Overview

Global reinsurers’ profitability will remain strong in 2025 despite lower risk-adjusted prices for most business lines when reinsurance contracts were renewed on 1 January, according to Fitch Ratings report. Beinsure analyzed the report and highlighted the key points.

The lower reinsurance prices reflect an abundance of capital, with the reinsurance cycle now past its peak, but market conditions remain supportive of strong risk-adjusted returns.

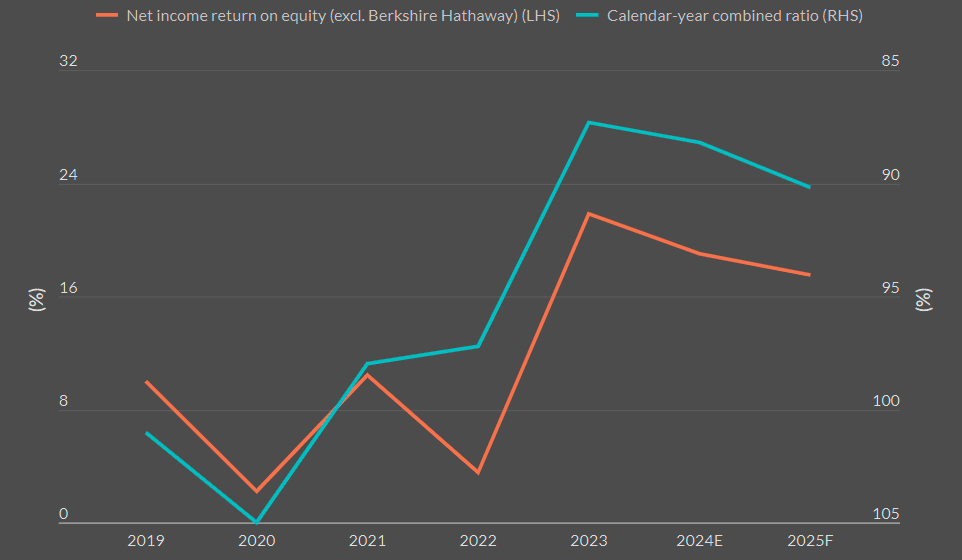

Fitch expects combined ratios to hover around 90% in 2025 and the sector return on equity to fall slightly to 17% from 19% in 2024. The sector outlook remains ‘neutral’.

Key Highlights

- Lower risk-adjusted prices at the January 2025 renewals reflect abundant capital and increasing competition. However, market conditions remain favorable for solid risk-adjusted returns.

- Combined ratios around 90% in 2025. The sector’s return on equity (ROE) is expected to dip to 17%, down from 19% in 2024, while the overall sector outlook remains neutral.

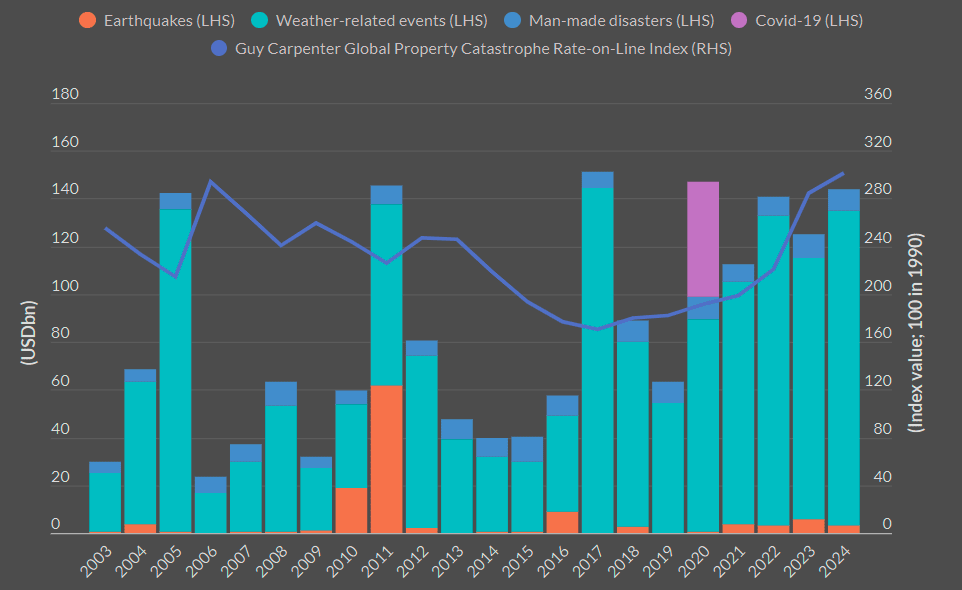

- Insured property catastrophe losses reached $140 bn in 2024, marking the fifth consecutive year of losses above $100 bn. Hurricanes and severe convective storms each accounted for $50 bn, with additional losses from floods in Europe and the Middle East.

- Reinsurers are likely to push for significant U.S. casualty premium rate hikes in 2025 to offset rising loss costs and social inflation risks. Casualty capacity remains tighter than in property and specialty segments.

- Reinsurance capital has risen by over 20% since 2022, supported by strong earnings and higher asset values. Alternative capacity, including cyber catastrophe bonds, continues to expand, reducing earnings volatility.

- Reinsurers have tightened contract terms by raising attachment points, which helped manage losses from large events like Hurricanes Milton and Helene. As a result, primary insurers absorbed most natural catastrophe losses in 2024.

- The ongoing LA fires could cause insured losses between $10 bn and $30 bn, significantly impacting reinsurers’ 1Q25 catastrophe budgets. However, these losses are unlikely to affect ratings, as reinsurers remain well-capitalized.

In 2024, reinsurance premium rates increased, interest rates remained high, and capital markets performed well. According to Global Reinsurance Market Trends Beinsure’s report, the composite achieved its highest ROE in five years.

Retained earnings grew due to strong underwriting and solid net investment income. Surplus rose, driven by unrealized capital gains, lower dividends, and reduced share buybacks.

Analysts highlight the complexity of settling claims, including extensive flood losses and tornado activity. The affected regions faced compounded challenges from both hurricanes, testing the terms and conditions of reinsurance contracts.

ROEs should be evaluated against the forward-looking cost of capital, such as the Market-Derived Capital Pricing Model (MCPM). This metric aligns better with investors’ views.

Global Reinsurers’ Profitability

Reinsurers entered 2025 with solid capital buffers and strong reserves, backed by record profits over the past two years. Additional capacity flowed into the market from traditional reinsurers and institutional investors, drawn by consistent underwriting returns.

This increased risk appetite and growth focus contributed to rate reductions. However, the price cuts did not come with looser contract terms. Reinsurers retained most of the structural improvements secured in recent years. Despite lower rates, premium income is expected to rise in 2025 due to increased volumes.

Market estimates put insured property catastrophe losses for 2024 at about $140 bn. This marked the fifth consecutive year of insured losses exceeding $100 bn. Hurricanes and severe convective storms each accounted for $50 bn, while medium-sized perils, including flooding in Europe and the Middle East, added $13 bn.

Secondary natural catastrophe events were frequent, but reinsurers adjusted policies, shifting away from lower layers close to primary perils. The result was the lowest combined and operating ratios seen in five years.

Hurricanes Milton and Helene together could lead to insured losses of $25 bn to $50 bn. A substantial portion of these losses will likely transfer to the global reinsurance market.

However, stricter reinsurance terms and conditions, which led to higher attachment points, also should help make reinsurers’ losses manageable.

Reinsurers are likely to push for double-digit increases in U.S. casualty premium rates during the January 2025 reinsurance renewals. This move aims to address higher loss costs. Rising social inflation in the U.S. casualty sector remains a major risk, keeping the global reinsurance sector outlook neutral.

Insured Catastrophe Losses

However, the vast majority of these losses (85%-90%) were absorbed by primary insurers due to higher attachment points, a situation that will persist in 2025 as reinsurers stay cautious on secondary peril exposure.

As a result, natural catastrophe losses in 2024 were generally within reinsurers’ budgets, which attracted capital to the sector, adding to pressure on pricing.

Property reinsurance prices fell by 5%-15% for loss-free accounts at the January renewals, with more remote, high attaching layers, which have the highest margins, most affected. Price increases for loss-affected regions were up to 20%.

In specialty insurance, renewal pricing remained stable or saw slight declines. U.S. casualty rates were generally flat to slightly higher, influenced by cedents’ loss histories, reserve developments, and portfolio composition.

Casualty capacity was more limited compared to property and specialty lines, with ceding commissions holding steady or falling slightly.

Reinsurance sector capital has grown by over 20% since the 2022 low, driven by stronger earnings and higher asset values. Alternative reinsurance capacity has also expanded, supported by favorable property catastrophe pricing. This growth is expected to continue in 2025, driven by cyber catastrophe bond issuances, further boosting the sector’s ability to manage earnings volatility.

Traditional and Alternative Reinsurance Capital

The ongoing fires in the Los Angeles area are expected to cause insured losses well above previous wildfire records. These losses will significantly impact reinsurers’ 1Q25 natural catastrophe budgets. However, reinsurer ratings are unlikely to be affected.

Impact on Future Reinsurance Renewal Pricing

The impact on future reinsurance renewal pricing will depend on the final reinsured loss figures and how unexpected the event is compared to catastrophe loss forecasts.

Revenue growth remained strong in 2024 at 9%, similar to the 2023 growth rate. Growth was driven primarily by rate increases rather than volume growth. Volume growth was limited due to shifts in business mix and rising attachment points.

The combined ratio dropped to 84.5%, marking a record low since 2014. This occurred despite a 0.7 percentage point (ppt) decrease in reserve releases and a 0.6 ppt rise in the expense ratio.

Reinsurers and brokers have mixed expectations for 2025 pricing, according to Fitch Ratings’ survey from the annual Rendez-Vous gathering in Monte Carlo.

Only 22% predict prices will drop, a view Fitch shares. Fitch believes the market may have reached its pricing peak, expecting 2025 to bring a softer market due to abundant capital in the sector. To reflect this, Fitch shifted its global reinsurance sector outlook from ‘improving’ to ‘neutral.’

More than 50% of the 81 respondents—reinsurers, insurers, and brokers—think global reinsurers will raise prices in January 2025 renewals, continuing recent increases driven by high claims inflation. Around 30% expect price hikes above 5%, while 26% foresee smaller increases.

The mid-year reinsurance renewals occurred against a continued increase in reinsurer appetite as overall reinsurance capacity grew. This uptick in capacity occurred against a backdrop of strong capital growth and robust reinsurer returns. In 2023, reinsurers in the Guy Carpenter Index added approximately $35 bn to traditional shareholders’ equity capital.

FAQ

Global reinsurers are expected to maintain strong profitability in 2025 due to solid capital buffers, strong underwriting returns, and continued premium growth. Despite lower risk-adjusted prices, the sector benefits from improved earnings, reserve adequacy, and rising net investment income, which will keep profitability stable.

The recent decline in reinsurance prices reflects abundant capital in the market, signaling that the reinsurance cycle has passed its peak. However, strong risk-adjusted returns are expected to persist, supported by stable contract terms and increased reinsurance volumes.

Reinsurance capital has grown by over 20% since 2022, driven by higher asset values, retained earnings, and alternative capacity from institutional investors. This growth is expected to continue, supported by developments such as cyber catastrophe bond issuances, further strengthening the sector’s ability to manage risk.

Insured property catastrophe losses reached $140 bn in 2024, marking the fifth consecutive year of losses exceeding $100 bn. Despite significant hurricane, storm, and flood events, most reinsurers stayed within budgeted catastrophe loss levels, helping maintain their financial resilience.

Specialty insurance renewal prices remained stable or slightly lower, while U.S. casualty rates were generally flat to slightly higher. Casualty capacity remains constrained compared to property lines. Reinsurers are expected to seek double-digit increases in casualty premiums during January 2025 renewals to address rising loss costs and social inflation risks.

The ongoing Los Angeles wildfires are expected to result in insured losses surpassing previous wildfire records. These losses will impact reinsurers’ 1Q25 natural catastrophe budgets. However, the ratings of reinsurers are unlikely to be affected due to their solid capital positions and improved contract structures.

Fitch Ratings maintains a neutral outlook for the reinsurance sector in 2025. While profitability is expected to remain strong, abundant capital is likely to apply downward pressure on prices. Analysts predict a softer market ahead, with rate increases limited to loss-affected regions and specific lines such as U.S. casualty insurance.

…………..

AUTHORS: Manuel Arrive, CFA – Director, Insurance at Fitch Ratings Ireland, Brian Schneider, CPA, CPCU, ARe – Senior Director, Insurance at Fitch Ratings, David Prowse – Senior Director at Fitch Wire