Overview

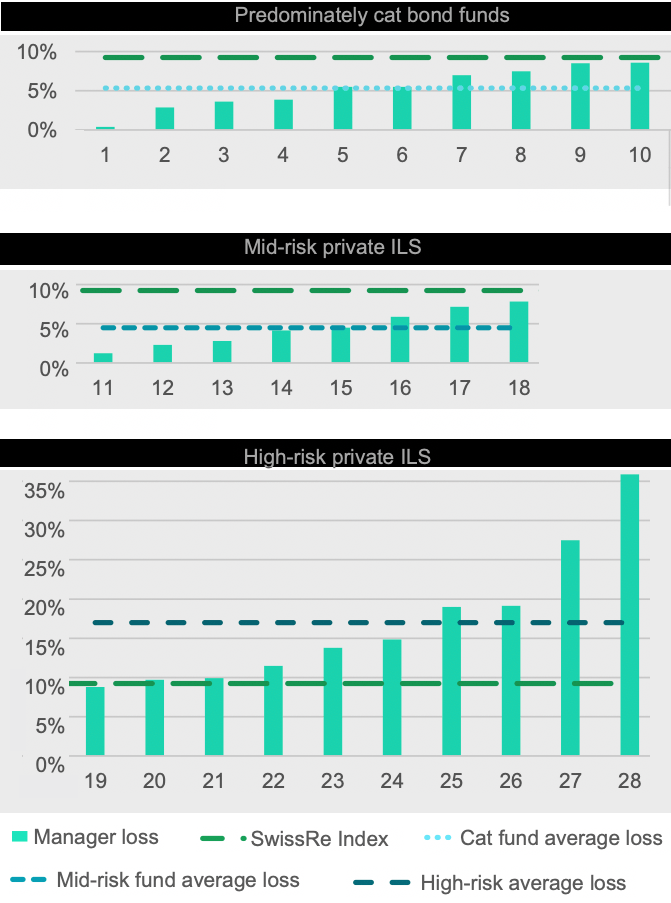

Higher-risk focused insurance-linked securities (ILS) fund strategies appear to be averaging losses around the 17% mark after hurricane Ian.

According to Frontier Advisors, there is a particularly wide dispersion of losses, as indicated by disclosures seen to date and side-pockets set, with a range of 3% to around 30% seen by Artemis.

Dispersion of losses from hurricane Ian

Wide range, but also shows some interesting detail on the dispersion of losses from hurricane Ian, across a range of catastrophe bond funds and funds that invest in private ILS and collateralised reinsurance or retroccession contracts (see Reinsurance Rates for Property Catastrophe).

Frontier Advisors shows the dispersion of reported hurricane Ian losses, across catastrophe bond funds, mid-risk private ILS funds and high-risk private ILS fund strategies (see how Investors in Insurance-Linked Securities (ILS) Are Seeking Innovation).

The average loss reported across catastrophe bond funds is actually slightly higher than the average across mid-risk private ILS fund strategies.

This is due to the level of the initial mark-to-market hit to catastrophe bonds after hurricane Ian, which has reduced as loss estimates have come out lower than anticipated from cat bond sponsors in a number of cases.

Manager estimated ILS product loss impact from Hurricane Ian

With mid-risk funds tending to hold less concentrated exposures to Florida and a greater level of peril and geographic diversification.

For the mid-risk ILS fund cohort, in some cases it is structure and strategy that has mattered and helped them deliver a better result after Ian than might have happened after smaller hurricanes in previous years.

The way some ILS fund managers have addressed their portfolio construction, terms and conditions, as well as fronting and arrangements to mitigate trapped capital, have all been seen to have a positive effect in 2025.

This is providing some confidence to longer-term investors in the ILS space, as seeing strategies better weathering an industry loss of the magnitude of hurricane Ian is seen as positive for some ILS managers.

Meanwhile, the higher-risk side of the ILS fund market shows a different picture, with some significant losses being reported.

The higher-risk ILS fund average loss from hurricane Ian, from those funds to be around the 17% mark, with two of the strategies reporting initial loss estimates above 25%.

Global insurance-linked securities market remains bogged with prior catastrophe losses as the overall performance of funds deteriorates, despite another year of record cat bond issuance.

According to AM Best, issuance in the 144a cat bond market reached a record of approximately $12.5bn exceeding the previous record set by $1.5bn.

Despite the generally higher returns cat bonds offer, US insurers hold only about $850m of the roughly $33bn outstanding cat bonds.

According to Global Insurance-Linked Securities Market Outlook, only about 40 insurers have exposures to cat bonds and five companies account for nearly 70% of investments.

Swiss Re’s US entities hold more than 20% of the industry’s investments, across a variety of risks and cedents, with the majority of the other investors being life insurers.

Hurricane Ian cat bond loss estimates significantly lower than expected

Plenum Investments has slashed hurricane Ian loss expectations for its catastrophe bond investment funds, saying that initial estimates from sponsors are coming in “significantly lower than our original expectations”, leading it to believe the draw-down could be less than half the initial estimates.

Realised catastrophe bond losses from hurricane Ian could ultimately prove to be as little as half the initial, and still current at that time, mark-to-market decline in the outstanding cat bond market.

With the latest signal being a range of early hurricane Ian loss estimates from catastrophe bond sponsors that suggest their bonds are either set to be free from loss, or face much lower losses than had originally been anticipated.

Hurricane Ian loss projection

The latest example of this comes in FEMA’s initial hurricane Ian loss projection for the NFIP, the upper-end of which is just below where its FloodSmart Re cat bonds would attach.

Specialist cat bond and reinsurance focused investment manager Plenum has said that other estimates are also coming in lower than anticipated, which confirms what we’ve been hearing this week from a few other sources.

Given the newly available loss estimate data direct from sponsors, Plenum has revisited its earlier estimates of losses its cat bond investment funds might suffer after hurricane Ian and slashed those declines by more than half, with an expectation of a 2% maximum hit to the flagship Plenum CAT Bond Fund, 3% maximum hit to the Plenum CAT Bond Dynamic Fund, and 1% maximum hit to the Plenum Insurance Capital Fund.

FEMA’s announcement of its initial estimate for flood insurance losses due to hurricane Ian will be one driver given that came out late yesterday and likely saw a loss estimate delivered to cat bond investors at the same time.

Despite the growth in the non-catastrophe ILS market and heightened interest in these types of transactions, (specifically those involving the transfer of casualty and liability insurance risks) US insurers’ investments in these asset classes are minimal at this point, aside from the financial guarantee and mortgage insurance risks.

………………………

AUTHORS: Artemis by Frontier Advisors and Plenum Investments Data