alongside debt and equity |

| Current friction | Lack of secondary market means capital must be committed ex ante |

| Cost implication | Irreversibility raises the effective cost of contingent capital |

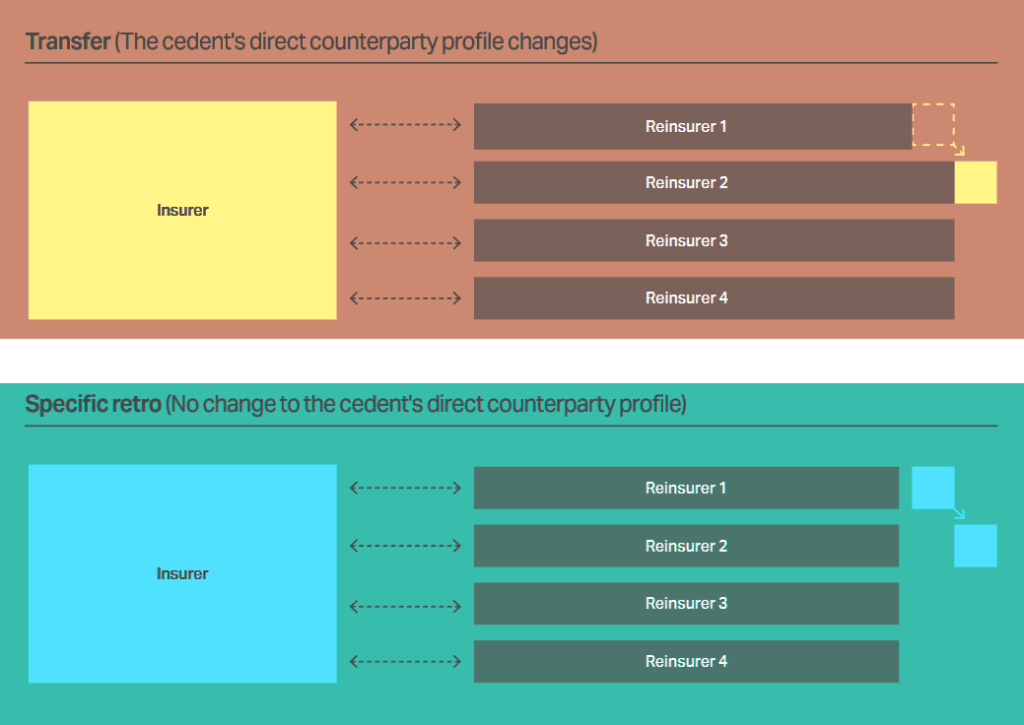

The reinsurance market, by contrast, does not generally possess this full facility. Primary risk is traditionally underwritten by insurance companies and distributed through reinsurance placements, while the secondary market consists largely of specialised, bilateral transactions between reinsurers, typically intermediated by brokers. These transactions are illiquid and specific to the underlying risk.

Reinsurance contracts involve the assumption of contingent liabilities and the potential payment of claims, such that the financial strength and counterparty profile of any buyer of risk is of material relevance to the ceding insurance company.

This feature complicates the transfer of insurance liabilities relative to more traditional financial assets, where secondary trading is more common (see Reinsurance Market Faces Post-Peak Pricing With Stable Sector Outlook).

A more open, liquid market for primary and secondary risk trading would bring important advantages to the reinsurance market by introducing optionality to the value chain, benefitting cedents, reinsurers, brokers and capital providers.

Illiquid vs secondary-traded reinsurance

| Dimension | Current hold-to-maturity market | Secondary-traded market |

| Liquidity | Very limited | Active post-placement trading |

| Position management | Little ability to rebalance mid-term | Ability to defer, expand, contract, or exit positions |

| Option value | Negligible | Material |

| Capital efficiency | Lower | Higher |

| Pricing | Reflects illiquidity and financing friction | More efficient pricing over time |

| Balance sheet use | Static | Dynamic |

This could, in turn, lower the cost of reinsurance while making reinsurance more economically profitable for underwriters. This brief considers how this might be realised and outlines the necessary operational mechanisms.

In credit markets, secondary trading transformed static exposures into dynamic balance-sheet assets. We see the same opportunity in reinsurance.

Rob Bredahl, Vice Chair, Howden Re and Chair, Howden Capital Markets & Advisory

A functioning secondary market would let participants actively manage risk through the cycle, releasing capital when returns compress and adding exposure when pricing improves.

Reinsurance within the capital structure

Reinsurance behaves as contingent capital. By absorbing losses, it reduces earnings volatility and lowers the risk borne by equity and debt holders. As the report demonstrates, it can be analysed as a component of a firm’s weighted average cost of capital, operating as a third contingent financing layer.

However, unlike debt or equity, reinsurance does not typically benefit from an active secondary market. Capital must be committed ex ante and priced to reflect the inability to rebalance exposures mid-term.

This irreversibility introduces an implicit financing friction and increases the effective cost of contingent capital.

Reinsurance real options value

| Option | Meaning in reinsurance context | Economic value in liquid market |

| Defer | Delay adding exposure until conditions are clearer | Improves timing of capital deployment |

| Expand | Increase participation when pricing improves | Captures attractive returns |

| Contract | Reduce exposure when returns compress or risk rises | Preserves capital and reduces downside |

| Exit | Sell down a position before maturity | Releases capital and improves flexibility |

Introducing secondary trading alters this dynamic

Drawing on a real options framework, the report explains that the ability to defer, expand, contract or exit a position as uncertainty resolves, has measurable economic value. In a hold to maturity market that option value is negligible. In a liquid market, it becomes material.

When reinsurance is treated as a third form of capital, the case for liquidity becomes obvious. Secondary trading turns static, hold-to-maturity contracts into flexible instruments with real option value.

David Flandro, Head of Industry Analysis & Strategic Advisory

This, in turn, lowers the cost of capital for cedents while allowing reinsurers to allocate balance sheet capacity far more efficiently.

Reinsurers can find value in a secondary market through being, in effect, released from full-year exposures, where an acceptable price exists for trading part of their position.

In doing so, reinsurers may rebalance their portfolios following unexpected original placement allocations, release collateral ahead of the timeframe permitted under the original treaty terms, or express a pricing view that differs from prevailing market levels.

Ideally, transactions would occur on existing contractual terms so that reinsurers would be able to adjust their exposure with minimal basis risk.

Lessons from mature capital markets

The report draws parallels with the development of the unfunded loan and syndicated credit markets. In those initially illiquid markets, underwriting and distribution became distinct functions as secondary trading infrastructure developed.

Reinsurance today resembles an earlier stage of that evolution. Syndication exists, broker intermediation is central and counterparties are pre-approved.

What is missing is the infrastructure required to support efficient post placement trading. The logical progression, the report argues, is to build liquidity on top of the broker led ecosystem rather than in place of it.

Lessons from mature capital markets

| Mature market example | What changed there | Relevance to reinsurance |

| Unfunded loan markets | Underwriting and distribution became distinct functions | Reinsurance could follow same path |

| Syndicated credit markets | Secondary trading infrastructure created liquidity | Suggests similar infrastructure can unlock efficiency |

| Common feature | Static exposures became tradeable balance-sheet assets | Reinsurance contracts could become more flexible instruments |

| Industry implication | Distribution and ownership no longer need to remain bundled | Supports separating origination from ongoing ownership |

An all reinsurance market solution

A successful secondary liquidity pool must deliver value to cedents, reinsurers and retrocessionaires alike.

Because reinsurers rarely achieve optimal portfolio composition at renewal, secondary trading would allow exposures to be rebalanced in line with internal capital models and evolving underwriting views.

Cedents could trade risk off existing treaties during the coverage period rather than relying solely on incremental retrocession or direct and facultative (D&F) purchases.

Secondary trading structures

Following seasonal events, collateralised retrocessionaires could reduce exposure and release collateral for tactical investing.

Traditional reinsurers could increase participations selectively where marginal profitability is attractive.

Over time, greater liquidity should support more efficient capital deployment and, consistent with corporate finance theory, lead to more efficient and ultimately lower pricing.

What reinsurance already has vs what is missing

| Already present | Missing |

| Syndication | Efficient post-placement trading infrastructure |

| Broker intermediation | Structured secondary liquidity mechanisms |

| Pre-approved counterparties | Trading processes to support rebalancing |

| Existing governance and credit structures | Operational tools for dynamic allocation |

Because reinsurers rarely achieve their optimal portfolio composition at renewals, a secondary market would enable them to rebalance portfolios post transaction in line with internal capital models, underwriting ambitions and their own view of risk.

Cedents could likewise ‘trade risk off’ existing treaties rather than purchasing additional retrocession or direct and facultative (D&F) cover following renewal.

During the coverage period, cedents and reinsurers, or reinsurers and retrocessionaires, would be able to trade risk on and off in-cycle to better meet their respective objectives.

Stakeholder benefits from a secondary market

| Stakeholder | Potential benefit |

| Cedents | Can trade risk off existing treaties during coverage period |

| Reinsurers | Can rebalance exposures according to internal capital models and underwriting views |

| Retrocessionaires | Can reduce exposure after seasonal events and release collateral |

| Traditional reinsurers | Can selectively add participations where marginal profitability is attractive |

| Market overall | More efficient capital deployment and potentially lower pricing over time |

A deliberate evolution

The barriers to a secondary market are practical rather than conceptual. Introducing liquidity requires a deliberate, broker-led approach that aligns with the industry’s governance, credit and relationship structures.

If successfully implemented, a secondary market would enable carriers to allocate risk more dynamically, improve capital utilisation to support more efficient and ultimately, lower pricing.

Over time, this evolution would expand reinsurance’s role as a supplier of contingent capital while remaining consistent with the characteristics that underpin its stability and resilience.

FAQ

It is a structured market where existing reinsurance exposures can be traded after placement, allowing participants to adjust risk positions during the contract term

Because it absorbs losses and reduces earnings volatility, lowering the risk carried by equity and debt holders within an insurer’s capital structure

Most reinsurance contracts are placed annually and held to maturity, with limited opportunity to rebalance or exit positions once they are written.

It would allow firms to reallocate capacity as pricing, risk and market conditions change, reducing financing friction and improving use of balance sheet capital.

Cedents gain flexibility to manage treaty risk during the coverage period, while reinsurers can rebalance portfolios and deploy capital where returns are stronger.

Yes. Greater liquidity and more efficient capital allocation could support better pricing efficiency and ultimately contribute to lower costs across the market.

………………….

AUTHORS: Rob Bredahl – Vice Chair, Howden Re and Chair, Howden Capital Markets & Advisory, David Flandro – Head of Industry Analysis & Strategic Advisory

Edited by Oleg Parashchak – Editor-in-Chief, Beinsure, Yana Keller – Lead Re/Insurance Editor, Beinsure