Overview

- U.S. P&C insurers have had to contend with rising loss costs

- U.S. personal lines insurers were met with multiple challenges

- Best US Property & Casualty Insurers in 2025 by admitted assets

- Best US Property & Casualty Insurers in 2025 by net premiums

- Best US Property & Casualty Insurers in 2025 by gross premiums

- Best US Property & Casualty Insurers in 2025 by policyholders’ surplus

- Property & Casualty Insurance Lines of Business

- Personal Insurance Lines of Business

The U.S. Property & casualty insurance market faces rising loss costs, driven by inflation, severe weather events, and litigation trends. Personal lines insurers experienced significant underwriting losses in 2024, primarily due to secondary perils like storms and wildfires, while commercial lines achieved profits through rate increases and advanced risk selection. Regulatory variations and inflation continue to influence rate approvals and claims costs, particularly in personal auto and homeowners insurance, according to AM Best‘s January Review. Beinsure has highlighted the key insights from the Best’s report.

In the United States, Property & casualty insurers file a special statement with the National Association of Insurance Commissioners. The filing is designed to determine premiums and losses by lines of business and to give an accurate view of the insurer’s reserving for loss.

AM Best’s database contained filing statements for 2,634 total single companies operating in the U.S. Property & casualty insurance market. According to the U.S. Department of Labor’s December 2024 jobs report, approximately 592,500 people work in the Property & casualty industry.

Key Highlights

- Rising Loss Costs and Secondary Perils: U.S. Property & casualty insurers face higher loss costs driven by inflation, social inflation, litigation financing, and increased frequency of secondary peril events, such as severe convective storms and wildfires.

- Segment Performance in 2024: Commercial lines recorded a $10 bn net underwriting profit, while personal lines faced a $33 bn loss due to severe weather-related events and rising repair costs.

- Top U.S. P&C Insurers: State Farm Group, Berkshire Hathaway Ins, and Progressive Ins Group rank among the largest U.S. Property & casualty insurers by net and gross premiums, admitted assets, and policyholders’ surplus.

- Impact of Inflation and Regulations: Inflation and regulatory constraints have significantly influenced rate increases across personal auto and homeowners insurance, with state approvals varying widely.

- Technological Investments in Commercial Lines: Commercial insurers are investing in predictive analytics, telematics, AI, and big data to improve risk segmentation, real-time pricing, and operational efficiency.

Property insurance covers damages or loss of property. As a result, rates can be significantly higher in areas susceptible to perils such as hurricanes. Casualty insurance covers indemnity losses and legal expenses from losses such as bodily injury or damage that the policyholder may cause to others.

U.S. P&C insurers have had to contend with rising loss costs

U.S. property and casualty insurers have had to contend with rising loss costs, above-average catastrophe activity, adverse trends in personal auto, more frequent (nonpeak) peril loss events, social inflation and litigation financing, and regulatory constraints, according to a Best’s Report.

- Commercial lines insurers achieved a net underwriting profit of more than $10 bn, as they continued to reap the benefits of rate increases and effective risk selection.

- The personal lines segment recorded a net underwriting loss of nearly $33 bn, primarily related to the frequency and severity of weather-related secondary peril events.

- Insured losses from these weather events continue to take a toll on P&C insurers and to trend above the long-term averages, as the frequency and intensity levels of storms worsen.

In 2023, the United States experienced more bn-dollar catastrophe events than in any other year on record, and activity has remained elevated throughout 2024, according to a Best’s Market Segment Report.

In addition to Hurricanes Milton, Helene, Debby, and Beryl, U.S. losses have also been significantly influenced by severe convective storms. Of note, Tornado Alley in the United States has been shifting beyond the Great Plains area, expanding to include the Midwestern and Southeastern United States.

The distinction between primary catastrophe perils (hurricanes and earthquakes) versus secondary perils (severe convective storms and wildfires) has become less important, with secondary peril activity rising and accounting for a greater share of losses than in past years.

AM Best’s outlook for the U.S. personal lines segment has been revised to Stable from Negative, in line with a corresponding change in the personal auto outlook to Stable from Negative. The outlook for the homeowners line remained at Negative.

U.S. personal lines insurers were met with multiple challenges

U.S. personal lines carriers were met with multiple challenges after the onset of the COVID-19 pandemic in 2020 significantly increasing loss costs. Factors contributing to higher costs include the economic impact of inflation in various areas (repair parts, labor, medical costs), supply chain disruptions, higher incidence of fatalities/severe injuries, more advanced technology in newer vehicles and elevated jury awards in litigated claims.

Insurers recognized the need to respond by aggressively pushing for higher rates to better account for these more volatile trends. Large increases have been achieved over the last two years, appearing to get to a more adequate position within personal auto.

Given the different state regulations across the United States, rate increase approvals have varied.

Most state governments have understood the need for large rate increases given the macroeconomic influences carriers have had to contend with. On the homeowners side, in addition to base rate changes, several carriers have increased inflation guard factors and made a concerted effort to correct insurance-to-values for current standards.

Best US Property & Casualty Insurers in 2025 by admitted assets

Top 10 US P&C Insurers by total admitted assets

- Berkshire Hathaway Ins

- State Farm Group

- Liberty Mutual Ins Cos

- Travelers Group

- Chubb INA Group

- Progressive Ins Group

- Allstate Ins Group

- Amer Intl Group

- Nationwide P&C Group

- USAA Group

P&C insurers refined underwriting practices

Carriers refined underwriting practices not only to better match rate to risk on a more granular basis but also to hone risk appetites and cull books of risks that sat outside of established risk-tolerance levels.

Greater focus on risk segmentation and tiering has translated into more sophisticated rating algorithms. Carriers recognized the need to evaluate credit risk, age of drivers, limits and coverages purchased, miles driven, specific vehicle characteristics, and many other qualities on a more detailed basis to more effectively capture expected loss costs and exposure.

A by-product of re-underwriting is that several carriers stopped writing new business, did not renew portions of their portfolios, or pulled out of certain areas and lines entirely.

This was more apparent in the homeowners segment. As a result of deep dives into nationwide portfolios leading to nonrenewals and more limited capacity, coupled with large rate increases, insureds began to shop for coverage more often.

The behavioral shift created a need for primary carriers to protect portfolios through more advanced and rigorous vetting processes to protect against adverse selection.

Best US Property & Casualty Insurers in 2025 by net premiums

Top 10 US P&C Insurers by net premiums written

- State Farm Group

- Berkshire Hathaway Ins

- Progressive Ins Group

- Allstate Ins Group

- Liberty Mutual Ins Cos

- Travelers Group

- USAA Group

- Chubb INA Group

- Nationwide P&C Group

- Farmers Ins Group

More robust controls during the quote and binding process were implemented to ensure efforts to refine active books of business and diligently manage the trajectory of growth (or strategic shrinking) were not undone by volatile new business.

Collectively, actions have led to meaningful improvement in the direct loss ratios for both personal auto liability and physical damage.

Best US Property & Casualty Insurers in 2025 by gross premiums

Top 10 US P&C Insurers by gross premiums written

- State Farm Group

- Berkshire Hathaway Ins

- Progressive Ins Group

- Allstate Ins Group

- Liberty Mutual Ins Cos

- Travelers Group

- Chubb INA Group

- USAA Group

- Farmers Ins Group

- Nationwide P&C Group

Homeowners insurers remain challenged by elevated severe weather activity

Conversely, homeowners insurers remain challenged by elevated severe weather activity, adjustments to reinsurance pricing and programs, and the negative impact of inflation on loss costs, driving a higher level of loss experience compared to prior years.

AM Best has revised its outlook for the U.S. personal auto insurance segment to Stable from Negative.

The key drivers of the outlook change were the segment’s improved rate adequacy, a more accommodating regulatory landscape for personal auto insurers, solid risk-adjusted capitalization, and rising investment yields as lower-yielding bonds mature and are reinvested at higher rates.

The personal auto line also benefits from being a leader in leveraging current technology in all operational areas, including claims, underwriting and distribution.

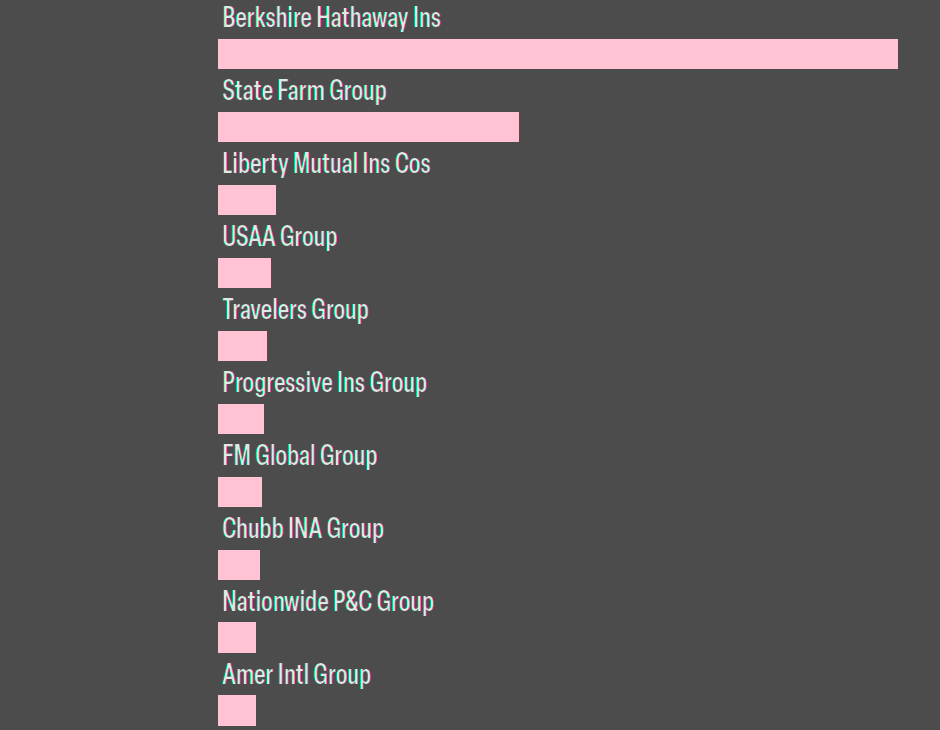

Best US Property & Casualty Insurers in 2025 by policyholders’ surplus

Top 10 US P&C Insurers by policyholders’ surplus

- Berkshire Hathaway Ins

- State Farm Group

- Liberty Mutual Ins Cos

- USAA Group

- Travelers Group

- Progressive Ins Group

- FM Global Group

- Chubb INA Group

- Nationwide P&C Group

- Amer Intl Group

AM Best’s outlook on the U.S. commercial and workers’ compensation insurance lines

AM Best’s outlook on the U.S. commercial lines segment remains at Stable, based on expectations the segment will remain profitable in aggregate and will be resilient in the face of near- and longer-term challenges, according to the Best’s Market Segment Report.

Commercial and specialty insurers are increasingly acquiring or making investments in innovative technologies, both to keep up with evolving market practices and to gain an edge over their competitors with respect to data access and risk selection.

Speed of response is an essential consideration in the highly commoditized small and medium-size risk marketplace, where consistency and streamlined and frictionless processing are essential for both agents and insureds.

Key areas of focus include predictive analytics (telematics and other behavioral-based data gathering and monitoring) to better match price with risk and to provide real-time individual risk-adjusted ratemaking, and the utilization of “big data” and increasingly artificial intelligence—to discover and leverage more nuanced relationships between risk and return.

The outlook for the U.S. workers’ compensation segment—the third-largest component of the commercial lines market, lagging only other and products liability and commercial auto—remains at Stable.

The outlook reflects the sustained performance, despite long-term rate decreases, of the workers’ compensation segment, which has been more profitable than any other line of business, personal or commercial, since 2015, according to a Best’s Market Segment Report, US Property/Casualty: Weather, Reinsurance, and Inflation Drive Results— Again.

AM Best maintains a Positive outlook on the excess and surplus lines segment due to the efficient use of E&S lines capacity as a safety valve for declining capacity in the commercial lines and some of the personal lines markets. Admitted carriers continue to tighten their underwriting criteria, leading accounts to seek coverage in the E&S market.

Property & Casualty Insurance Lines of Business

Property insurance covers damages or loss of property. As a result, rates can be significantly higher in areas susceptible to perils, such as hurricanes. Casualty insurance covers indemnity losses and legal expenses from losses such as bodily injury or damage that the policyholder may cause to others.

When a loss occurs, insurance companies establish a claim reserve for the amount of the expected cost of the claim using a projection of estimated loss costs over a period of time.

While property reserves are established when a property loss occurs and are usually settled soon after a loss, casualty reserves are established for losses that may not be paid or settled for years (i.e., medical professional liability, workers’ compensation, production liability and environmental-related claims).

These long-tail lines of business are so named because of the length of time that may elapse before claims are finally settled.

Determining and comparing profitability among Property & casualty companies typically is achieved through the combined ratio, which measures the percentage of claims and expenses incurred relative to premiums earned/written. A combined ratio of less than 100 means that the insurer is making an underwriting profit. Companies with combined ratios over 100 still may earn an operating profit, however, because the ratio does not account for investment income.

Property & casualty insurance generally falls

Property & casualty insurance generally falls into two areas of concentration: personal and commercial lines. The two largest product lines within the personal lines sector are auto insurance and homeowners insurance.

Commercial lines include insurance for businesses, professionals and commercial establishments. There are many more varieties of commercial lines products than personal lines. The largest two lines are workers’ compensation and other liability.

Personal Insurance Lines of Business

Personal insurance protects families, individuals and their property, typically homes and vehicles, from loss and damage. Auto and homeowners coverages dominate mostly because of legal provisions that mandate coverage be obtained.

Auto insurance

The largest line of business in the property/ casualty sector is auto insurance. According to AM Best’s BestLink database, State Farm Group is the largest writer of both all auto lines and U.S private passenger auto.

The top 50 groups and unaffiliated singles writing all auto insurance lines captured 89.41% of the grand total market in 2023, or $342.27 bn of the $382.79 bn.

Auto insurance includes collision, liability, comprehensive, personal injury protection and coverage in the event another motorist is uninsured or underinsured.

Homeowners insurance

The second-largest line of personal Property & casualty insurance is homeowners, representing a grand total of $152.67 bn in direct premiums written for the U.S. Property & casualty industry in 2023. A standard homeowners policy insures a home’s structure and the policyholder’s belongings in event of a fire or other destructive event. It does not, however, provide coverage in the event of a flood or an earthquake.

Historically, the leading cause of U.S. insured catastrophe losses has been hurricanes and tropical storms, followed by severe thunderstorms and winter storms.

The top 50 groups writing homeowners multiperil coverage represented 87.49% of the U.S. market, according to the BestLink database. State Farm Group is the largest writer of homeowners multiperil coverage.

Two of the largest lines in the commercial segment are workers’ compensation and general liability.

Workers’ Compensation

Insurers on behalf of employers pay benefits regardless of who is to blame for a work-related injury or accident, unless the employee was negligent. In return, the employee gives up the right to sue.

General Liability

General liability insurance protects businessowners (the “insured”) from the risks of liabilities imposed by lawsuits and similar claims. Liability insurance is designed to offer its insureds specific protection against third-party insurance claims; in other words, payment is not typically made to the insured, but rather to someone suffering loss but who is not a party to the insurance contract.

In general, damages caused by intentional acts are not covered under general liability insurance policies. When a claim is made, the insurance carrier has the duty to defend the insured.

FAQ

Property insurance protects against damages or loss of property, while casualty insurance covers indemnity losses and legal expenses related to bodily injury or damages caused to others.

They file a special statement with the National Association of Insurance Commissioners to determine premiums, losses by business lines, and reserve levels.

Key drivers include weather-related events, inflation, advanced vehicle technology repair costs, supply chain disruptions, and higher jury awards.

Through effective risk selection, rate increases, investments in advanced technology, and streamlined underwriting practices.

Auto insurance is the largest in personal lines, while workers’ compensation and liability dominate the commercial lines segment.

Carriers have adjusted base rates, inflation guard factors, and insurance-to-value ratios to account for higher costs in materials and labor.

The revision reflects improved rate adequacy, favorable regulatory changes, better capitalization, and rising investment yields.

……………….

Ratings & Data Analytic Services: Arthur Snyder IV – AM Best’s Senior Director, Maryrose Paar – AM Best’s Director USA, Brian Schlesinger – AM Best’s Associate Director

Edited by Nataly Kramer