Overview

Two recent public announcements of cyber risk transference by (re)insurers to the capital markets through insurance-linked securities (ILS) issuances represent the potential for a broader reinsurance source for the risk.

Capital markets solutions for cyber (re)insurers

According to Fitch Ratings, capital markets solutions for cyber (re)insurers present the potential for counterparty diversification and an opportunity to lessen “tail risk” for a rapidly growing product line of property & casualty insurance.

Wider development of the cyber risk transfer market requires further maturation of the product, including greater standardization of coverage terms and policy language, price discovery and risk modelling applications.

Cyber risk is difficult to assess due to the dynamic, man-made root causes of claims. Challenges include a lack of widely accepted modelling tools and a limited data set of historical claims where past events are not necessarily indicative of future risks.

Cyber-risk transfer deals

Early deals within the spectrum of cyber-risk transfer will be comprised of cyber risks that are easier to model and quantify and will be of modest size (see how Reduce Cyber Risk).

Although cyber risk has been transferred to capital markets on a private basis through collateralized reinsurance deals, these public transactions may represent a stepping stone to broader market acceptance that provides insurance companies additional capital, lessens counterparty risk, and a future vehicle for cyber catastrophe coverage (see Cyber Insurance Trends in 2023).

Primary insurers cede an estimated 50% of direct cyber premiums with the majority of risk concentrated in the largest global reinsurers and the Lloyd’s market.

ILS deals offer different structural profiles & limited distribution

Fermat Capital Management (AuM: approximately $10 billion) was the main investor to the Beazley-sponsored “Cairney” cyber bond of $45 million providing excess-of-loss (XoL) coverage for cyber claims exceeding an attachment point of $300 million.

Stone Ridge Asset Management provided the funds for Hannover Re’s $100 million collateralized reinsurance deal on a quota share (QS) arrangement

These transactions of $145 million are a small fraction relative to the $10 billion of the 144(a) debt instruments cat bonds issued in 2022, which typically cover natural events such as “named storms” or earthquakes.

The more expansive alternative reinsurance of risk capacity (cat bonds, collateralized reinsurance, sidecars and industry loss warranties) is between $90 – $100 billion.

Cyber insurance represents less than 1% of the nearly $800 billion of total U.S. industry direct premium written (DPW) but is the fastest growing product line with DPW expanding by 73% in 2021 to $4.8 billion.

The TOP-10 writers of cyber insurance represent 55% of DPW in 2021 (and the top-15 represent 70%).

Munich Re projects the global cyber market could reach $25 billion by 2025. By comparison, DPW for U.S. homeowner’s multi-peril was $103 billion in 2022.

Significant rate increases by insurers in reaction to rising loss frequency and associated claims costs across the market fueled the increase in DPW.

While rate increases are moderating, global broker Marsh reports cyber renewal rates increased by an average of 48% in 3Q22.

Top 15 (Re)Insurance Cyber Underwriters

Combined Stand Alone & Package Cyber Coverage

| Company | DWP ($ mn) | Share (%) |

|---|---|---|

| Chubb | 473.1 | 9.8 |

| Fairfax Financial Holdings | 436.4 | 9.0 |

| AXA XL | 421.0 | 8.7 |

| Tokio Marine US | 249.8 | 5.2 |

| AIG | 240.6 | 5.0 |

| Travelers Companies | 232.3 | 4.8 |

| Beazley Insurance | 199.9 | 4.1 |

| CNA Financial | 181.4 | 3.8 |

| AXIS Capital Holdings | 159.1 | 3.3 |

| Zurich American | 151.9 | 3.1 |

| Liberty Mutual Insurance | 141.5 | 2.9 |

| Sompo Holdings | 133.5 | 2.8 |

| BCS Insurance | 132.0 | 2.7 |

| Hartford | 123.2 | 2.6 |

| Alleghany | 88.6 | 1.8 |

| Top 10 Market Share | 2,745.4 | 56.9 |

| Top 15 Market Share | 3,364.3 | 69.7 |

DWP – Direct written premium. DWP includes both quantified and estimated premiums. Data based on statutory accounting practices.

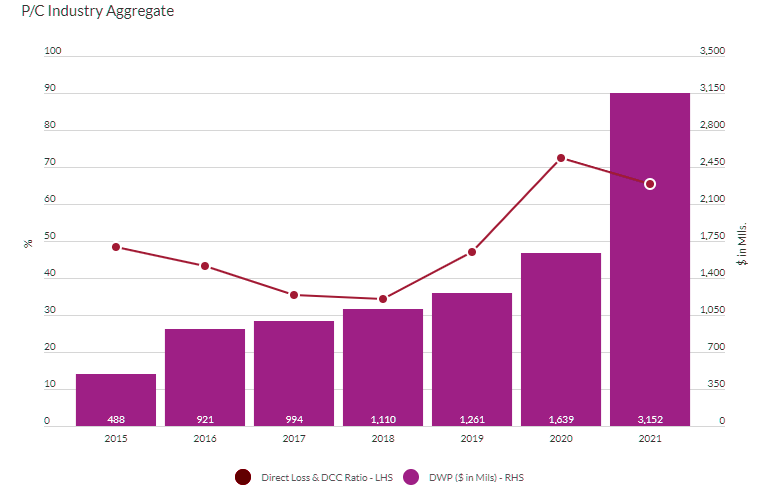

U.S. Statutory underwriting experience for stand-alone cyber policies was highly profitable from 2015-2019 with an industry direct loss ratio averaging 42% for the period. Experience deteriorated in 2020-2021 with the loss ratio rising to an average of 69%.

Standalone Cyber Risk Direct Loss & DCC Ratios

Global insurance-linked securities (ILS) market remains bogged with prior catastrophe losses as the overall performance of funds deteriorates, despite another year of record cat bond issuance. Issuance in the 144a cat bond market reached a record of approximately $12.5bn.

Despite the generally higher returns cat bonds offer, US insurers hold only about $850m of the roughly $33bn outstanding cat bonds.

Correlation with catastrophe risk in their underwriting books could be a concern with regard to asset allocation.

According to Global Insurance-Linked Securities Market Outlook, only about 40 insurers have exposures to cat bonds and five companies account for nearly 70% of investments.

Swiss Re’s US entities hold more than 20% of the industry’s investments, across a variety of risks and cedents, with the majority of the other investors being life insurers.

What is ILS in insurance terms?

ILS are products of the rapid development of financial innovation and the convergence of the insurance industry and the capital markets. The securitization model has been employed by insurers eager to transfer risk and use new sources of capital market funding.

What is the advantage of insurance-linked securities?

Insurance-linked securities allow insurers to transfer some of their risk to investors. For example, in the case of catastrophe bonds, the issuer pays a coupon to an investor in exchange for protection from a specified type of event — such as a hurricane or earthquake — for a particular duration of time.

What is the difference between ILS and CAT bonds?

Cat bonds have been primarily used in property lines of insurance but are also used in other lines of business. ILS represent a convergence of the insurance industry and capital markets.

How does ILS reinsurance work?

ILS involve the transfer of risk from an insurance company to an investor who, in return, receives a share of regular insurance premiums (subject to a certain level of claims not being received by the insurer).

How much reinsurance capacity does ILS have?

The amount of ILS in the global reinsurance industry is approximately $95 billion, which represents approximately 20% of total available reinsurance capacity.

Is ILS collateralized reinsurance?

ILS is another form of reinsurance available to insurance entities. However, instead of facing a rated balance sheet, the insurance entity faces a fully secure, collateralized form of funding dedicated to a precise risk requiring coverage.

……………….

AUTHORS: Jeff Mohrenweiser – Senior Director, Insurance Fitch Ratings, Gerald B. Glombicki – Senior Director, Insurance Fitch Ratings, Laura Kaster – Senior Director, Fitch Wire North and South American Financial Institutions Fitch Ratings