Private health insurance coverage in the US rises sharply with household income, according to new research from GlobalData, released as Donald Trump submits a healthcare reform proposal to Congress targeting prescription pricing and insurance costs.

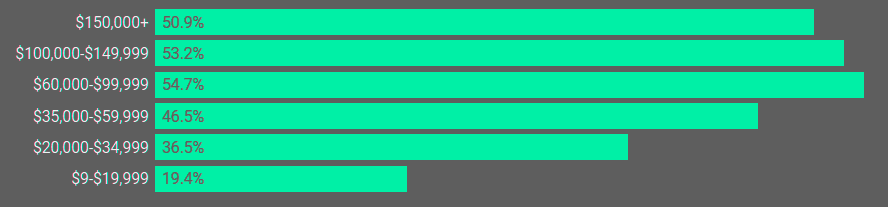

Financial Services Consumer Survey shows only 19.4% of respondents earning $0 to $19,999 a year reported holding private health insurance.

Among households earning $150,000 or more, coverage reached 50.9%. The gap points to affordability as a structural barrier rather than a lack of demand, according to Beinsure analysts.

Fitch Ratings assigns a deteriorating outlook to the U.S. health insurance sector for 2026, citing sustained pressure from high medical costs, disruption tied to the year-end 2025 expiration of enhanced Affordable Care Act marketplace tax credits, and unresolved regulatory and policy risk.

The Affordable Care Act (ACA) is a comprehensive reform law, enacted in 2010, that increases health insurance coverage for the uninsured and implements reforms to the health insurance market.

This includes many provisions that are consistent with AMA policy and holds the potential for a better health care system.

The findings arrive alongside the White House proposal branded the Great Healthcare Plan. The administration says the package aims to lower consumer costs and widen access to coverage.

A White House fact sheet outlines plans to bring US prescription drug prices closer to international reference levels and expand price transparency across healthcare services.

Private health insurance penetration rates

A central insurance element involves restructuring federal subsidies. Instead of routing support through insurers, subsidies would flow directly to eligible individuals.

Consumers would select plans themselves, with the administration stating this structure would intensify competition, reduce premiums on commonly chosen plans by more than 10%, and cut taxpayer spending by at least $36 bn.

The proposal also targets cost drivers tied to intermediaries. It calls for eliminating specific payments linked to pharmacy benefit managers and brokers, which the administration describes as inflating end prices.

New disclosure rules would require insurers to publish policy pricing, benefit structures, claims denial rates, and administrative cost data in plain language.

Similar transparency standards would apply to Medicare and Medicaid providers.

- For lower-income households, the approach would narrow income-based coverage gaps highlighted by GlobalData’s research.

- For insurers, the framework points toward tighter price competition, simpler products, and greater sensitivity to consumer choice as transparency expands.

If enacted, the reforms would shift pricing pressure onto insurers and increase visibility into cost structures across the market.