Overview

Reinsurance renewals reflect a shift in market conditions. Property reinsurance rates have softened, though profitability remains strong. Casualty renewals face closer scrutiny, but capacity remains available. During the January renewals, demand for reinsurance coverage remains elevated.

Following an increase in capital supply, the market conditions have become slightly more competitive compared to the peak level of the cycle observed last year.

The reinsurance industry’s capitalization is on pace to reach all-time highs, and credit profiles continue to improve, according to AM Best market report.

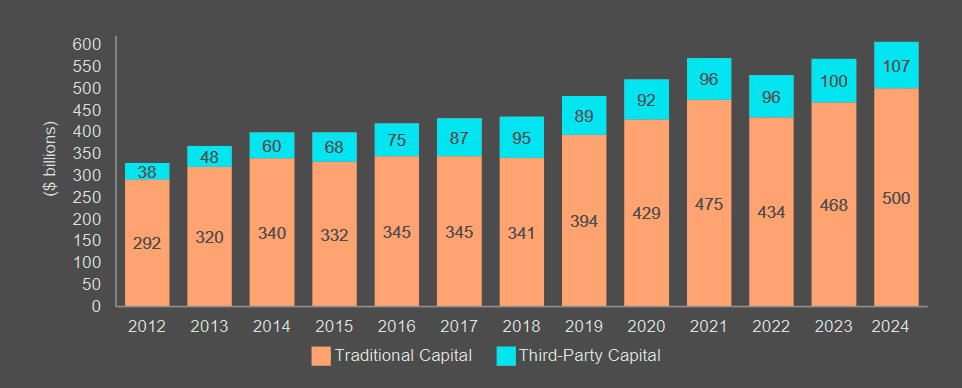

Global reinsurance market entered 2025 with a record $500 bn in traditional reinsurance capital, supported by strong earnings and reduced investment volatility. Third-party capital also set a new high of $107 bn, driven by investor reinvestment.

The 2024 hurricane season sparked concerns over potential $100 bn industry losses. However, losses remained manageable as storms followed standard catastrophe models, Beinsure noted.

Global reinsurers strengthened pricing and attachment points, reducing exposure to secondary perils. Increased capital has pressured property rates, but reinsurers are maintaining strict terms.

Key Insights

- Property reinsurance rates are easing, though profitability remains high.

- Casualty reinsurance faces tighter scrutiny but renewals proceed without capacity shortages.

- Traditional reinsurance capital reached a record high, driven by strong earnings and lower investment volatility.

- Third-party capital is expanding as investors reinvest gains.

- The industry faces increased uncertainty in 2025, following higher losses from secondary perils and economic instability.

Casualty reinsurance renewals are uncertain due to rising claims costs from social inflation. Many reinsurers strengthened reserves in 2024, a trend expected to continue. Some signaled plans to scale back on casualty business, but renewals still secured sufficient capacity.

FY data for global reinsurers indicates that net claims losses of around $15 bn would be necessary for the composite’s ROE to match a cost of capital exceeding 15%, excluding tax implications.

AM Best views the hurricane losses as an earnings event rather than a capital one (see Global Reinsurance Capital & Catastrophe Bond Market Dynamics).

California wildfires and severe winter storms have heightened concerns for 2025, Beinsure noted. Had the fires occurred earlier, they might have influenced renewals more significantly. As companies release financial reports, further reserve strengthening is likely. Despite early-year challenges, reinsurers remain well-positioned, with growing capital and improved credit profiles. The mid-year renewal period will provide further insight into market stability.

Reinsurance Market Conditions Leading into 2025

In 2024, reinsurance premium rates increased, interest rates remained high, and capital markets performed well. The composite achieved its highest ROE in five years. Retained earnings grew due to strong underwriting and solid net investment income. Surplus rose, driven by unrealized capital gains, lower dividends, and reduced share buybacks.

The lead-up to January 2025 renewals was unpredictable, with uncertainty about how results would affect negotiations. The year began with concerns over the US hurricane season, given the risk of significant losses. Storm frequency and severity exceeded normal levels, with Hurricanes Helene and Milton triggering market reactions. However, as they progressed, losses remained manageable, avoiding extreme financial strain.

Heading into reinsurance renewals, industry participants questioned reinsurers’ response to hurricane activity. A $100bn annual loss was a key concern, recalling prior years when similar losses led to reduced property capacity and tighter market conditions.

However, 2024’s losses mainly stemmed from well-modeled primary perils. In contrast, prior years saw significant losses from secondary perils with weak modeling, making risk assessment more difficult. The 2024 hurricanes aligned with standard catastrophe models, meaning their financial impact fell within expected parameters. While secondary perils persisted, reinsurers reduced exposure by increasing attachment points and refining pricing.

Ultimately, hurricane losses were less severe than feared. Coupled with strong investment performance, reinsurers improved their capital positions, increasing available property capacity for 2025. This affected property rates, but reinsurers maintained firm attachment points and strict terms to limit exposure to unmodeled perils, Beinsure noted.

Property & Casualty Renewals Face Margin Pressures

Property reinsurance renewal trends are clear, but casualty renewals present more uncertainty regarding profitability. Social inflation continues to drive claims costs higher.

In 2024, several reinsurers bolstered their casualty reserves, a trend expected to persist as companies report year-end results.

Much of this reserve growth relates to recent accident years, with some strengthening past reserves as well. With limited ways to offset rising loss trends, many reinsurers signaled plans to reduce casualty exposure. Despite this, programs continued to secure sufficient capacity.

Reinsurers are likely to push for double-digit increases in U.S. casualty premium rates during the January 2025 reinsurance renewals. This move aims to address higher loss costs. Rising social inflation in the U.S. casualty sector remains a major risk, keeping the global reinsurance sector outlook neutral.

General liability and excess/umbrella placements that are US exposed experienced continued reinsurance pricing pressure for excess of loss programs, while quota share outcomes were tied to the amount of adverse development.

Casualty lines were the least popular choice (16%), likely reflecting the difficulty of managing rising casualty costs driven by social inflation.

Analytics expect reinsurers to seek double-digit rate increases for US casualty insurance premiums at renewals and to cut cover limits and quota-share commissions.

Opinions varied on whether pricing will offset the increasing loss trends in property-catastrophe lines. Around 39% believe it will, while 36% disagree, and 25% remain uncertain.

Traditional Reinsurance Capital Near Record Highs

AM Best revised its 2024 traditional reinsurance capital estimate down to $500bn from its previous $515bn projection. The revision stemmed from special dividends issued by major US and Bermuda reinsurers, along with reserve increases.

Still, the 6.8% increase from the prior year pushed capital levels past the previous peak of $475bn in 2021.

Estimate of Total Dedicated Reinsurance Capital

Reinsurers and brokers have mixed expectations for 2025 pricing, according to Fitch Ratings’ survey.

The Jan. 1, 2025, reinsurance renewals marked a return to normalcy after challenging conditions two years ago. Back then, a dramatic increase in property and property catastrophe (short-tail lines) reinsurance pricing, driven by years of underperformance, led to a frantic and disorderly market renewal.

In contrast, buoyed by two years of strong and favorable returns, reinsurers entered this year’s renewals with a greater willingness to deploy capacity, Beinsure noted.

As a result, our view of the global reinsurance sector remains stable, reflecting forecast credit trends over the next 12 months, including the distribution of rating outlooks, existing sector-wide risks, and emerging risks.

Growth in Third-Party Capital

Guy Carpenter adjusted its year-end 2024 estimate for third-party capital to $107 bn, up from an earlier range of $105 bn to $110 bn. This marks a new record, surpassing 2023 levels. Since the property reinsurance market hardened in 2022, the ILS market has gained traction.

While early growth was limited by capital constraints, recent years have seen fewer major loss events, allowing investors to withdraw earnings. However, in 2024, many opted to reinvest, further expanding available capacity.

Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January. Analytics expect combined ratios to hover around 90% in 2025 and the sector return on equity to fall slightly to 17% from 19% in 2024. The sector outlook remains ‘neutral’.

Reinsurance Market Outlook

The industry faces critical developments in 2025. Reinsurers had recovered from a period of weak performance and improved pricing models for secondary perils. Global reinsurers brace for mixed reinsurance pricing outlook in 2025. This allowed some rate relief. However, early 2025 events introduced new concerns, Beinsure noted.

California wildfires could become the most expensive on record, raising questions about how programs will absorb the losses.

Had the fires started earlier, they might have significantly influenced renewals. Additionally, severe winter storms in the Southeast reinforced concerns about secondary perils.

In the coming months, companies will release full-year financial reports, including actuarial assessments. Many are expected to strengthen casualty reserves, but the impact on investor confidence and capital levels remains uncertain.

Reinsurance renewals throughout 2025 will be closely watched. Reinsurers have adapted well to past challenges, maintaining profitability and expanding capital. Despite a rough start to the year, the industry remains positioned for continued growth. The mid-year renewal period will be a key test for market stability.

FAQs on Reinsurance Renewals 2025

Increased capacity from improved capital positions has put downward pressure on rates, though reinsurers maintain strict terms to manage risk.

Rising claims costs from social inflation have led reinsurers to strengthen reserves, though capacity remains sufficient for renewals.

Strong earnings and lower investment volatility allowed reinsurers to build capital, reaching $500bn by the end of 2025.

Many investors reinvested their gains in 2024, pushing third-party capital to $107bn, surpassing the previous record from 2023.

Industry participants feared another $100bn loss year, but actual losses remained manageable due to storms aligning with standard catastrophe models.

California wildfires and Southeast winter storms raise concerns over secondary perils, while economic uncertainty adds further unpredictability.

Companies will release full-year financials, likely strengthening casualty reserves, and reinsurers’ responses will shape capital positions and pricing trends.

………………

AUTHORS: Carlos Wong-Fupuy – Senior Director, global reinsurance ratings AM Best, Steven M. Chirico – Director AM Best, Michael Lagomarsino – Director AM Best