Overview

Europe’s four largest reinsurers—Munich Re, Swiss Re, Hannover Re, and SCOR—reported strong financial results in 2024 for a second year, reinforcing their credit profiles ahead of potentially weaker market conditions in 2025, according to Fitch Ratings. Beinsure analyzed the Fitch’s report and highlighted the key points.

Reinsurance rates in Europe declined 2% in the fourth quarter of 2024. The European reinsurance industry faced a year of changes and challenges, with the top 10 reinsurance companies remaining consistent while a noticeable reshuffling occurred further down the rankings.

Improved market conditions, disciplined underwriting, and solid investment returns supported capital growth and reserve strengthening last year.

Key Highlights

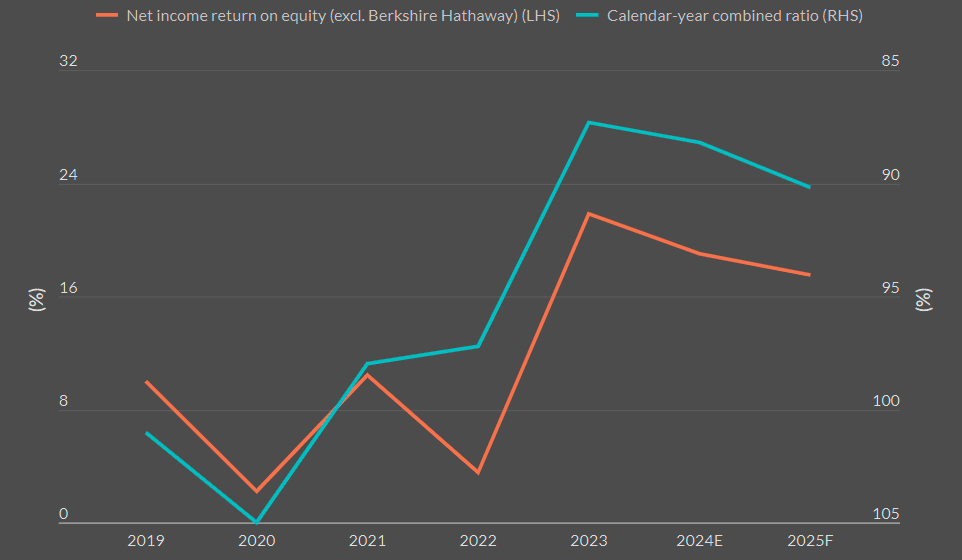

- Return on equity averaged 14% across the four major reinsurers, reflecting another year of strong profitability.

- Combined ratio improved to 86.3%, a cycle low, supported by stable pricing and fewer major losses.

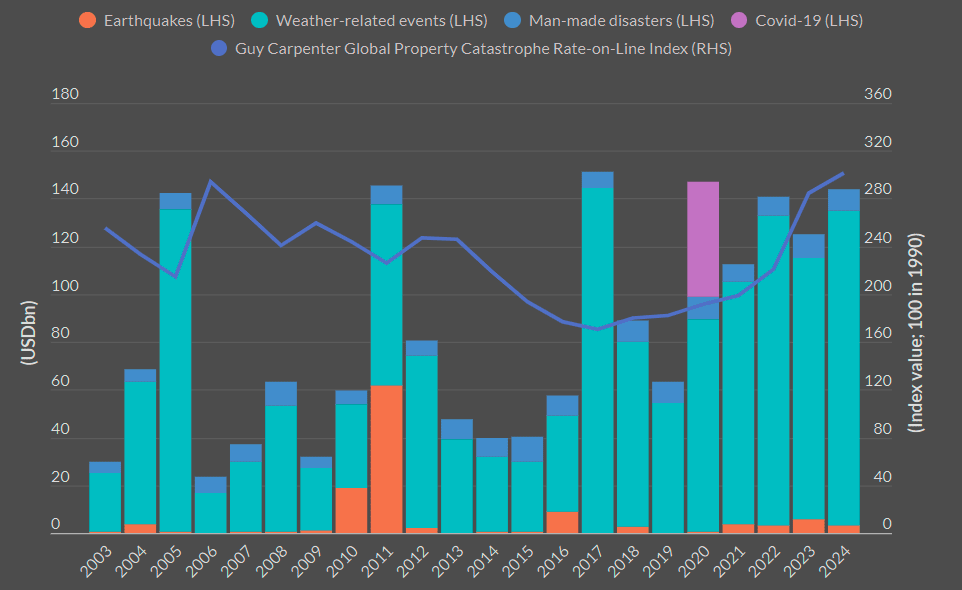

- Natural catastrophe losses hit $150bn, but reinsurers’ budgets remained intact due to higher retention by primary insurers.

- January 2025 renewals showed mild softening, with increased capacity and competitive pricing, especially in property lines.

- Reinsurers maintained capital strength, enabling strategic reserve builds and positioning them for continued stability in 2025.

Bolstered capital from strong earnings in 2024 led to ample capacity and strong reinsurer capital positions, contributing to a more orderly renewal season despite ongoing challenges from natural catastrophes and adverse casualty trends, according to Beinsure`s data.

Strong Performance Strengthens Financial Position

Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January.

The group—Munich Re, Swiss Re, Hannover Re, and SCOR—reported an average return on equity of nearly 14% in 2024, down from 17% in 2023 but still reflecting strong performance.

Property and casualty underwriting reached a cycle high. The average combined ratio improved to 86.3%, a 1 percentage point gain. This was driven by stable pricing and fewer large losses.

Property re/insurance rates remained stable, reflecting increased capacity and improved coverage terms following a strong reinsurance renewal season.

Reinsurers prioritized key clients, offering long-term agreements while maintaining scrutiny over high-risk industries such as food and beverage, waste and recycling, and wood and paper.

All four reinsurers beat guidance, except Swiss Re. Its combined ratio worsened due to prior-year US liability reserve additions.

The group used strong P&C results to increase specific claims reserves and build general prudence, which Fitch considers positive for reserve adequacy.

The Global Insurance Market Index is proprietary measure of commercial insurance rate changes at renewal. Property insurance rates remained unchanged, signaling continued moderation in price increases.

In contrast to the sharp increase in property and property catastrophe reinsurance pricing during prior years, this renewal cycle proceeded in a more orderly manner. Reinsurers, supported by two consecutive years of strong returns, entered 2025 with greater confidence and a willingness to deploy capital.

S&P’s outlook for the global reinsurance sector remains stable, reflecting expected credit trends, sector-wide risks, and emerging challenges over the next 12 months.

Strong underwriting performance in short-tail lines, higher net investment income, and asset value recovery contributed to strong 2024 operating earnings. These factors further reinforced the industry’s capital position.

The report highlighted downward pricing pressure in property and catastrophe lines, primarily driven by strong earnings and abundant capital.

Reinsurers’ Profitability

A strong reinsurance renewal season led to more capacity, better pricing, and improved coverage terms. Incumbent insurers prioritized key clients, limiting opportunities for new entrants in favorable risk segments.

Casualty insurance rates in Europe flattened after 21 consecutive quarters of increases. Greater capacity, particularly in the Mediterranean, fueled competition.

Major insurers provided competitive terms, with some clients securing three-year agreements. Risks with minimal U.S. exposure saw fewer restrictions, and quota-share placements rose due to oversubscriptions.

Catastrophe Exposure and Reserve Management

Natural catastrophe losses reached $150bn in 2024, the fifth year in a row with losses above $100bn. Most losses came from hurricanes, convective storms, and medium-sized events like floods in Europe and the Middle East. These events mostly stayed within primary insurers’ retention levels.

Fitch noted that 85%–90% of losses were frequent, low-severity weather events known as secondary perils.

These were largely absorbed by primary insurers due to higher attachment points. Reinsurers were mostly affected by larger events, particularly hurricanes Milton and Helen.

Fitch warned that catastrophe budgets may come under pressure in 2025. A hypothetical wildfire scenario in Los Angeles would result in losses of about $40bn, equal to 35% of the annual catastrophe budget.

The reinsurers also used the strong 2024 performance to strengthen reserves and increase buffer levels. Fitch viewed this positively in its reserve adequacy assessment.

Insured Catastrophe Losses

However, the vast majority of these losses (85%-90%) were absorbed by primary insurers due to higher attachment points, a situation that will persist in 2025 as reinsurers stay cautious on secondary peril exposure.

As a result, natural catastrophe losses in 2024 were generally within reinsurers’ budgets, which attracted capital to the sector, adding to pressure on pricing.

Property reinsurance prices fell by 5%-15% for loss-free accounts at the January renewals, with more remote, high attaching layers, which have the highest margins, most affected. Price increases for loss-affected regions were up to 20%.

Outlook for 2025 and Market Conditions

In life and health (L&H), results varied. Munich Re, Hannover Re, and to a lesser extent Swiss Re, reported solid margins from contractual service releases and new business.

SCOR, however, faced losses due to changes in reserving assumptions, highlighting earnings volatility in this segment.

At the January 2025 renewals, reinsurers saw slightly lower risk-adjusted pricing due to excess capacity. Despite minor price drops, underwriting discipline remained firm, and contract terms held steady.

Premium growth was supported by volume increases in specialty lines and alternative products. Reinsurers stayed cautious on US casualty business due to social inflation concerns. Higher retrocession availability allowed some to expand coverage at lower cost.

Fitch kept a neutral outlook on global reinsurance for 2025

Positive elements include stable underwriting margins, steady pricing, and strong primary P&C markets. Sufficient capital buffers and solid reserves help reduce earnings volatility.

Balanced supply and demand, along with recurring investment income, support the neutral view. However, Fitch expects gradual softening due to increased capacity.

Rising claims costs—driven by inflation, climate-related events, and social inflation—may limit further price declines. Casualty capacity was more limited compared to property and specialty lines, with ceding commissions holding steady or falling slightly.

FAQ

Munich Re, Swiss Re, Hannover Re, and SCOR reported an average return on equity of nearly 14%, backed by strong underwriting and investment results.

Improved market conditions, disciplined underwriting, and solid investment income contributed to capital growth and reserve strengthening.

Rates declined modestly due to surplus capacity. Property reinsurance rates dropped 5%–15% for loss-free accounts, while loss-affected regions saw increases of up to 20%.

Fitch maintained a neutral outlook, citing stable underwriting margins, strong capital buffers, and balanced supply-demand dynamics.

Despite $150bn in insured catastrophe losses in 2024, most losses were absorbed by primary insurers. Reinsurers focused on larger events and maintained budgets within limits.

Yes. Munich Re, Hannover Re, and Swiss Re posted stable results, while SCOR reported losses due to revised reserving assumptions.

They prioritized core clients, offered long-term deals, and exercised caution in high-risk sectors. Retrocession availability supported selective expansion.

………………

AUTHOR: Yana Keller — Editor at Beinsure Media