U.S. life insurers looking for higher yields and longer-term returns have raised their allocations to private credit and Level III assets but are not expected to face widespread rating pressure if private credit performance weakens over the next one to two years, Fitch Ratings says.

The riskiness of these investments is partially mitigated by insurers’ diversified investments, strong asset-liability management, ample capitalization, and ratings headroom.

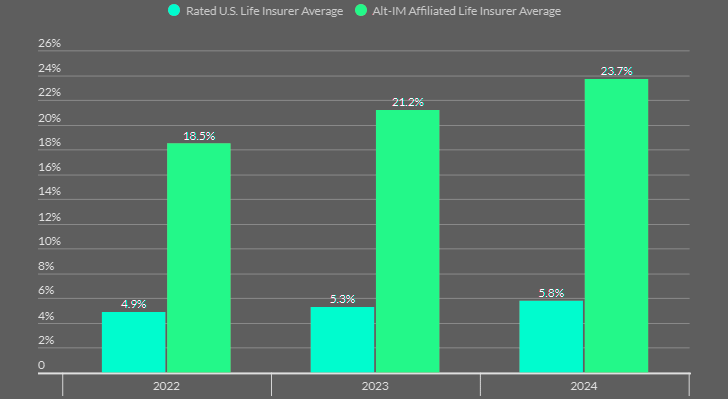

In contrast with the broader life insurance industry, Alt IM-backed life insurers allocate a higher proportion of their portfolios to structured securities and private asset classes and invest more in lower-rated instruments.

Exposure to Level III assets for life insurers affiliated with Alt IMs was 24% compared to 6% for non-affiliated insurers as of YE 2024.

Alt IM-Affiliated Life Insurers Hold Above-Average Level III Assets

Fitch says private credit isn’t a systemic threat for insurers. Not yet. The market still looks small compared to the broader financial system, and capital comes in through funds with locked commitments, limited redemption risk, and only moderate leverage at the fund level.

But growth has been explosive, spreads are compressed, competition keeps rising, and retail buyers keep showing up. The whole setup has a whiff of bubble behavior.

Life insurers in the US are piling deeper into illiquid bets – private credit deals and Level III assets. These investments can crank up valuation swings, liquidity stress, and concentration risk.

They also make balance sheets harder to parse, since valuations depend less on markets and more on subjective models, sometimes with inputs that don’t age well.

When markets tighten or credit cycles turn, the structure gets heavier. Borrowers deal with larger debt service costs, even as rates stabilize, and profit volatility feeds through. Insurers then hold the bag on valuation gaps, impairments, or messy restructurings.

Those most exposed are firms with chunky concentrations and market-sensitive liabilities, and they could take the hit on ratings.

Level III assets in particular show why this matters. They’re illiquid, complex, and carry far less transparency than anything public.

Models say what they’re worth, but models only stretch so far. And that’s the tension – these positions can juice returns when the cycle runs hot, but in a downturn, the opacity works against insurers.