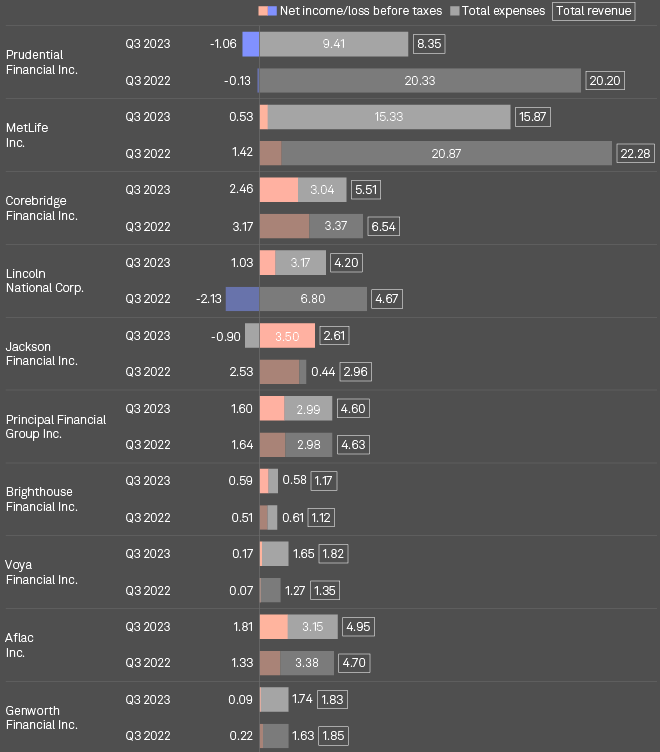

Similar to the Q2 2023, the majority of the top US life insurers posted year-over-year declines in revenue.

Voya Financial, Aflac and Brighthouse Financial were the exceptions, with Voya logging the largest year-over-year revenue gain.

Voya’s revenue grew to $1.82 billion in the third quarter from $1.35 billion a year ago. Aflac booked third-quarter revenue of $4.95 billion, up from $4.70 billion a year earlier, and Brighthouse Financial had third-quarter revenue of $1.17 billion, a modest uptick from $1.12 billion in the prior-year period.

MetLife Inc. posted the second-largest year-over-year revenue decline. Its revenue came in at $15.87 billion in the third quarter, down from $22.28 billion a year ago.

Prudential Financial Inc. experienced the largest year-over-year decline in revenue in the third quarter among the largest publicly traded US life insurers.

Total revenue came in at $8.35 billion for the third quarter, a steep drop from the $20.20 billion reported for the same period in 2022.

Prudential reported a net loss for the third quarter of $802 million, or $2.23 per share, compared to a net loss of $92 million, or 26 cents per share, in the year-ago period.

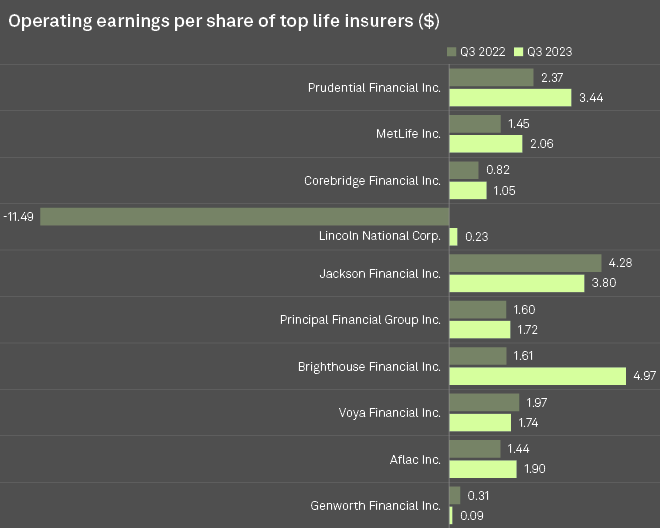

Earnings rose for most of the top listed US life insurers, with just three companies — Jackson Financial Inc., Voya and Genworth Financial Inc. — experiencing year-over-year declines.

Lincoln National Corp. posted the most significant earnings gain in the third quarter. The company booked earnings per share of 23 cents, a massive increase from a loss of $11.49 per share in the third quarter of 2022.

Although Lincoln showed year-over-year improvement, its third-quarter earnings included net unfavorable notable items of 84 cents per share related to its annual review of reserve assumptions as well as an unfavorable impact of 41 cents per share related to items affecting its life insurance business.

During Lincoln’s earnings call, the insurer said its previously announced $29 billion deal with Fortitude Reinsurance Co. Ltd. that was expected to close in the second quarter would instead close in the fourth quarter.

by Hailey Ross – insurance reporter with S&P Global Market Intelligence’s Global Insurance team, Kris Elaine Figuracion – Insurance Associate at S&P Global Market Intelligence