The recent spike in dedicated reinsurance capital growth may prove short-lived, given expectations for depressed investment markets, continued geopolitical turmoil and a potential decline in global gross domestic product.

According to AM Best, declining reinsurance profitsDedicated reinsurance capacity in 2022 increased to $568 billion, driven by an increase of nearly 11% from traditional reinsurance capacity providers.

For 2023 is that total dedicated capital will slide back after a decade of year-over-year increases, driven by reductions in traditional reinsurance capital.

Although underwriting returns for many companies have been close to break even in recent years, analysts note that capital levels grew through investment gains and inexpensive debt financing.

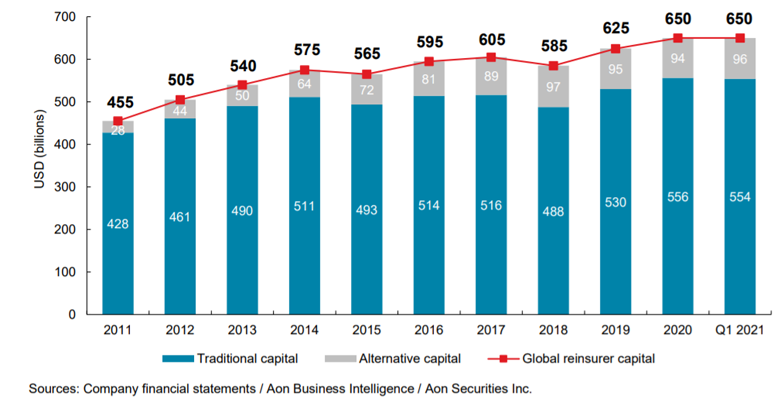

According to Global Reinsurance Sector Outlook, supporting risk transfer, global reinsurance capital increased 3.8% through year end 2021 to $675 billion, with traditional capital increasing 4.1% to a new peak of $579 billion and alternative capital growing to $96 billion (slightly shy of the peak levels at $97 billion in 2018). With record issuance in the catastrophe bond market in 2021, issuance pipelines continue to expand as the turmoil created by non-loss external sources is expected to be short-lived.

Catastrophe activity in Q1 2022 resulted in more than $10 billion of losses to the industry. That said, this is consistent with average results for the prior 10 years and significantly less than losses experienced in 2021. While a number of events surpassed the $1 billion level, overall losses were distributed fairly evenly among the regions.

Global Reinsurer Capital

But challenges in the macro-economic environment mean that the start of 2022 has seen a reversal of most of these conditions.

Headwinds in the capital and investment markets to continue in 2022, dragging down traditional capital levels, some of these losses likely will be offset by underwriting gains

Dan Hofmeister, Senior Financial Analyst at AM Best

The historical lack of a strong correlation between underwriting and asset returns may indicate relatively flat capital levels, but the repeat of a severe property catastrophe season in 2022 could prove to be adverse for reinsurers.

Many reinsurers substantially decreased property exposure through the last renewal cycle, and those still exposed to material amounts of multiyear reinsurance contracts or who did not manage risk exposures prudently could be exposed to material capital deterioration should they suffer underwriting losses, especially if coupled with adverse investment market returns in 2022.

A reduction in traditional capital of roughly $40 billion, or 8.4%, by year-end 2022.

But, on the third-party reinsurance capacity side, the pullback of traditional reinsurance in catastrophe-exposed markets such as Florida has created opportunities for insurance-linked securities (ILS) funds.

By taking advantage of the lack of capacity, some ILS funds have been able to capitalize on not only significant price increases, but also on tighter terms and conditions.

by Yana Keller