Overview

Reinsurance buyers generally experienced a more competitive reinsurance market at the July 1 renewal compared to recent years, with capacity available even where demand increased, and reinsurers looking to grow, according to Gallagher Re’s 1st View mid-year renewal report.

Insurers were largely able to secure risk-adjusted rate reductions for property treaties and were well-placed to hold pricing broadly flat in casualty lines – in part, as underlying pricing increases continue to flow through to reinsurers.

With these conditions in place, clients had the opportunity to challenge the status quo, and secure improvements to the structure and terms of their property and specialty reinsurance programs, according to Global Reinsurance Market Report.

Key Highlights of Reinsurance Renewals Report

- Reinsurers entered the renewal with strong capital, disciplined strategies, and willingness to grow, resulting in ample capacity, competitive pricing, and improved terms for buyers across property, casualty, and specialty lines.

- Property treaties achieved average risk-adjusted rate reductions of 10–15%, alongside enhancements in attachment points, terms, and conditions. Florida benefited from returning capacity driven by legislative reforms that reduced litigation and improved claims predictability.

- Casualty lines saw stable rates and flat or slightly lower ceding commissions, with better outcomes for cedants demonstrating measurable improvements in underwriting, claims management, and risk selection.

- Cyber reinsurance continued to favor buyers due to oversupply and growing APAC demand. Aviation focused on clarifying losses from recent aircraft incidents, while marine, mortgage, credit/surety, and political violence maintained strong capacity and competitive terms.

- Total reinsurance capital reached $769 bn by year-end 2024, bolstered by retained earnings and ILS inflows. Reinsurers remain innovative, exploring non-traditional vehicles and optimized structures, with the market expected to remain favorable barring unforeseen catastrophic events.

Gallagher Re issues the publication for reinsurers at the key reinsurance renewal seasons — 1 January, 1 April, 1 July — to deliver the very first view on current market conditions in the reinsurance industry, Beinsure noted.

Reinsurers came into the renewal in good financial shape

They reported strong results for 2024, with ROEs well above the cost of capital.

Q1 results were weaker due to the impact of January’s unprecedented wildfires in Los Angeles, California, but barring further exceptional cat events, reinsurers remain on track for another good year overall, total reinsurance dedicated capital hit a new peak of $769 bn at the year-end 2024.

As noted in Gallagher Re’s Reinsurance Market Report in April, reinsurers are currently on track to deliver healthy ROEs in the mid-teens for 2025, with traditional reinsurance capital set to increase by another 6% (assuming average results for the rest of the year).

- $769 bn — Total reinsurance dedicated capital at year-end 2024, reaching a new peak.

- 10–15% — Average risk-adjusted rate reductions achieved on property reinsurance at July 1, 2025 renewals.

- $56 bn — Global insured catastrophe losses in Q1 2025, driven largely by the Los Angeles wildfires.

- $15.2 bn — H1 2025 cat bond issuance through June 13, up 36% year-on-year.

- $4 bn — Growth in non-life ILS assets under management in Q1 2025, supporting additional capital supply.

The increase in reinsurance dedicated capital

The increase in reinsurance dedicated capital has been driven mainly by retained earnings at the traditional reinsurance groups, rather than new entrants or capital raises.

But capital supply has also been supported by further inflows into the ILS market, with $4 bn of non-life ILS AUM growth in Q1 supporting $15.2 bn in H1 cat bond issuance through June 13, up 36% year-on-year, Beinsure noted.

Global reinsurers are also collaborating with insurers to utilize non-traditional capital vehicles, such as sidecars, where interest in accessing insurance risk remains robust.

Whether or how broader macroeconomic conditions impact the (re)insurance industry through 2025 and beyond was a topic of discussion in mid-year renewal negotiations.

To support appropriate outcomes relative to this uncertainty, cedants were largely successful in articulating their approach to fluctuating conditions within their underwriting, mitigating the need for additional adjustments.

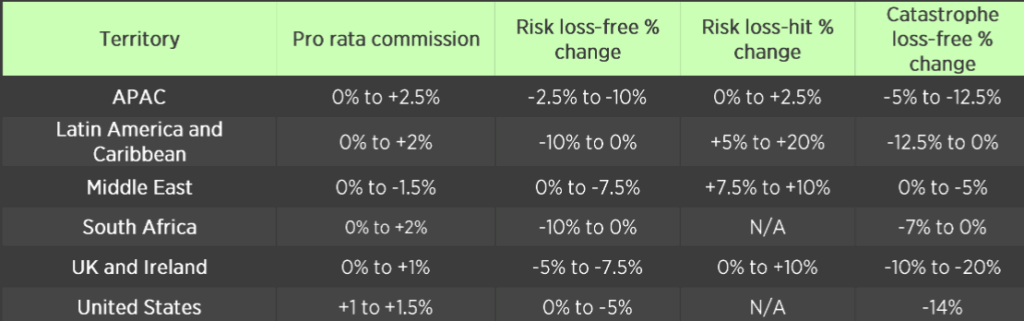

Property reinsurance and property cat losses

After several years in which the share of incurred property cat losses has skewed to primary insurers, market conditions were favorable to better address buyer needs at this renewal.

Reinsurers were looking to balance their appetite for growth with their objective of orotecting profitability. The result was risk-adjusted rate reductions around 10-15% on average.

While this reflects the broader outcome, individual renewals remained highly dependent on their own characteristics, continuing the trend of more diverse results at a granular level.

This calculation also reflects structural adjustments such as shifts in attachment points, and where quantifiable, improvements in terms and conditions.

Property reinsurance rate movements

Florida renewals are a particular focus at mid-year

This market had seen an exodus of (re)insurance capacity in the past few years, which created a highly challenged operating environment and exacerbated already-difficult conditions for buyers, Beinsure noted.

2025 saw a return of capacity to the state, driven by legislative changes that reinsurers can reliably anchor to.

In order to best position our Florida clients, we have worked with them to assemble market-wide evidence that legislative changes have proved successful in reducing insurance-related litigation, with Hurricane Milton in late 2024 having provided a real-world ‘test case’.

We will be sharing greater insight into this analysis in a subsequent publication, providing ongoing insight for the positive impact of the reforms.

Reinsurance brokers also continue to support clients on organic growth initiatives, as well as depopulation efforts from Citizens, the state-backed ‘insurer of last resort’, as, greater ability to implement evolving business strategies is bolstered by increasing reinsurer support.

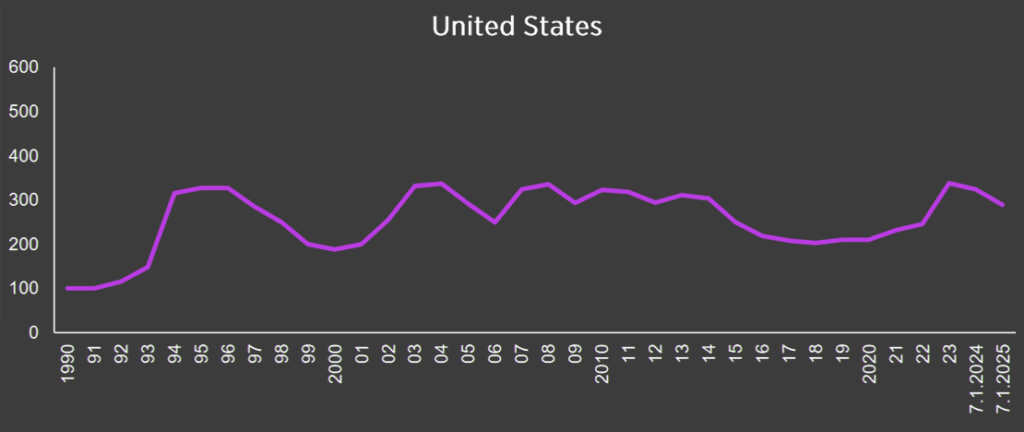

Property cat market and P&C insurance losses

In the broader property cat market, global insured losses in Q1 2025 were notably elevated at $56 bn.

January’s unprecedented wildfires in Los Angeles, California were a major driver and have continued to be a topic of discussion through the renewal, though did not materially impact pricing or appetite.

SCS frequency has also remained elevated in areas of the US, compared to the 10-year average, but severity has been lower than in 2023 and 2024.

Overall, losses have proved manageable so far in 2025, and outside particular loss-hit portfolios, had limited impact on renewal outcomes.

Property catastrophe reinsurance pricing trend

That said, cedants remain keen to cap their maximum exposure to high frequency events, and we have been working with them to bolster the availability of solutions such as aggregate covers that better address buyers’ needs.

With no shortage of capacity, reinsurers are seeking ways to differentiate themselves and are showing increased willingness to consider re-entering and innovating in this space.

For the moment, they remain most receptive to structures that require a peak zone loss to trigger coverage, rather than a larger number of secondary peril losses.

Property reinsurance market saw more muted rate reductions

The property per risk market, meanwhile, saw more muted rate reductions, often in single digits.

Reinsurers were less willing to lean into the risk market, reflecting historically lower margins. Client differentiation remains key, and those cedants able to show they have devoted time and attention to optimizing their per risk programs have seen meaningfully improved outcomes.

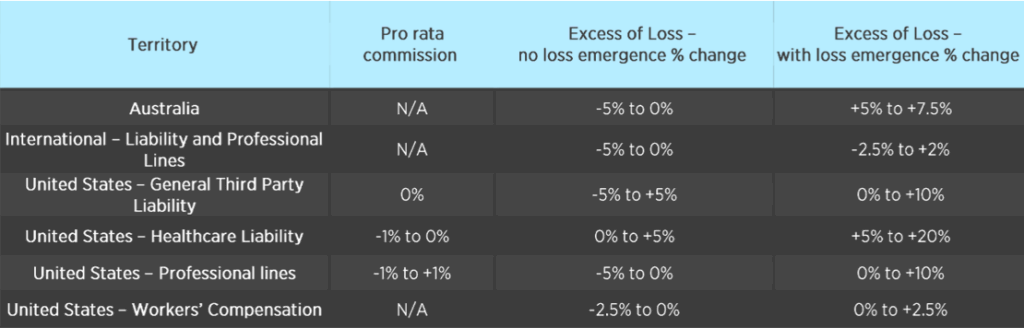

Casualty reinsurance and loss development

In casualty lines, concerns persist over prior-year loss development as well as loss trends from inflation and the litigation environment.

US P&C insurers reported a collective $8.1 bn of adverse prior-year development in calendar year 2024 relating to the trailing 10 accident years, up from $3.8 bn in 2023.

On the flip side, many carriers continue to take proactive steps through their underwriting strategies and claims management practices to mitigate the impact of loss trends and improve outlook on profitability.

This was reflected in outcomes at the July 1 renewal, with ceding commissions largely flat or fractionally down on quota-share business, and rates broadly stable in excess of loss.

Casualty reinsurance rate movements

Reinsurers showed greater confidence

Reinsurers showed greater confidence in those cedants who articulated the actions they have taken to improve performance, and how their actions tangibly improve future performance.

Yet there was a clear market divide. For cedants unable to provide evidence on how they are tackling the performance issues, outcomes were less favorable.

That puts a premium on not only articulating, but also crucially quantifying, the impact of these strategic improvements.

Gallagher Re has been working closely with our clients to evidence the impact of these shifts, from overhauling claims practices, to changes in business mix by geography or industry.

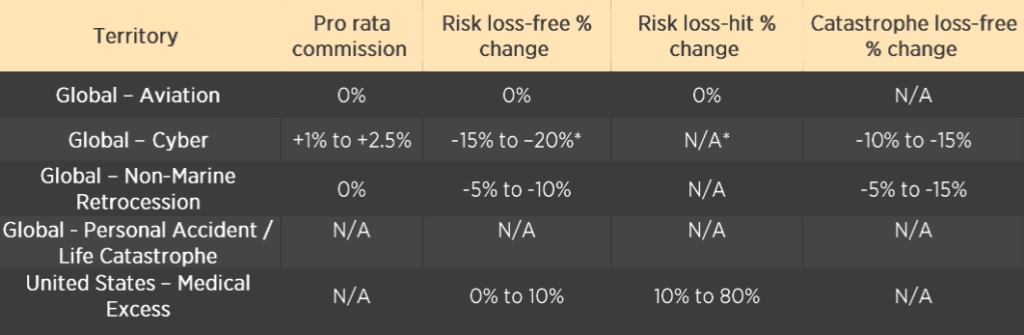

Specialty reinsurance and oversupply of capacity

In specialty lines, which cover aviation, cyber, marine & energy, mortgage, credit/surety, and political violence & terror, several dynamics applied.

Notably, in cyber, we saw a general continuation of the same trends seen at 1.1.25, leading to risk-adjusted rate improvements in favor of reinsurance buyers and retro purchasers.

This was expected in a market with an oversupply of capacity and a slowdown in organic growth. But there was growing demand, and supply, of turnkey solutions for international cyber, especially in the APAC region.

Specialty reinsurance rate movements

In aviation, (re)insurers are likely to have to wait for some time to determine the impact of the recent, tragic loss of Air India flight AII71 in Ahmedabad, as air accident investigators do their vital work.

But the market has also recently gained some long-awaited clarity on losses related to 147 aircraft trapped in Russia, with a judgement from London’s High Court early in June that contingent hull war risks coverage will apply.

We are now heavily engaged with certain clients and their reinsurers, working to deliver optimal claims recovery outcomes, but we do not expect this to be a situation where the recovery floodgates suddenly open.

Instead, carefully considered conversations can now begin.

Outlook for global reinsurance market

2025’s renewals are showing a consistent trend: a growing market in which the balance of supply and demand has tilted back toward reinsurance buyers. The scale of the changes we have seen in underlying pricing and underwriting actions in recent years cannot be overstated, Beinsure noted.

North American casualty has experienced five consecutive years of substantial compound rate increases, accompanied by additional loss mitigation measures aimed at addressing persistent challenges in the segment.

After several highly profitable years, reinsurers are actively seeking opportunities to deploy their significant capital. However, their approach remains disciplined.

In certain businesses and regions, some reinsurers — particularly larger and less growth-oriented players — continue to prioritize profitability over market share and are prepared to cede share to maintain margins.

Reinsurers are showing greater flexibility

In the property market, reinsurers are showing greater flexibility on aggregates and per-risk terms, which is a positive development.

However, substantial work remains in refining the details and presenting a compelling case supported by robust data and analysis.

Insurers operating in U.S. casualty should expect continued, close scrutiny of their underwriting practices.

This is a highly segmented market where data transparency and clear evidence of underwriting discipline are critical to securing favorable terms.

3rd quarter, which includes the most active period of the North Atlantic hurricane season, will be particularly significant for industry financial results this year, especially following the wildfire losses in California during the first quarter.

Forecasts continue to anticipate an “above average” hurricane season, though slightly less intense than 2024.

At the April renewal, it was noted that absent major unforeseen events during the remainder of 2025, reinsurers would likely maintain their differentiated approach to risk-adjusted rate reductions.

So far, market behavior has supported this expectation. Cedants and brokers currently have room to maneuver while reinsurers explore innovative solutions.

The focus is extending beyond rates to broader optimization of reinsurance placements, with parties seeking more effective and balanced arrangements.

FAQ

Reinsurers entered the renewal with strong 2024 results, high levels of dedicated capital, and a desire to grow portfolios. Buyers benefited from abundant capacity, with reinsurers competing to maintain or expand market share. The legislative improvements in key markets like Florida and manageable catastrophe losses further supported a more favorable environment for cedants.

Property reinsurance achieved average risk-adjusted rate reductions between 10–15%. Improvements extended beyond pricing to include adjustments in attachment points, elimination of unfavorable terms, and better conditions on aggregate and per-risk structures. Individual renewal outcomes remained highly dependent on program characteristics, loss history, and evidence of underwriting discipline.

Reinsurers returned capacity to Florida after several years of retrenchment, encouraged by legislative reforms that reduced litigation and improved claims predictability. Buyers were able to use market-wide evidence of these reforms’ effectiveness — supported by the real-world impact of Hurricane Milton — to negotiate better structures, secure more favorable pricing, and attract additional capacity for organic growth and depopulation efforts from Citizens.

While Q1 2025 saw elevated global insured losses of $56 bn, particularly from the Los Angeles wildfires, these losses were largely manageable for the industry. Outside specific loss-affected portfolios, these events did not materially disrupt pricing or reduce appetite. Reinsurers continued to favor structures that protect against peak perils while remaining cautious about high-frequency secondary perils.

Casualty lines maintained broadly stable rates and commissions, particularly for cedants who demonstrated clear and quantifiable improvements in underwriting, claims management, and business mix. Conversely, those unable to present evidence of corrective actions faced less favorable terms. Reinsurers showed confidence in disciplined programs while continuing to monitor trends in litigation and prior-year development closely.

Specialty lines saw mixed dynamics. Cyber experienced rate improvements for buyers and growing demand for turnkey solutions, especially in APAC, as oversupply persisted. Aviation focused on assessing the impact of the Air India accident and clarifying recoveries related to aircraft stranded in Russia. Marine, mortgage, credit/surety, and political violence also benefited from strong capacity and competitive conditions.

Reinsurers remain disciplined yet increasingly innovative, with ample capital and a focus on optimizing placements. Buyers are in a stronger position to negotiate favorable structures and rates, provided they present robust data and clear strategies. The third quarter’s hurricane season remains a key factor to watch, but absent major unforeseen events, the market is expected to maintain its balanced and competitive posture through year-end.

……………..

AUTHORS: James Vickers – Chairman Gallagher Re International, Michael van Wegen – Head of Client & Market Insights, International, Global Strategic Advisory

Edited by Yana Keller — Editor at Beinsure Media