Overview

- Reinsurance pricing cycle may have peaked in 2025

- What are your expectations for reinsurance pricing at the January 2025 renewals?

- Which reinsurance business lines will offer the most attractive margins at the January 2025 renewals?

- Will price increases be sufficient to compensate for increasing loss trends in property-catastrophe?

Reinsurers and brokers have mixed expectations for 2025 pricing, according to Fitch Ratings’ survey from the annual Rendez-Vous gathering in Monte Carlo.

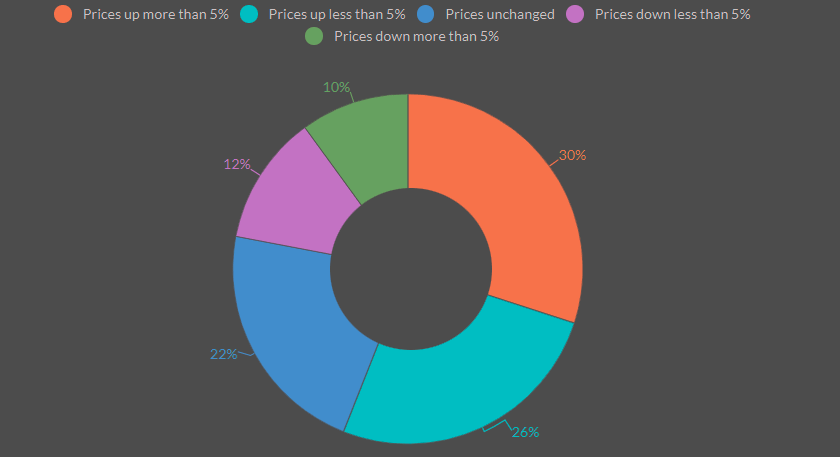

More than 50% of the 81 respondents—reinsurers, insurers, and brokers—think global reinsurers will raise prices in January 2025 renewals, continuing recent increases driven by high claims inflation. Around 30% expect price hikes above 5%, while 26% foresee smaller increases.

Only 22% predict prices will drop, a view Fitch shares. Fitch believes the market may have reached its pricing peak, expecting 2025 to bring a softer market due to abundant capital in the sector. To reflect this, Fitch shifted its global reinsurance sector outlook from ‘improving’ to ‘neutral.’

Reinsurance pricing cycle may have peaked in 2025

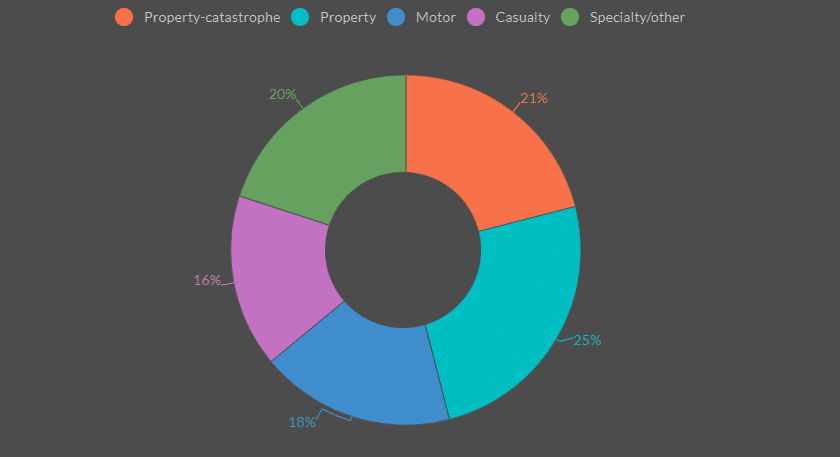

Respondents were split on which business lines might offer the best margins at January 2025 reinsurance renewals.

The mid-year reinsurance renewals occurred against a continued increase in reinsurer appetite as overall reinsurance capacity grew. This uptick in capacity occurred against a backdrop of strong capital growth and robust reinsurer returns. In 2023, reinsurers in the Guy Carpenter Index added approximately $35 bn to traditional shareholders’ equity capital.

Casualty renewal outcomes varied by sublines as well as reinsurance type

General liability and excess/umbrella placements that are US exposed experienced continued reinsurance pricing pressure for excess of loss programs, while quota share outcomes were tied to the amount of adverse development.

Casualty lines were the least popular choice (16%), likely reflecting the difficulty of managing rising casualty costs driven by social inflation.

Fitch expects reinsurers to seek double-digit rate increases for US casualty insurance premiums at renewals and to cut cover limits and quota-share commissions.

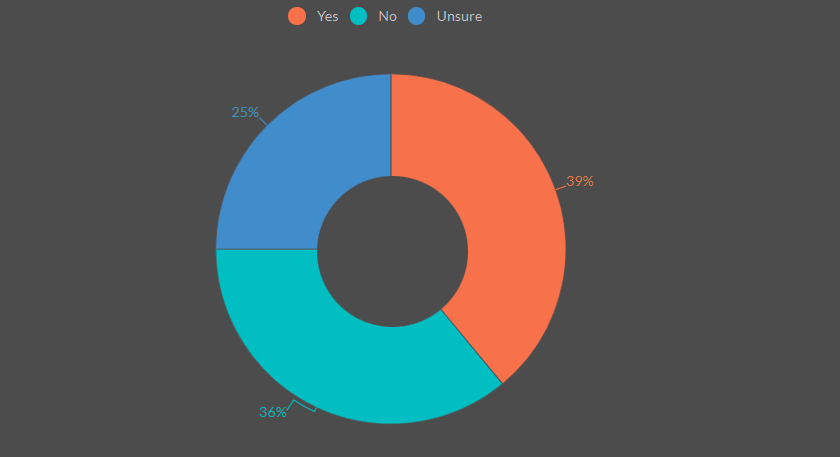

Opinions varied on whether pricing will offset the increasing loss trends in property-catastrophe lines. Around 39% believe it will, while 36% disagree, and 25% remain uncertain.

According to Global Reinsurance Property Catastrophe Market Outlook, the general dynamic of more capacity being available for upper layers and constrained appetite for lower layers has been modestly tempered by a slight increase in reinsurers moving lower into programs to secure shares higher in a program.

Global property catastrophe reinsurance risk-adjusted rates at mid-year were generally flat to mid- to high-single digits.

In some cases, upper layers were risk-adjusted down 10% or more for non-loss impacted accounts. Pricing movement was heavily dependent on account specific factors including portfolio composition and historical pricing movement.

The material increases in demand for catastrophe reinsurance have easily been met by growing market appetite.

The past year and half have seen major changes in the global Reinsurance Property Catastrophe (CAT) market. In the recent reinsurance renewals we have seen robust price improvements, increased net retentions and much tighter terms and conditions

Fitch expects reinsurers to maintain strong property-catastrophe profits, even as prices ease, with underlying margins near their 2023–2024 peaks in 2025.

Increased capital buffers and reserves, supported by record 2023 and first-half 2024 profits, should help reinsurers stay disciplined. Fitch expects them to continue enforcing strict terms to manage risks from secondary peril events, given the rise in climate-related losses.

What are your expectations for reinsurance pricing at the January 2025 renewals?

Which reinsurance business lines will offer the most attractive margins at the January 2025 renewals?

Will price increases be sufficient to compensate for increasing loss trends in property-catastrophe?

FAQ

Fitch’s survey indicates varied expectations, with just over half of participants expecting global reinsurers to increase prices in January 2025 renewals. High claims inflation has driven these recent years’ price rises.

About 30% of respondents anticipate price hikes above 5%, while 26% foresee more moderate increases. Only 22% expect prices to decrease.

Yes, Fitch shares the view of those predicting lower prices. They believe the pricing cycle has likely peaked, anticipating a softer market in 2025 due to ample capital in the reinsurance sector.

Participants are split on which lines may yield the best margins, though casualty lines were the least favored (16%), likely due to rising casualty costs from social inflation.

Fitch expects reinsurers to seek double-digit rate increases in US casualty premiums and to reduce cover limits and quota-share commissions at renewals.

Survey respondents are divided, with 39% believing prices will offset rising loss trends in property-catastrophe lines, 36% disagreeing, and 25% uncertain.

Fitch believes reinsurers will sustain strong property-catastrophe profitability in 2025, supported by reinforced capital buffers and reserves from 2023–2024 gains. They expect reinsurers to maintain strict terms to mitigate exposure to volatile weather-related losses linked to climate change.

……………….

AUTHORS: Manuel Arrive, CFA – Director, Insurance at Fitch Ratings Ireland, Brian Schneider, CPA, CPCU, ARe – Senior Director, Insurance at Fitch Ratings, David Prowse – Senior Director at Fitch Wire