Overview

Global re/insurers reported improved underwriting results and capital positions. These gains came alongside rising uncertainty around reserve development and expanding loss gaps, particularly in high-risk areas, according to Howden Re’s report.

Howden Re Business Intelligence explores key market movements from (re)insurance earning updates. This includes analysis on reserve volatility, widening loss gap, pricing and capital recovery.

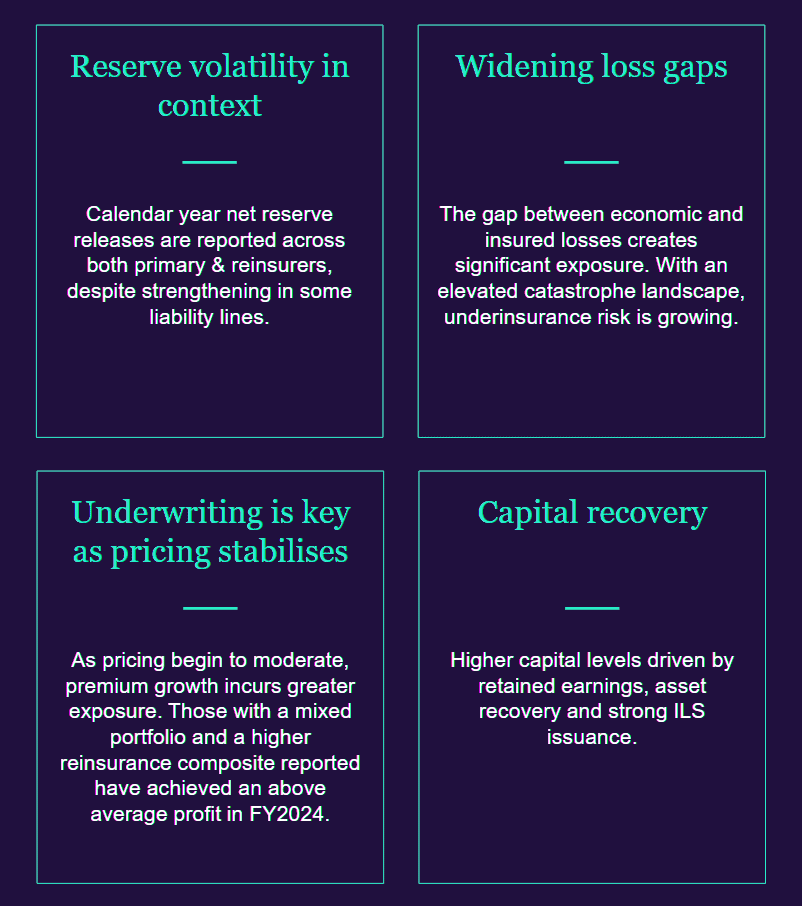

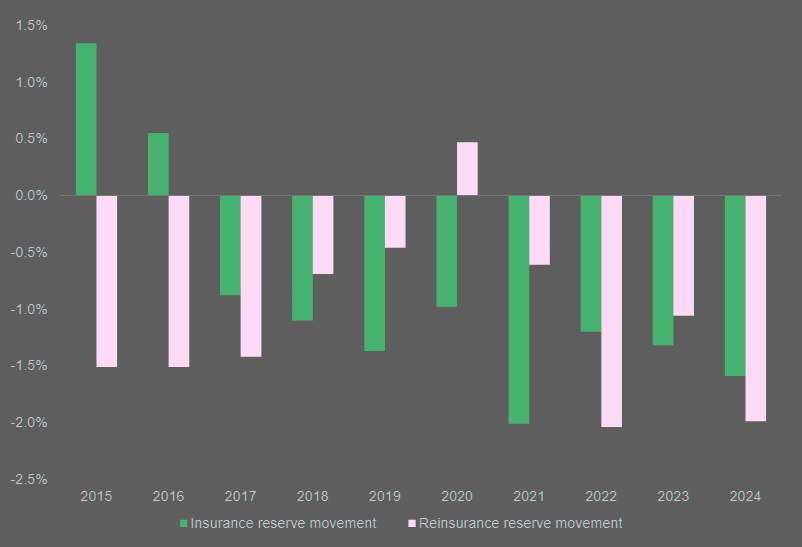

Reserve volatility remains a concern despite calendar year net reserve releases reported across primary and reinsurance carriers. Some liability lines still show signs of reserve strengthening.

5 Key Highlights

- Combined ratios improved by 3.6pts, exceeding the five-year average performance.

- Capital levels recovered on the back of retained earnings, asset value recovery, and strong ILS issuance, despite higher dividends and buybacks.

- Secondary perils pushed the insured vs. economic loss gap higher, increasing underinsurance risk.

- Rate momentum faded, shifting premium growth reliance to exposure. Pricing flattened or declined across many lines.

- Munich Re, Swiss Re, Hannover Re, and SCOR posted a 14% average RoE and 86.3% average combined ratio, showing continued profitability despite moderating risk-adjusted prices.

The gap between economic and insured losses continues to grow, increasing exposure. With catastrophe frequency rising, underinsurance risk is also climbing.

Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January.

The lower reinsurance prices reflect an abundance of capital, with the reinsurance cycle now past its peak, but market conditions remain supportive of strong risk-adjusted returns.

Fitch expects combined ratios to hover around 90% in 2025 and the sector return on equity to fall slightly to 17% from 19% in 2024. The sector outlook remains ‘neutral’.

As pricing stabilises, premium growth increasingly depends on exposure. Carriers with diversified portfolios and stronger reinsurance programmes reported above-average profits in FY2024.

Capital levels have recovered, supported by retained earnings, asset value rebound, and strong ILS issuance.

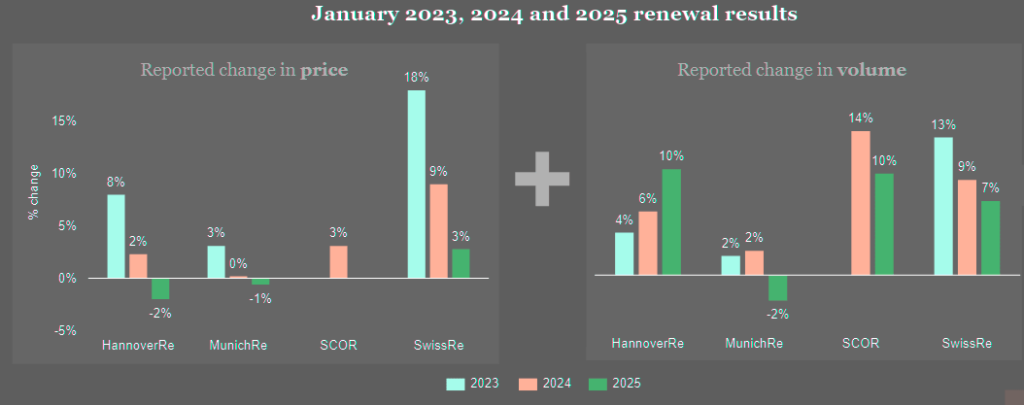

Reinsurers experienced stable reinsurance renewals

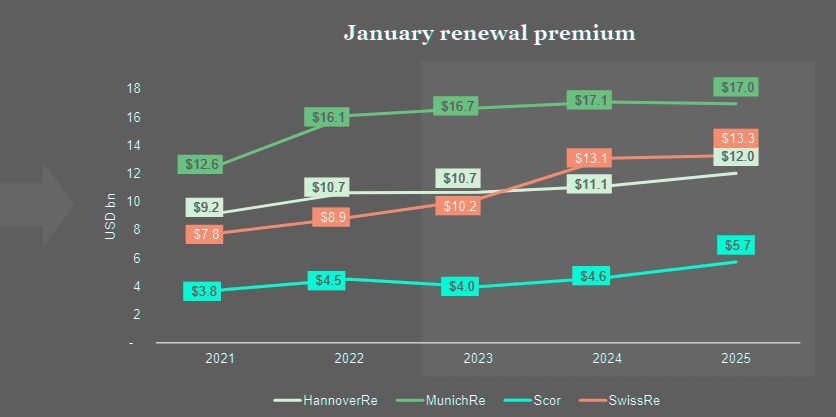

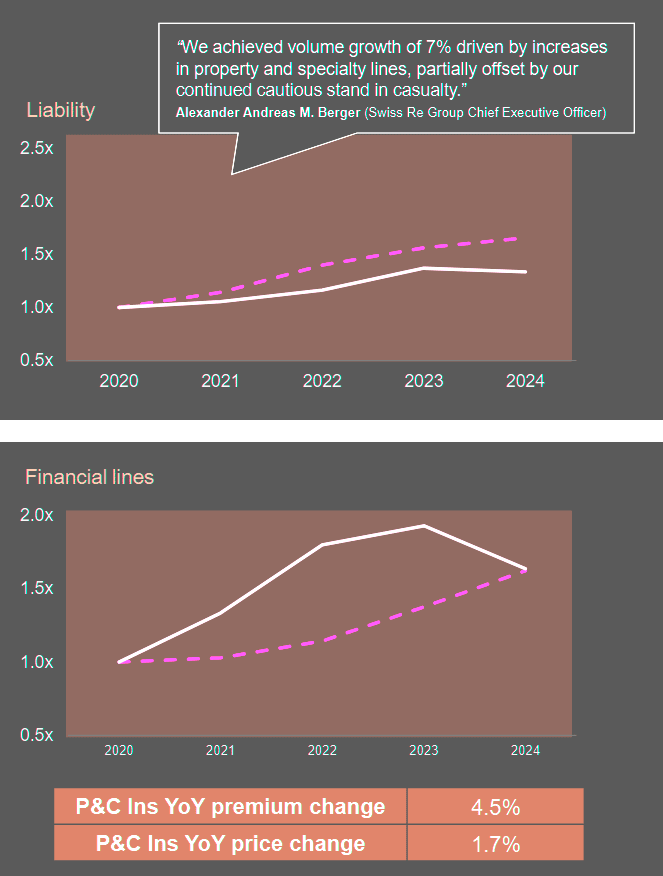

January reinsurance renewal premiums increased by 4.5%, primarily driven by volume. Reinsurers experienced stable reinsurance renewals at 1.1 due to greater prudence and selective focus in underwriting, Beinsure noted.

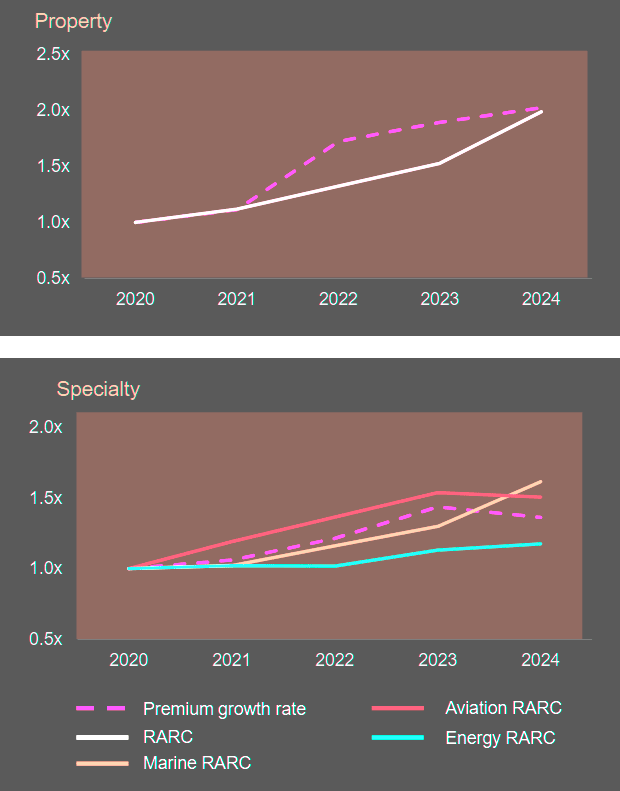

- Premium growth in 2024 was driven more by volume than rate, as rising exposure—particularly in property—pushed up demand for reinsurance.

- Natural catastrophe pricing declined slightly, while casualty pricing remained stable or increased. This was due to a cautious inflation outlook and updated loss models.

- Munich Re applied strict portfolio management, prioritising key client relationships and selective growth.

- Terms and conditions remained favourable. Ample retrocession capacity encouraged flexible purchasing strategies.

According to Barclays, “There is little evidence of capacity stepping back… we expect the reinsurance market to remain oversupplied for April, June/July renewals and into 2026.”

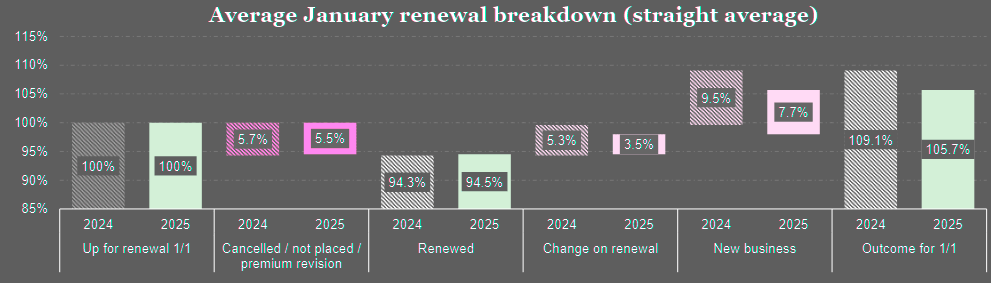

SCOR’s renewal breakdown is for their treaty book of business, and is based on EGPI (Estimated Gross Premium Income, U/W year) in 2025.

Pricing stabilised across many lines after a period of steep increases

However, January 1st, 2025, renewals showed that volumes remain below 2023 levels, suggesting a shift in market dynamics.

Pricing is no longer a major growth driver. Carriers are now growing through exposure, though exposure levels remain low by historical standards.

Michelle To, Head of Business Intelligence at Howden Re

Premium growth now exceeds pricing in some lines, such as liability. The report stressed the need for consistent underwriting discipline as rate momentum fades.

Varying trends found between pricing and premiums across LoB’s

Attention shifts to upcoming renewals where pricing is expected to moderate.

P&C insurance lines

P&C reinsurance lines

In 2024, average underwriting performance exceeded the 2019–2023 period, with combined ratios improving by 3.6 percentage points.

Reinsurance strategies played a key role in performance outcomes. The report pointed to smart, selective reinsurance buying as a major differentiator across the sector.

David Flandro, Head of Industry Analysis and Strategic Advisory

Looking ahead, Flandro warned that California wildfire losses could deepen the global loss gap in 2025. “The LA wildfires could contribute to a 60–90bn loss gap,” he said. “The gap is widening globally, making it harder for policyholders and cedents to access coverage.”

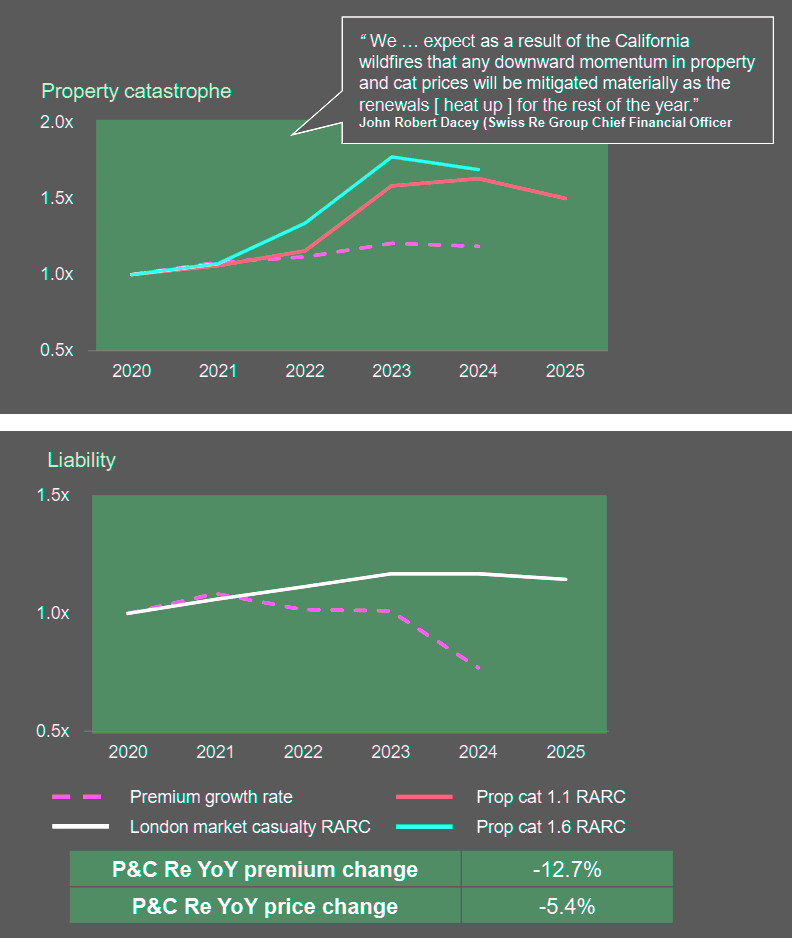

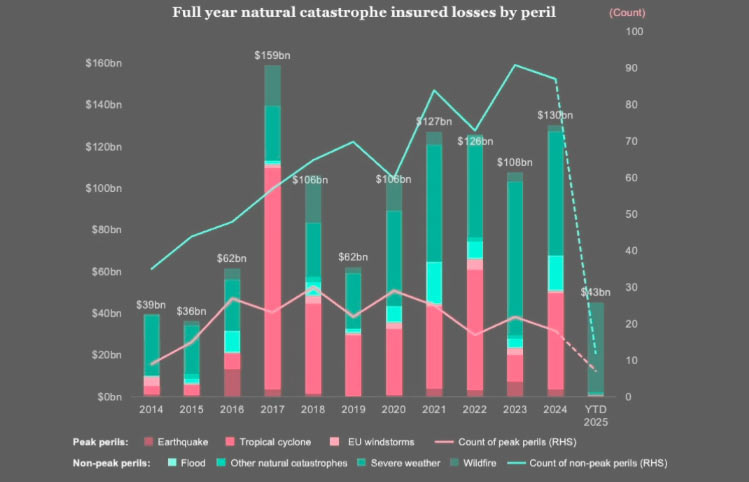

Natural catastrophe insured losses above $100 bn for 5th consecutive year

Secondary perils, especially convective storms and wildfires, continue to increase in severity and are starting to behave like primary perils. These events have caused annual losses of over $100bn for five consecutive years.

The growing prominence of non-peak perils in 2024 underscores a shifting risk landscape.

Full year natural catastrophe insured losses by peril

Share of $42.8bn insured loss estimate for 2025 LA wildfire

The report highlighted weak liability reserve development as a growing issue. However, this was partially offset by positive reserve movement in workers’ compensation, short-tail, and specialty lines. The report questioned whether these positive offsets can continue.

Despite these concerns, the report showed a clear increase in carrier book values. Underwriting and investment results drove capital growth in 2024.

This growth came even with higher dividend payouts and share buybacks, and it supports expanded capacity across reinsurance programs.

Capital recovery was supported by strong investment gains

Capital recovery in 2025 was supported by strong investment gains and high levels of ILS issuance. The report also noted that economic conditions since 2022 have mirrored the strongest growth period since 2007, which supported underwriting across most lines, Beinsure noted.

Flandro concluded that sustainable growth will depend on exposure growth rather than pricing. “It’s still an underwriters’ market. There’s room for innovation and further value creation.”

Reserve movement as a % of NPE

Europe’s four largest reinsurers—Munich Re, Swiss Re, Hannover Re, and SCOR—reported strong financial results in 2024. Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January.

Property and casualty underwriting reached a cycle high

The group—Munich Re, Swiss Re, Hannover Re, and SCOR—reported an average return on equity of nearly 14% in 2024, down from 17% in 2023 but still reflecting strong performance.

The average combined ratio improved to 86.3%, a 1 percentage point gain. This was driven by stable pricing and fewer large losses.

Property re/insurance rates remained stable, reflecting increased capacity and improved coverage terms following a strong reinsurance renewal season.

Reinsurers prioritized key clients, offering long-term agreements while maintaining scrutiny over high-risk industries such as food and beverage, waste and recycling, and wood and paper.

FAQ

Premium growth in 2024 was led by volume rather than rate. This was largely due to increased exposure, especially in property lines.

Natural catastrophe pricing declined slightly, while casualty lines saw stable or rising rates due to inflation concerns and model revisions.

Despite net reserve releases across carriers, reserve volatility remains a concern, particularly in liability lines where strengthening continues.

Secondary perils, including convective storms and wildfires, drove over $100bn in annual insured losses for the fifth year in a row, contributing to a widening protection gap.

Underwriting performance exceeded the 2019–2023 average, with combined ratios improving by 3.6 percentage points. Reinsurers reported stable renewals and strong capital positions.

Selective reinsurance purchasing and portfolio focus were key performance differentiators. Carriers with diversified portfolios and strong reinsurance composite outperformed peers.

Barclays noted no signs of capacity retreat. The market is expected to remain oversupplied into 2026, supporting stable terms and increased purchasing flexibility.

……………………

AUTHORS: Michelle To – Head of Business Intelligence at Howden Re, David Flandro – Head of Industry Analysis and Strategic Advisory