Overview

European reinsurers recorded stronger return on equity (ROE) in 2024 and 2025, exceeding their cost of equity in three of the last four years, according to Goldman Sachs.

Between 2017 and 2022, the sector only met or exceeded this benchmark in two years. ROE lagged materially behind in 2017, 2018, 2020, and 2022.

Key pressures included large losses from hurricanes such as Irma, Harvey, and Maria in 2017, and Ian in 2022. But systemic issues also played a role, Beinsure noted.

5 Key Highlights

- European reinsurers exceeded cost of equity in 2023 and 2024, driven by underwriting gains and reserve actions.

- Reinsurers used strong results to build buffers. Swiss Re added $3.1bn in US liability reserves; Hannover Re grew its reserve to €2bn.

- The average P&C combined ratio fell to a record 86.3%, reflecting benign large-loss activity and disciplined underwriting.

- European reinsurers held a 36% global share, supported by local presence and diversified portfolios across geography and business lines.

- After mixed January renewals, property catastrophe reinsurance pricing is expected to stabilise at mid-year renewals, despite pressure from wildfire and hurricane losses.

These included increased catastrophe losses excluding major events, higher secondary peril costs, US social inflation affecting casualty books, and rising capital levels through 2021.

Although reinsurance rates began increasing in 2017, they remained below loss cost trends for several years. Hurricane Ian in 2022 marked a turning point.

Rates rose sharply, coinciding with higher interest rates and a reduction in industry capital. Carriers responded by adjusting attachment points and reducing proportional business, which lowered exposure to frequent losses and improved combined ratios.

January reinsurance renewal premiums increased by 4.5%, primarily driven by volume. Reinsurers experienced stable reinsurance renewals at 1.1 due to greater prudence and selective focus in underwriting.

Premium growth in 2024 was driven more by volume than rate, as rising exposure—particularly in property—pushed up demand for reinsurance. Natural catastrophe pricing declined slightly, while casualty pricing remained stable or increased. This was due to a cautious inflation outlook and updated loss models.

European reinsurers maintain market share

European reinsurers retained a 36% share of the global reinsurance market, according to AM Best. Premiums grew from $53.5 bn to $122.1 bn, reflecting 4.2% annual growth. This stability came without a shift toward wholesale markets. Instead, reinsurers focused on retail networks and in-country presence.

As national markets attempt to retain more premium, local engagement has been a key advantage. However, this strategy has increased operating costs and added regulatory complexity due to compliance with multiple national regimes.

To sustain growth, European reinsurers are pursuing innovation tied to public-private collaboration and large-scale risk cover. Focus areas include social, geopolitical, and climate-related perils such as earthquakes and floods. The industry has also worked to highlight protection gaps, especially for natural catastrophes, Beinsure noted.

European reinsurers have maintained financial strength for over 15 years, with no failures or stress events over that period.

The current strategy builds on this position, using diversification by geography and business lines, including life reinsurance, to reduce concentration risk.

This diversification approach has yielded better outcomes than past efforts, which often pursued expansion at the cost of profitability.

The structured and transparent regulatory framework in Europe supports this more measured growth path.

To continue playing a stabilising role during systemic shocks, reinsurers must remain engaged in a broader European dialogue addressing technical, social, and political risk. Regulators must also uphold policies that support prudent risk-taking on both sides of the balance sheet.

Reinsurers used the hard market to strengthen reserves

Accordin to Fitch, Munich Re, Swiss Re, Hannover Re and SCOR – reported very strong average return on equity of 13.7% in 2024, albeit slightly down from 17.1% in 2023.

Sustained underwriting results and investment income made 2024 the second consecutive year of very strong property and casualty (P&C) financial performance in a prolonged favourable market.

Swiss Re added $3.1bn to US liability reserves. Scor raised its P&C Re reserves by over €300mn in 2024. Hannover Re increased its resiliency reserve to around €2bn. Munich Re added €0.9bn in 4Q23 and made further reserve additions in 4Q24.

These moves contributed to stronger ROE in 2023 and 2024, despite persistent industry losses and reserve strengthening. Scor was an exception, as reserving on its L&H Re book kept its ROE below target levels in 2024, Beinsure noted.

January 2026 renewals showed a 0–2% drop in risk-adjusted pricing—the first decline since 2017. This reflected solid reinsurer results, frequency losses absorbed by primary carriers, and stronger capital supply.

Hannover Re reported a 2.1% rate decline, while Scor saw flat pricing driven by retro market conditions.

SCOR was an outlier, with its results tarnished by the losses from adverse changes in its life and health (L&H) reserving assumptions. Very strong performance, coupled with very strong capital adequacy and bolstered reserves buffers, have consolidated the reinsurers’ credit strength.

P&C reinsurance combined ratio improved

This has positioned the peers to meet their ambitious targets for 2025 in what may be a less supportive reinsurance market environment, amid heightened macroeconomic and geopolitical uncertainties.

The peer group’s average reported P&C reinsurance combined ratio improved to a record 86.3%. This was a 1.0pp improvement from the previous year, driven by sustained pricing level and a benign large loss experience.

All reinsurers exceeded guidance, except for Swiss Re, whose combined ratio deteriorated due to substantial prior-year US liability reserve additions.

Property catastrophe reinsurance pricing to stabilize at US-focused renewal rounds, according to Beinsure report.

After a mixed pricing environment at the January 1, 2025, reinsurance renewals, Moody’s analysts expect property catastrophe reinsurance pricing to stabilize at the mid-year US-focused renewal rounds.

The impact of Hurricanes Helene and Milton, along with costly California wildfires, is expected to influence pricing.

Moody’s highlighted that largest European reinsurers and reinsurance brokers shared insights on their January 1 renewals, when 40% to 60% of a global reinsurer’s portfolio is typically renewed, including much of the European reinsurance business, Beinsure noted.

Among the four largest European reinsurers, all except Munich Re recorded premium growth at the January renewals.

The four reinsurers took advantage of strong P&C underwriting results to strengthen specific claims reserves as well as build up general prudence in reserves, which is positive for our assessment of reserves adequacy.

P&C margin cycle may have peaked

Analysts noted the P&C margin cycle may have peaked, though California wildfire losses could influence mid-year renewals.

Overall, the sector’s repositioning has supported improved returns and better alignment between ROE and cost of equity.

Global reinsurers have tightened their terms and conditions to limit their aggregate covers and the lower layers of their natural catastrophe protection, largely in response to increasingly frequent and volatile weather-related losses due to climate change.

European reinsurers have become more exposed to weather-related losses due to reinsurers providing less cover against medium-sized natural catastrophe risks

This leaves insurers much less protected against secondary peril events. In addition, higher reinsurance prices have led some insurers to buy less cover.

Reinsurers achieved stronger investment yields

Largest global reinsurance groups are cutting back on the cover they provide against medium-sized natural catastrophe risks due to investor pressure after several years of large catastrophe losses and improved profitability in other parts of the market.

Reinsurers achieved stronger investment yields due to higher interest rates and favourable financial market conditions, contributing to their increased earnings.

Although they paid dividends and, in some cases, bought back shares, Moodey’s emphasises that their risk profiles are largely unchanged, reflecting the group’s stable appetite for underwriting and investment risk.

Most of the four reinsurers have committed to progressive dividend policies, which limit their flexibility to reduce shareholder payouts.

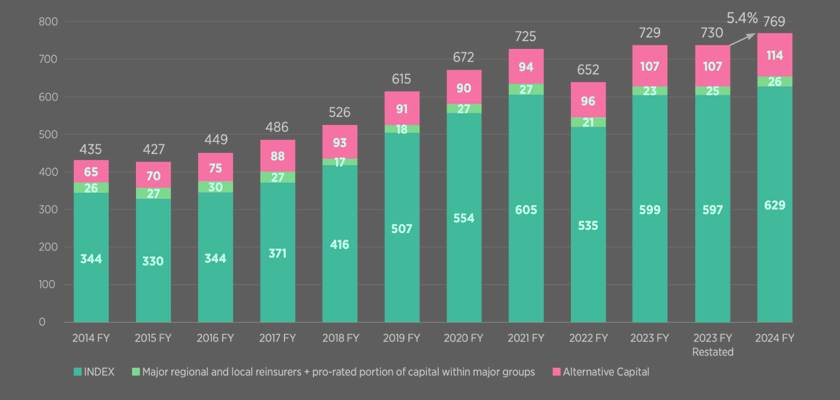

Total dedicated reinsurance capital

Total dedicated reinsurance capital rose by 5.4% in 2024, reaching a record $769bn, according to Gallagher Re. The increase came from both traditional and alternative capital sources.

Gallagher Re’s year-end report noted strong retained earnings as the main driver of capital growth, reflecting another profitable year for reinsurers. Capital increased from $730bn in 2023 to $769bn in 2024.

INDEX companies, which hold over 80% of total industry capital, saw a 5.3% rise to $629bn. This was supported by $117bn in net income. Capital return of $58bn and unrealised investment losses of $23bn partially offset the gains, Beinsure noted.

Non-life alternative reinsurance capital grew by 6.6% year-on-year to $114bn. The rise was driven by strong investor demand and a record year for catastrophe bond issuance.

FAQ

Higher underwriting profits, reserve strengthening, and investment gains from rising interest rates contributed to improved ROE. Most carriers exceeded their cost of equity for three of the last four years.

Large catastrophe losses, notably from hurricanes Irma, Harvey, Maria, and Ian, along with weaker pricing relative to loss trends and high secondary peril costs, suppressed returns during this period.

Carriers adjusted attachment points, reduced proportional business, and tightened terms. These changes reduced exposure to frequent losses and helped improve combined ratios.

Volume growth, not rate increases, accounted for most of the premium expansion. Higher exposure in property and stabilised or rising casualty pricing supported this trend.

Key reinsurers—Swiss Re, SCOR, Hannover Re, and Munich Re—added to reserves in 2023–2024 to strengthen balance sheets. This improved financial resilience and reserve adequacy.

Yes. January 2025 renewals saw a 0–2% drop in risk-adjusted pricing for the first time since 2017, due to strong reinsurer results and abundant capital.

Rising secondary peril exposure, potential mid-year pricing pressure, and limited coverage for medium-sized catastrophes. Maintaining discipline and reserve adequacy will be key in a less favourable market.