Sale of individual insurance policies has decreased of 7.8%. The beginning of 2024 has been slow when compared to the previous year, with January showing a fall of 3% in new application volumes, according to Swiss Re’s Term & Health Watch report.

2024 year characterised by uncertainty, with recurring political change, compounded by high inflation and a growing cost-of-living crisis.

Although, this figure was contrasted by an increase of new business APE of 9%. There are fewer people buying protection, but those who do, are buying bigger.

The total underwritten whole-life sales increased by 34.5% to 27,807 policies. This is credited in part, to the reaction to the government’s decision to freeze the UK’s Inheritance Tax thresholds once again.

Total guaranteed acceptance whole-life sales were 206,802, showcasing a drop of 31.3%.

The number of new term-only sales decreased by 5.3% to 1,149,976 in 2022. The number of term assurances with critical illness insurance fell by 7.3% – a strong contributing factor to this fall was a 12.5% drop in sales of decreasing term with critical illness sales. Decreasing term sales without critical illness, on the other hand, increased by 4%. This could signal affordability concerns throughout the cost-of-living crisis, compounded by a slowing housing market.

New term assurance sales with a CI benefit represent 28% of total new term sales, one percent lower than in 2023.

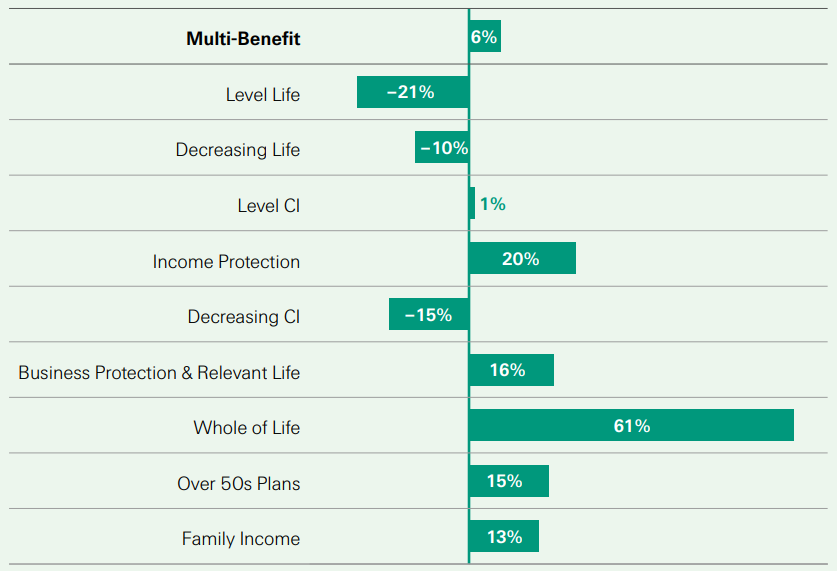

Single-benefit Policies

- In January 2024 Multi-Benefit policies were up 6% on the same period in 2023, absorbing some of the market for single-benefit term assurance.

- Level Life saw the biggest fall by –18% across both multi and single-benefit policies and both Decreasing Life and Decreasing CI also fell though less severely.

- The demand for Level CI has continued to expand, with 5% growth when looking across both multi and single-benefit policies, and a 1% growth as just a single-benefit.

- The Whole of Life market saw tremendous growth with record January 2024 applications 61% up on last year.

- Price competition for life cover continued into 2024, meaning the average of the cheapest 5 products, excluding low start plans, for a basket of cases was 2% lower in December 2023 compared with January 2023. Market pricing for Critical Illness cover has been getting marginally more expensive, increasing by 0.5% over the same period.

The cost-of-living crisis will have impacted households differently depending on their overall financial resilience. However, most people will have felt the impact of inflation in the last twelve months, so it is unsurprising that individual long-term life and health protection sales were impacted. It was a challenging year for total new sales compared to 2023, but it was encouraging to see that average sums assured had increased.

The pressure on UK households was the highest it has been in years as the costs of everyday goods and services rose continuously, with the Consumer Price Index rising by 10.5% in the 12 months to December 2023.

In 2024, there were 2,114,559 new term, whole life, critical illness, and income protection policies sold. Comparatively, there was a 6.3% growth in 2023 where 2,293,704 policies were sold, following the bounce back from the COVID-19 pandemic.

The average sum assured for all new term assurance sales, including term assurance with a critical illness benefit was £177,665 (an increase of 9.4% on the previous year). The largest percentage increases were seen with level term assurance (11.7%), relevant life (21.9%) and family income benefit (13.8%) – see full table below. The increase could be reflective of rising inflation referred to earlier and the desire to keep cover in line with rising costs.

Although there was a drop in new sales for the term and critical illness overall, average new sums assured and premiums for all term assurance and critical illness products saw a rise.

The total number of new individual income protection policies sold rose by 2% to 180,547. While total income protection premiums increased by 12% in 2024.

New maximum two-year benefit payment policies surpassed the number of “to retirement” income protection policies sold for the first time standing at 86,309 and 78,397 policies respectively.

The decline in new level term non-advised purchases is one of the stand-out statistics this year.

42% of total sales is still well ahead of the 24% seen in 2018 but way below 50% in 2024. New-level term non-advised sales fell by 24% and those with a CI benefited by 27%.

The market faced some difficult challenges, and we attribute this fall in part to the cost-of-living crisis which has put people off making what they may see as discretionary purchases.

Above inflation, new sums assured for level term in particular (11.7%) reflect that advisers appear to be managing better in the current difficult environment.

by

by