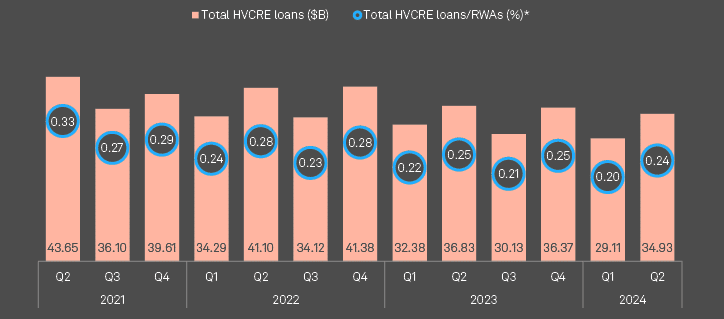

US banks saw a 20% rise in high-volatility commercial real estate loans (HVCRE) in Q2 2024, following a four-year low in the previous quarter, according to S&P Global Market Intelligence.

These loans, typically riskier due to their higher capital requirements, are tied to projects like construction and land development.

The total balance of these loans reached $34.9 bn, up from $29 bn in Q1 but down 5.2% from $36.8 bn a year earlier.

HVCRE loans made up 0.24% of banks’ risk-weighted assets in Q2, a 4 basis point increase from Q1.

The rise indicates growing exposure to potentially volatile sectors, which could signal increased risk for banks if market conditions change. This trend may prompt regulators to scrutinize balance sheets more closely, especially with the ongoing focus on financial stability in the face of economic uncertainty.

Aggregate high-volatility commercial real estate loans trend

Regulators define HVCRE ADC loans as those used to finance acquisitions, developments, or construction of real properties. These loans depend on future income, sales, or refinancing of the properties for repayment.

The loans exclude certain property types, including residential, agricultural, and commercial real estate with permanent financing, and those made before January 1, 2015.

The rule does not apply to community banks that use the community bank leverage ratio framework.

Federal Reserve Board issued guidance with important implications for banks in the US with respect to cryptoasset activities.

In a policy statement, the Fed indicated that it intends to exercise its authority to limit the cryptoasset activities of state member banks (SMBs) it oversees.

U.S. banks are increasingly using insurance as a key mitigant against growing climate-related risks and potential losses in their commercial and residential real estate loan portfolios by limiting exposure to volatile, deteriorating weather environments, Fitch Ratings says.

Banks’ climate risk governance is increasingly important as losses related to weather events occur with more regularity and as regulators scrutinize climate-related vulnerabilities and local, state and federal authorities implement policies that influence economic incentives.

The Federal Reserve’s recent “Pilot Climate Scenario Analysis Exercise” underscores the importance of hazard insurance in reducing potential losses for banks. It advises banks to regularly review and update their insurance coverage and underwriting practices to keep pace with industry changes and protect their credit profiles.

by Yana Keller

by Yana Keller